RMB Rallies Versus the US Dollar Along with Mainland Equities

4 Min. Read Time

Key News

Asia rebounded overnight less Japan and Hong Kong after yesterday’s swoon. CNH, China’s currency that trades outside of China, had a very strong day versus the US dollar, rallying 0.32% from yesterday’s price of 6.47 to 6.45 overnight (because the currency is quoted US dollar divided by CNH, down means appreciation of China’s currency versus the US dollar, kind of confusing!). CNH’s volatility versus the US dollar is back to pre-Evergrande/the world is ending levels.

Tomorrow, China starts the Golden Week holiday as markets will be closed until next Friday. Hong Kong is closed tomorrow though the volumes were light in Hong Kong and China as folks might have cut out early.

Mainland value of volume dipped below RMB 1 trillion for the first time in 50 days. Yesterday’s decliners were today’s advancers as lithium stocks rebounded sharply along with the broader clean technology space including wind, solar, and the electric vehicle (EV) ecosystem as EV battery giant CATL jumped +4.62%. I would expect a significant push for ramping up renewables, considering what is occurring in the coal space.

The National Development and Reform Commission had a lengthy response on the coal shortage, indicating a big push to solve the issue. There was significant Mainland media coverage on efforts to ramp up electrical transmission considering recent curbs due to a shortage of coal. Coal is needed not only for electricity transmission but also for heating as we head into the winter. Thermal coal futures eased overnight after hitting a 52 week and all-time high yesterday.

The PBOC replaced RMB 40B of maturing repos with RMB 100B in a liquidity injection as China heads off on holiday. Today there were 3,516 advancers versus just 618 decliners on the Shanghai and Shenzhen. The Mainland market rally was despite the “official” PMI being mixed/off as September Manufacturing contracted to 49.6 versus August’s 50.1 while the Non-Manufacturing PMI rebounded to 53.2 from August’s 47.5. We also saw Caixin’s Manufacturing PMI release at 50 versus August’s 49.2. Not a lot of commentary on the PMIs candidly nor coverage in China so not likely a market factor.

Foreign investors were net buyers of Mainland stocks though only +$150mm. Hong Kong couldn’t shake its funk closing off -0.36% with internet names off following an article from the South China Morning Post that game approvals are being curtailed. For what it is worth I’ve not seen this news confirmed elsewhere. We are in a shoot first ask questions later mentality, so the weakness isn’t surprising.

Quarter-end window dressing might have been a factor as active managers need to show their top ten holdings. It is feasible that we’ll see active managers, which have been underweight in China and overweight in India, could dip in their toes post-quarter-end. The idea would be to buy a little and see if the names can rebound going into year-end as no one would know you bought.

Cleantech had a nice rally in Hong Kong along with real estate as real estate developer Sunac (1918 HK) rallied 12.77%. Yesterday we hosted Nikko Asset Management’s Head of Asia Credit on a webinar to discuss the Evergrande situation. He believes Evergrande is an isolated issue and is too big to fail. With that said, a restructuring of bonds and loans is apt to keep Evergrande in the news. One nugget was that a single court will handle all Evergrande restructuring cases which is a positive. The webinar replay is available on our website.

The WSJ had an article on Chinese variable interest entities today. The VIE structure was originally used by Chinese companies starting twenty years to list in the US. Not mentioned in the article is the reality that because many of these growth companies weren’t profitable at the time, they weren’t allowed to list on Shanghai and Shenzhen because unprofitable companies aren’t allowed to list. The article tries to make the argument that the VIE structure is a danger to investors. The article completely contradicts itself in the last paragraph by quoting a Hong Kong lawyer who states, “The fact that Shanghai Stock Exchange has allowed VIE-structured companies to list is a sign of validation”. Not mentioned in the article is the reality that the CSRC, China’s financial regulator/like our SEC, has recognized the VIE structure several times. I’ll find several examples and provide them.

H-Shares Update

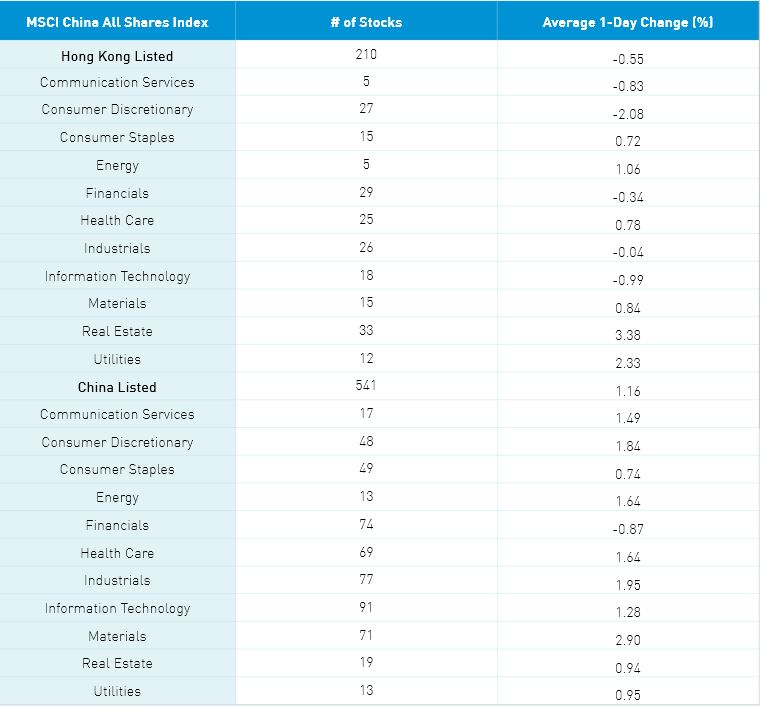

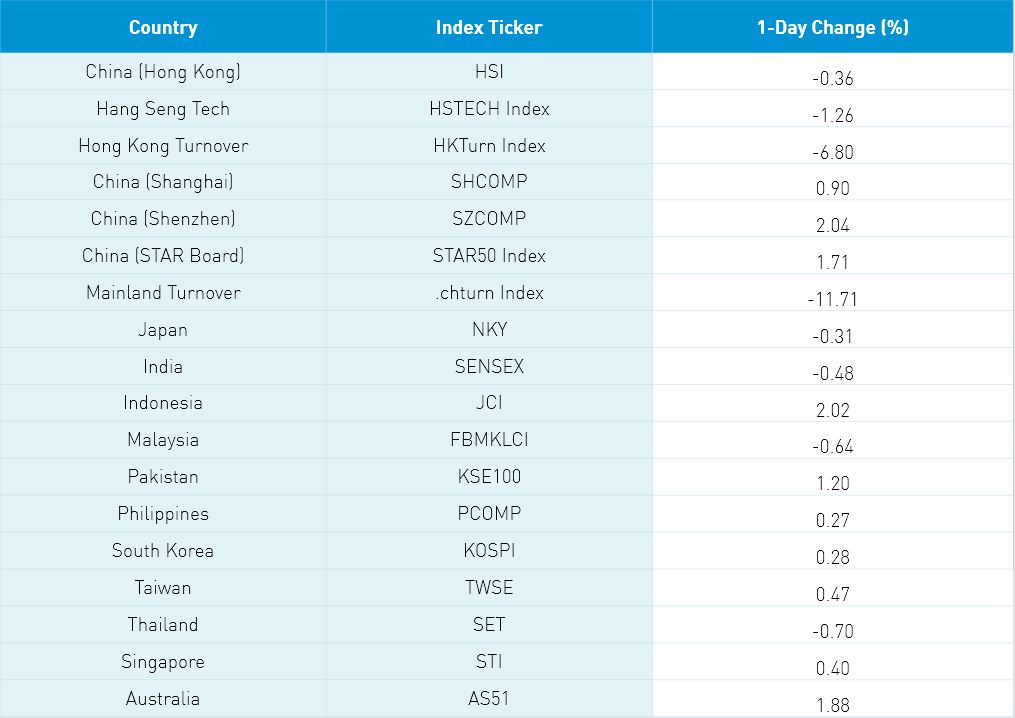

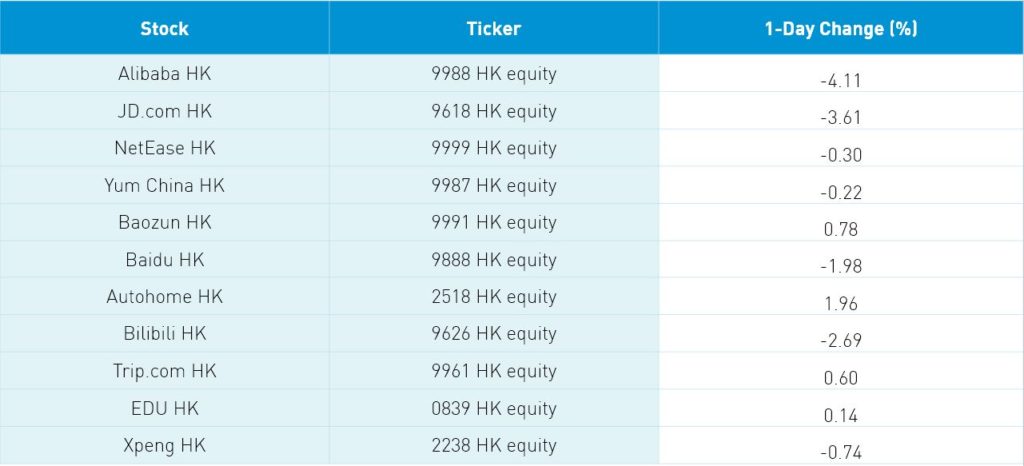

The Hang Seng opened lower but rallied in the afternoon to curtail losses closing -0.36% as volume dipped -6.85% which is only 67% of the 1-year average. The 210 Chinese companies listed in Hong Kong within the MSCI China All Shares lost -0.54% with real estate +3.39%, utilities +2.34%, energy +10.7% and materials +0.84% while discretionary -2.07%, tech -0.99%, and communication -0.83%. Hong Kong’s most heavily traded by value were Tencent -0.77%, Alibaba HK -4.11%, Meituan -1.36%, AIA +1.01%, JD.com HK -3.61%, Ping An -2.38%, HK Exchanges +1.05%, Xiaomi -2.95%, Sunac China +12.77% and Wuxi Biologics +0.56%. Southbound Stock Connect was closed today.

A-Shares Update

Shanghai, Shenzhen, and STAR Board gained +0.9%, +2.04%, and +1.71 on volume off -11.71% from yesterday which is 97% of the 1-year average. The 542 Mainland stocks within the MSCI China All Shares gained +1.16% led by materials +2.9%, industrials +1.95%, discretionary +1.84%, energy and healthcare +1.64%, communication +1.49% and tec +1.28% while financials were off -0.87%. The Mainland’s most heavily traded by value were China Energy Engine -0.33%, CATL +4.62%, Tianqi Lithium +5.81%, Kweichow Moutai +0.55%, Wuliangye Yibin +0.3%, CECEP Solar Energy +2.44%, Luzhou Laojiao +4.77%, China Three Gorges +4.39%, BYD +5.72% and China Northern Rare Earth +6.8%. Northbound Stock Connect volumes were moderate/light as foreign investors bought $150mm of Mainland stocks as Northbound trading accounted for 5.4% of Mainland turnover.

Last Night’s Exchange Rates, Prices, & Yields

- CNY/USD 6.46 versus 6.47 yesterday

- CNY/EUR 7.48 versus 7.54 yesterday

- Yield on 10-Year Government Bond 2.88% versus 2.86% yesterday

- Yield on 10-Year China Development Bank Bond 3.21% versus 3.19% yesterday

- Copper Price -0.68% overnight