Mainland Records Massive Volume Day As Foreign Investors Buy in Size, Hong Kong Internet Rebounds

4 Min. Read Time

August Caixin Manufacturing PMI

Takeaway: The PMI is a diffusion index with readings below 50 indicating contraction and above 50 indicating growth month over month. Delta outbreaks were the main culprit for the Caixin PMI survey's weak reading, which is conducted by IHS Markit. We’ve all read about China closing the port of Ningbo after one worker tested positive though foreign demand slackened as Asia fights Delta outbreaks as well. High input prices i.e. commodity prices are a factor as well, which will be watched closely by policymakers. We had another release of industrial metals from China’s strategic reserves in an attempt to stamp out high commodity prices. I would assume OPEC will be under a lot of pressure to ramp up production for similar reasons. Business confidence remained high, which is a good sign.

Key News

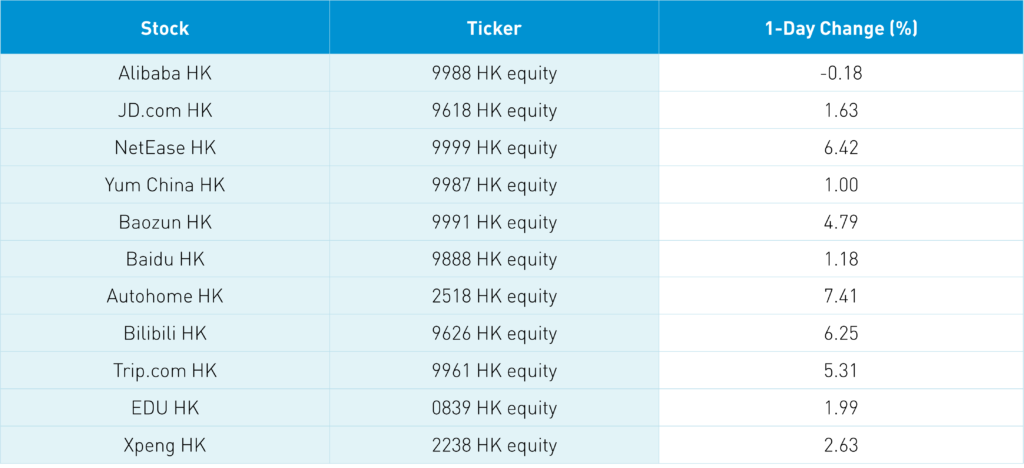

Asian equities were largely higher in an interesting trading day following yesterday’s MSCI rebalance. Hong Kong gained today as internet stocks had a strong day except for Alibaba HK (9988 HK), which posted a small loss. Tencent (700 HK) gained +1.7% as Mainland investors bought via Southbound Stock Connect as the company bought another 220k shares today. Spinout Tencent Music Entertainment (TME US) officially dropped its music exclusivity deals. NetEase HK (9999 HK) had a strong day +6.42% after reporting Q2 results yesterday.

Today’s price action was despite Mainland media specifically mentioning Alibaba and Pinduoduo would be scrutinized for intellectual property rules. Our air pocket thesis is based on the belief that active managers have moved out of the space. With no natural buyers stepping into the space, it would explain the price action.

The recent surge in Indian equities is an indication of the shift out of China internet. Another indication is the uptick in Northbound Stock Connect flows, the trading venue used by foreign investors to hold Shanghai and Shenzhen listed stocks. Overnight, foreign investors bought a healthy $1.189B of Mainland stocks. Remember active managers can’t eliminate China because it is a good weight. I am arguing that active managers moved out of China internet into Shanghai and Shenzhen stocks.

MSCI's rebalance yesterday included a healthy increase in the number of Chinese stocks increased from 730 to 741. Now that this shift has occurred the market is most apt to do what is least expected, which would be a rally in China internet stocks. Fingers crossed!

I grew up caddying, which has led to many a good walk spoiled. In pro golf tournaments, Saturday is called “moving day” because if you want to win you better get yourself in a position to win. Mainland China had the highest volume day over the last year in fact. Many favored sectors such as the EV ecosystem, semiconductors, and clean technology were weaker today while several value sectors such as real estate, financials, and staples outperformed. Active managers in China likely balanced their portfolios between growth stocks/outperformers and value stocks/underperformers. Coincidentally an influential/widely read Mainland financial media source published an interview with four “star” portfolio managers. Three mentioned these growth sectors as areas of focus.

If you missed Saturday’s WSJ had a very good article by Jacob Schlesinger titled “The Return of the Trustbusters” focused on new FTC chair Lina Khan. I learned a lot from it.

Today’s Financial Times has a piece titled “Investors eye emerging market upswing after China shock”. The argument is EM has had a “lost decade”. Yes, that’s true if you solely held the EM benchmark. Take a look at the total returns of these indexes per Bloomberg data from 3/9/2009 to 8/31/2021 in US $s:

I did some homework and found there was gold in them thar hills! One big asterisk – remember the definition of technology changed in September 2018 when the Global Industry Classification System was juggled. Don’t go out and buy “technology” as many of the strong performers left the tech sector for consumer discretionary and communication sectors.

H-Share Update

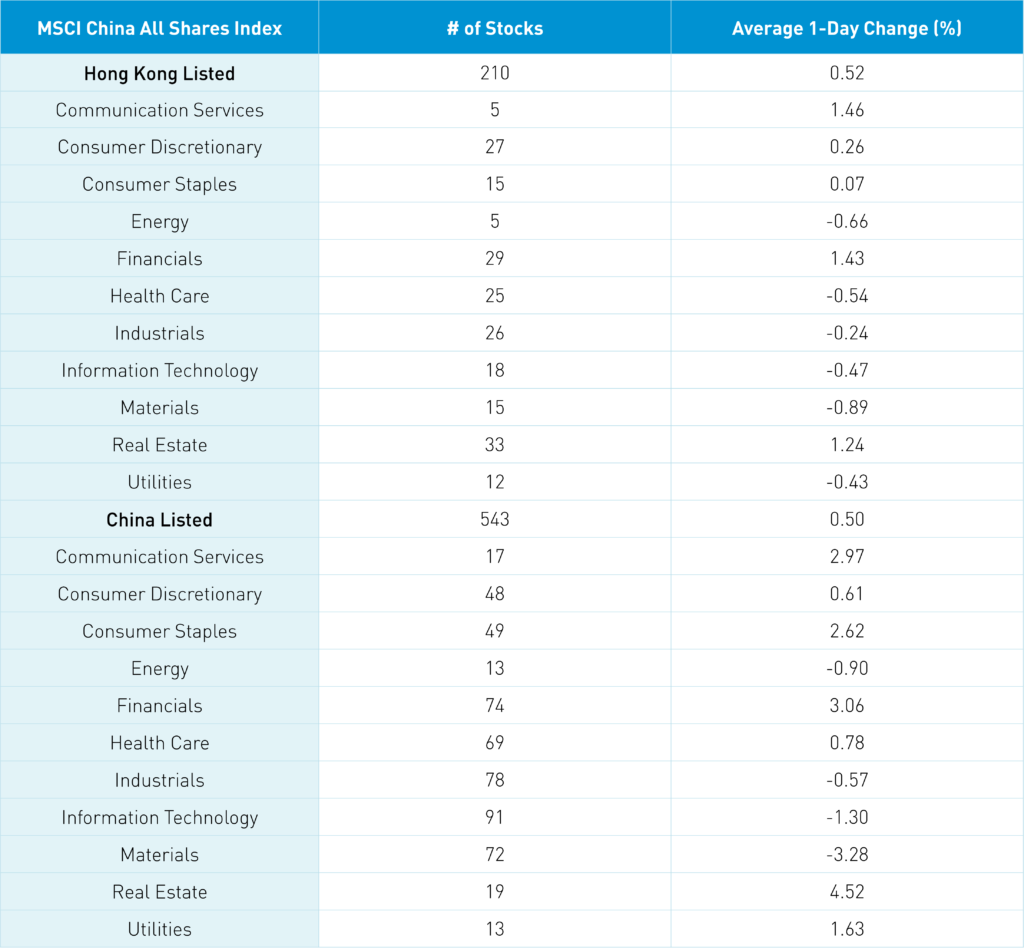

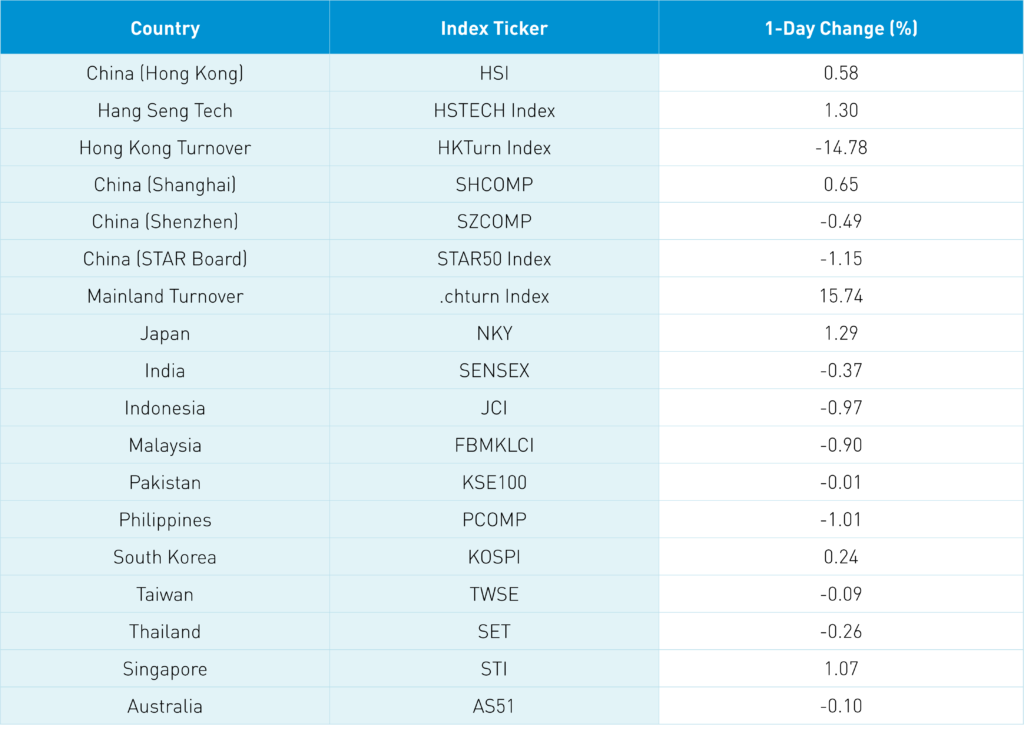

The Hang Seng dipped briefly in the red during morning trading before rebounding to close +0.58% as volume slumped -14.78% after yesterday’s MSCI rebalance trading. Today’s trading was still 108% of the 1-year average. The 210 Chinese companies listed in HK within the MSCI China All Shares gained +0.51% led by communication +1.46%, financials +1.42%, real estate +1.24% and discretionary +0.26% while materials -0.9%, energy -0.67%, healthcare -0.55%, tech -0.47% and utilities -0.44%. HK’s most heavily traded by value were Tencent +1.5%, Meituan +1.77%, Alibaba HK -0.18%, Kuaishou -0.65%, Ping An +1.99%, Dongyue Group -6.53% after selling shares, Xiaomi +0.8%, Wuxi Biologics -2.99%, BYD -2.66% and AIA +0.91%. Southbound Stock Connect trading was moderate/high was Mainland investors sold -$14mm of HK stocks today as Southbound trading accounted for 11.9% turnover.

A-Share Update

Shanghai, Shenzhen, and STAR Board diverged closing +0.65%, -0.49% and -1.15% as volume increased +15.74% from yesterday, which is 184% of the 1-year average. The 543 Mainland stocks within the MSCI China All Shares gained +0.51% led by real estate +4.52%, financials +3.06%, communication +2.98%, staples +2.62%, utilities +1.64% and healthcare +0.79% while materials -3.27%, tech -1..3% and energy -0.89%. The Mainland’s most heavily traded by value were China Northern Rare Earth -7.67%, Inner Mongolio BaoTou Steel +1.06%, TBEA flat, Tianqi Lithium -9.99%, Sany Heavy Industry +9.99%, Kweichow Moutai +4.11%, broker East Money +2.55%, CITIC Securities +4.71%, Longi Green Energy -4.95%, and Wuliangye Yibin +2.98%. Northbound Stock Connect volumes were very high as foreign investors bought $1.189B of Mainland stocks as Northbound trading accounted for 6.5% of Mainland turnover.

Last Night’s Exchange Rates, Prices, & Yields

- CNY/USD 6.47 versus 6.46 yesterday

- CNY/EUR 7.64 versus 7.65 yesterday

- Yield on 10-Year Government Bond 2.82% versus 2.84% yesterday

- Yield on 10-Year China Development Bank Bond 3.16% versus 3.19% yesterday

- Copper Price -0.83% overnight