Good Riddance to July, Week in Review

3 Min. Read Time

Webinar Today:

Join us Tuesday, August 3rd at 11:00 am EDT for:

China Market Volatility Update and Q&A KraneShares

Click here to register.

The following is a summary of recent statements from the Chinese media regarding the internet regulations:

China’s Solid Economy Guarantees Market Development: Xinhua

- China’s strengthening economy provides a guarantee and foundation for capital market development, official Xinhua says after a clampdown on online tutoring firms fueled an equities rout.

- The recently announced policies targeting “platform economies” and after-school tutoring are aimed at protecting online data security and social welfare rather than outright curtailing those industries.

- China’s securities regulator has an “open attitude” towards companies’ listing venue; will continue supporting companies to choose a suitable venue and develop themselves by using resources in two different markets

China’s Tech, Education Policies Not to Curb Industries: Economic Daily

- The recent regulatory policies on tech and tutoring sectors are not aimed at restricting and suppressing the development of certain industries, but to promote disciplined and healthy growth of the sectors, ensure data security and safeguard people’s wellbeing, Economic Daily said in a front-page editorial Thursday.

- The fundamentals of China’s economic recovery have not changed; China will refrain from using “flood-style” stimulus

- Investors shouldn’t be affected by irrational sentiments. China is firmly committed to reform and opening up, and supports companies’ decision on where to seek listings

Key News

Asian equities were off today, which is fitting for what was a tough month for the region. It was fairly quiet on the news front, but that isn’t surprising for a summer Friday.

There was a significant government meeting in China regarding economic policy in the second half of 2021, with implications for investors. First and foremost, “housing is for living and not for speculating” was reiterated, which explains weakness in real estate overnight. EV was highlighted as a key industry focus along with creating a game plan to meet the 2030 peak carbon goal. Not surprising, the EV ecosystem space and clean technology stocks were today’s winners in Hong Kong and China.

The Mainland market had a decent day though mega/large cap liquor stocks, healthcare and financial stocks were off, pulling down the Shanghai Composite while the Shenzhen and STAR Board managed gains.

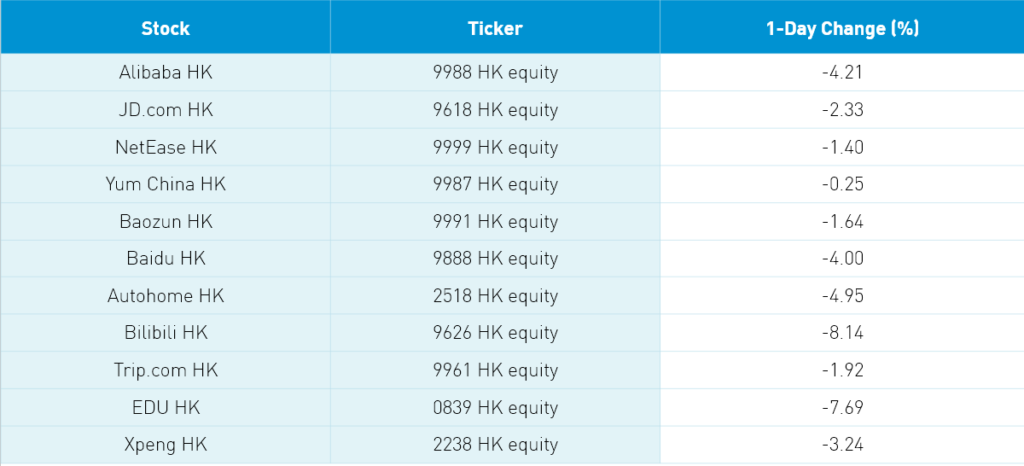

Hong Kong was off today with internet stocks off on the news SEC will examine IPOs more thoroughly post Didi’s IPO debacle. As noted previously, Didi had 60 pages of risk factors.

The Ministry of Industry and Information Technology met with executives from twelve internet companies to reiterate they should protect user data and privacy. Doesn’t seem like a big deal to me as the companies continue to adhere to regulation. However, the news clearly weighed on sentiment, as Hong Kong was led lower by technology plays. Remember we get Alibaba earnings next Tuesday (fingers crossed!).

Northbound Stock Connect flows saw $347mm of net buying of Mainland stocks from foreign investors. Southbound Stock Connect saw another net outflow with Tencent and Meituan reduced. At the top of this post, I included the statements from Chinese media on tempering internet regulation from yesterday thanks to Bloomberg.

SupChina, an online China-focused website, had a good review of Qin Gang, China’s new US ambassador. He appears to be a moderate and well respected though not afraid to speak up.

H-Share Update

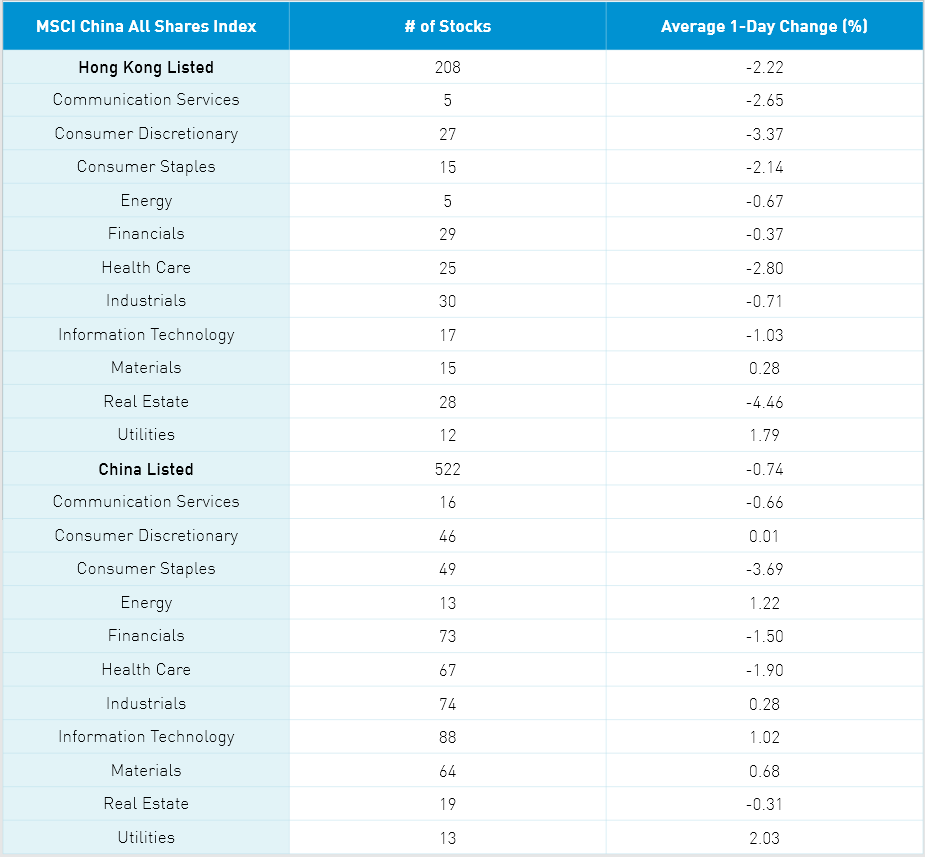

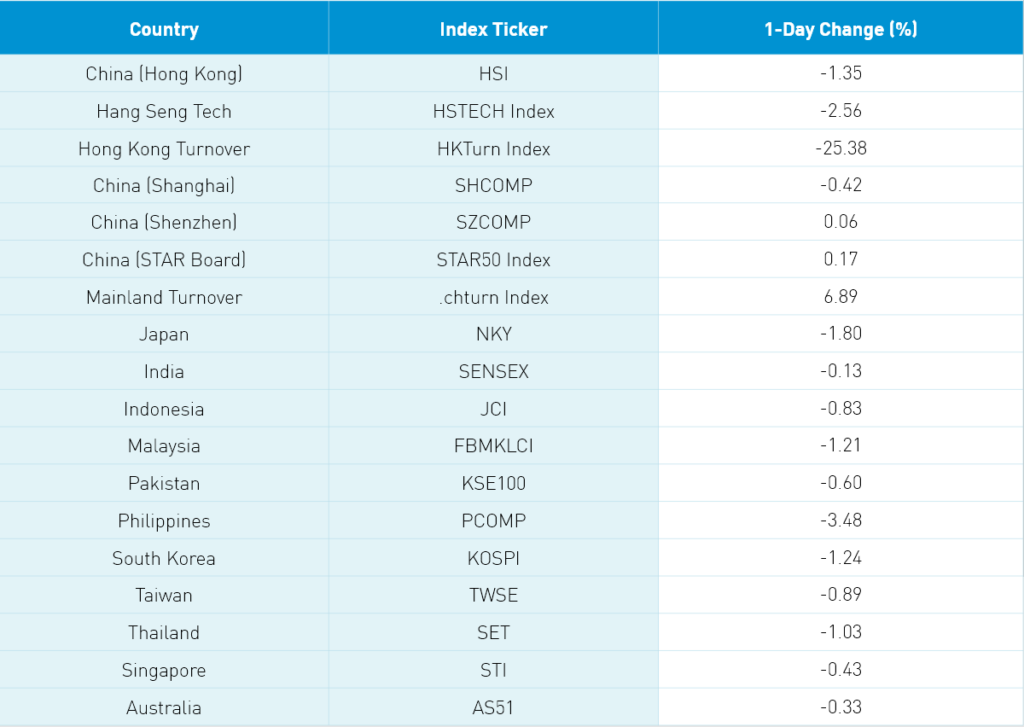

The Hang Seng Index opened lower, sliding further across the trading day though it did manage a late-day rally to stem losses at -1.35% while the Hang Seng TECH Index slid -2.56%. Volumes were off -25.4% from yesterday which is 114% of the 1-year average. The 208 Chinese companies listed in Hong Kong within the MSCI China All Shares lost -2.23% with utilities and materials +1.78% and +0.27% while real estate -4.47%, discretionary -3.38%, healthcare -2.81%, communication -2.66%, staples -2.15%, tech -1.03%, industrials -0.71%, energy -0.68% and financials -0.38%. Hong Kong’s most heavily traded by value were Tencent -2.64%, Meituan -5.87%, Alibaba Hong Kong -4.21%, SMIC +2.84%, BYD +3.46%, Wuxi Biologics -4.9%, AIA +1.14%, Xiaomi -2.12%, Ping An Insurance +0.89% and Hong Kong Exchanges -0.8%. Southbound Stock Connect volumes were elevated as Mainland investors sold -$205mm of Hong Kong stocks as Southbound trading accounted for 12.4% of Hong Kong turnover.

A-Share Update

Shanghai, Shenzhen and STAR Board diverged -0.42%, +0.06% and +0.17% as volume increased +6.89% from yesterday which is 146% of the 1-year average. The 522 Mainland stocks within the MSCI China All Shares were off -0.74% with utilities +2.03%, energy +1.22%, tech +1.02%, materials +0.68%, industrials +0.28%, discretionary +0.01% while staples -3.69%, healthcare -1.9%, financials -1.49%, communication -0.66% and real estate -0.31%. Foreign investors were active buying +$347mm of Mainland stocks as Northbound Stock Connect trading accounted for 6.4% of Mainland turnover.

Last Night’s Exchange Rates, Prices, & Yields

- CNY/USD 6.46 versus 6.46 Yesterday

- CNY/EUR 7.69 versus 7.67 Yesterday

- Yield on 10-Year Government Bond 2.84% versus 2.88% Yesterday

- Yield on 10-Year China Development Bank Bond 3.24% versus 3.28% Yesterday

- Copper Price +0.24% overnight