After School Tutoring Receives Double Reduction, Week in Review

3 Min. Read Time

Week in Review

- China markets began the week lower on Monday as the PBOC released a report on the E-CNY, confirming that the digital currency is not a threat to payments processors such as Alipay.

- The divergence between overseas-listed and Mainland-listed China equities in terms of performance continued to widen this week as perceptions of the country’s economic situation and the health of its tech firms differ between Mainland and foreign investors.

- Clean technology and stocks representing the electric vehicles ecosystem outperformed on Wednesday.

- Internet stocks saw a rebound on Thursday as investors and the international community await meetings between the US and China this weekend.

Key News

We knew after-school tutoring (AST) was going to have hours curtailed to reduce the cost of having kids to stem China’s declining birth rates. However, the apparent outcome appears to be far worse than anyone imagined. The companies will not only be prohibited from tutoring on weekends and holidays but may also have to become nonprofits. I use “appears” and “potentially,” as the official rules have yet to be circulated though they were distributed to regional regulatory offices and leaked on social media. The document is named “double reduction,” which seems understated compared to the impact it will have on the companies. The move is shocking as it would effectively put the companies out of business or require them to spin out their K-12 education businesses into a non-publicly traded unit. The companies will likely see a floor based on how much cash they have on hand.

We know Didi will be fined, but hopefully the reaction to this regulation causes a pause in the broader regulatory effort. Ultimately, consumers continue to utilize the services of the companies within the e-commerce, online gaming, and social media space. Remember, we Alibaba will report earnings on August 3rd.

Asia markets were mixed as Japan was on holiday today. The AST news weighed on Hong Kong and the technology space while the Mainland market saw profit-taking in the growth sectors that have been leading the market higher of late. Elements of cleantech managed a strong day on the Mainland as some metals, solar, and auto manufacturing all outperformed.

H-Share Update

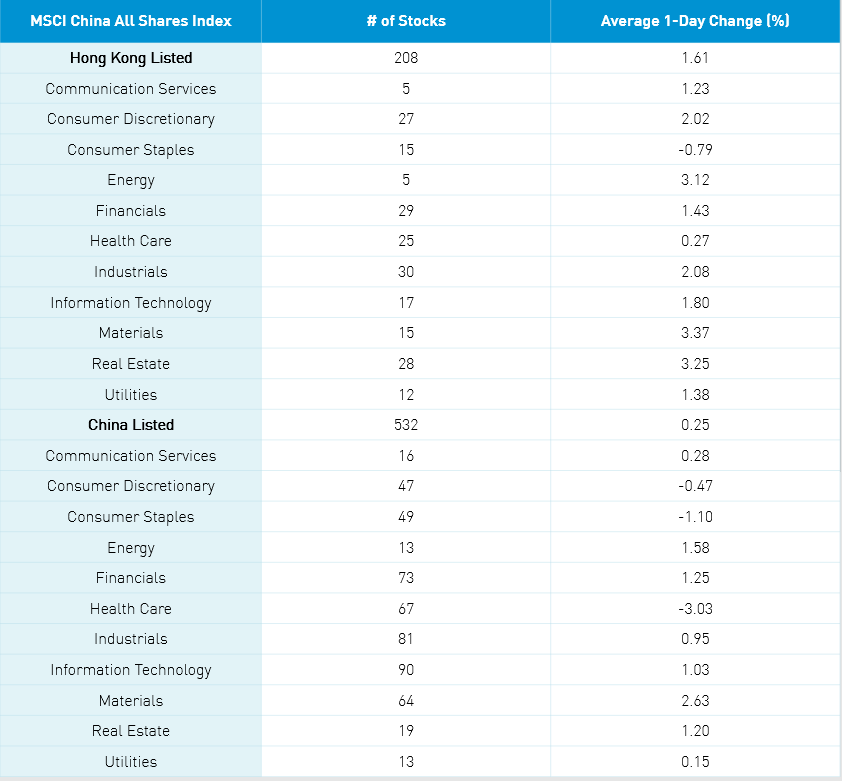

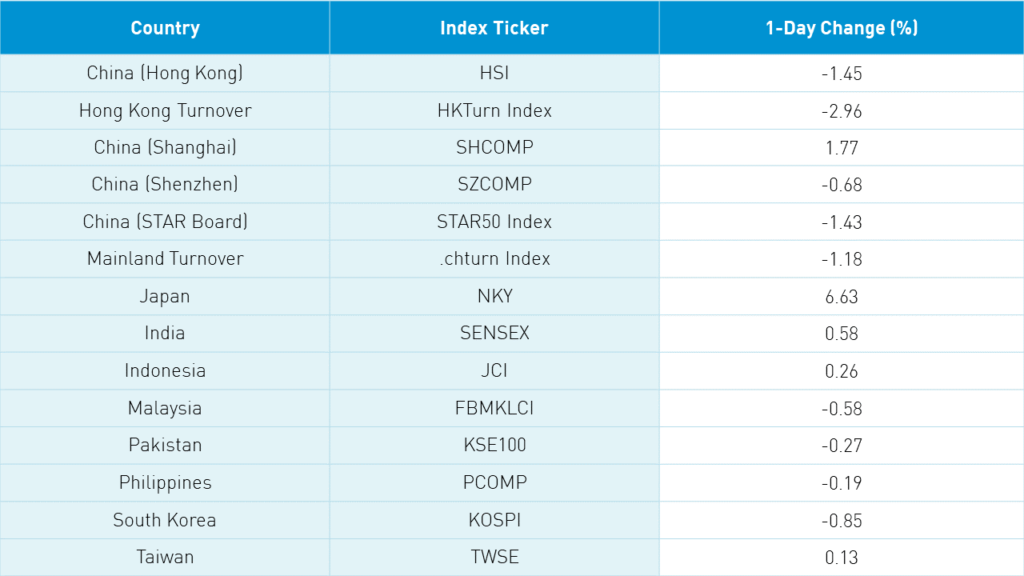

The Hang Seng Index and Hang Seng TECH Index grinded lower over the course of the trading closing -1.45% and -2.96%, respectively, as volume increased +1.79% though still only 85% of the 1-year average. The 208 Chinese companies listed in Hong Kong were off -1.71% with tech off -2.86%, healthcare -2.56%, communication -2.44%, industrials -1.77%, staples -1.77%, discretionary -1.53%, real estate -1.45%, materials -1.11% and utilities -0.8%. Hong Kong’s most heavily traded stocks by value were Tencent, which fell -2.39%, Meituan, which fell -2.36%, HK Exchanges, which fell -3.52%, BYD, which gained +1.52%, Great Wall Motor, which gained +8.23%, Li Ning, which fell -8.26%, Xiaomi, which fell -2.95%, Anta Sports, which fell -4.55%, New Orient Education, which fell -40.61%, and Alibaba HK, which fell -1.06%. Southbound Stock Connect volumes were moderate as Mainland investors sold a net $627 million worth of Hong Kong stocks as Southbound trading accounted for 15.6% of Hong Kong turnover.

A-Share Update

Shanghai, Shenzhen, and the STAR Board were off -0.68%, -1.43%, and -1.18%, respectively, as volume increased +6.63%, which is 152% of the 1-year average. The 532 Mainland stocks within the MSCI China All Shares Index declined -1.34% led by healthcare -3.38%, communication -2.64%, staples -2.45%, real estate -1.54%, utilities -1.17%, materials -1.09%, tech -0.94%. The Mainland’s most heavily traded stocks by value were broker East Money, which fell -2.76%, BYD, which gained +3.9%, COSCO Shipping, which fell -8.88%, Ganfeng Lithium, which fell -5.47%, Inner Mongolia BaoTou Steel, which gained +3.07%, Kweichow Moutai, which fell -2.06%, GEM, which gained +5.96%, Tianqi Lithium, which gained +0..41%, China Northern Rare Earth, which fell -2.93%, and Longi Green Energy, which fell -0.74%. Northern Bound Stock Connect volumes were moderate as foreign investors sold -$719 million worth of Mainland stock.

Last Night’s Exchange Rates, Prices, & Yields

- CNY/USD 6.48 versus 6.47 yesterday

- CNY/EUR 7.62 versus 7.62 yesterday

- Yield on 1-Day Government Bond 1.63% versus 1.67% yesterday

- Yield on 10-Year Government Bond 2.91% versus 2.93% yesterday

- Yield on 10-Year China Development Bank Bond 3.30% versus 3.32% yesterday

- Copper Price +1.34% overnight