Hong Kong Stocks Become An Oasis of Green In A Sea of Red, Week in Review

3 Min. Read Time

Week In Review

- China reported Monday that the country’s GDP grew at a better than expected +8% in 2021, though Q4 GDP disappointed at only +4%.

- Monetary policy easing was the key word in China this week as the PBOC announced cuts to the medium-term lending facility (MLF), reverse repos, and the loan prime rate (LPR), confirming a looser stance in the new year.

- The Biden Administration announced Tuesday that it would be looking into the national security implications of Alibaba’s cloud services in the US. However, the company’s US cloud business represents a negligible portion of the company’s revenue.

- Hong Kong-listed China internet stocks enjoyed a major rebound on Thursday as investors cheered easing and less regulatory uncertainty.

Friday’s Key News

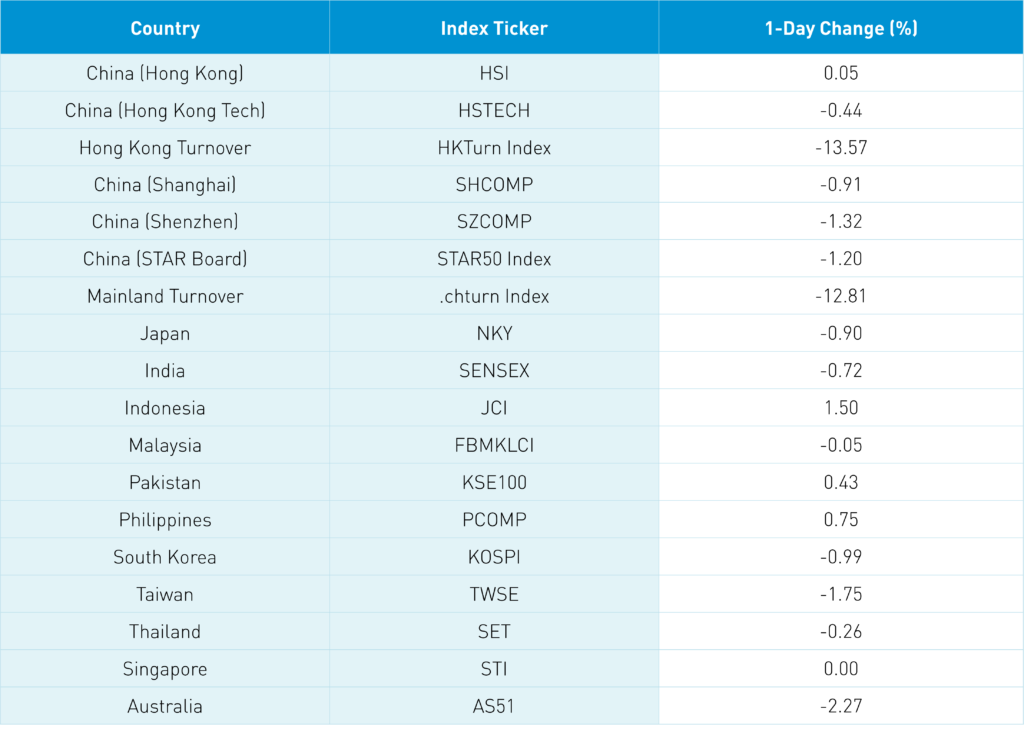

Asian equities had another rough day to end a rough week, though Hong Kong and the Philippines were outliers as both managed small gains. For the week, most markets were off -1% to -2% though South Korea was off an especially deep -3.54%, India was lower by -3.85%, Malaysia was off by -2.88%, and Taiwan was down -3.16%.

Remember that Hong Kong’s uptrend and India’s downtrend may be causing active manager pain due to their being underweight China internet and overweight India. If this early trend can stick, it could “force” big funds back into the space. Another catalyst is the simple reality that the US dollar may strengthen on Fed rate hikes, posing a significant headwind for EM currencies. Hong Kong stocks are denominated in Hong Kong Dollars, which are pegged to the US dollar, providing a margin of safety in such an environment.

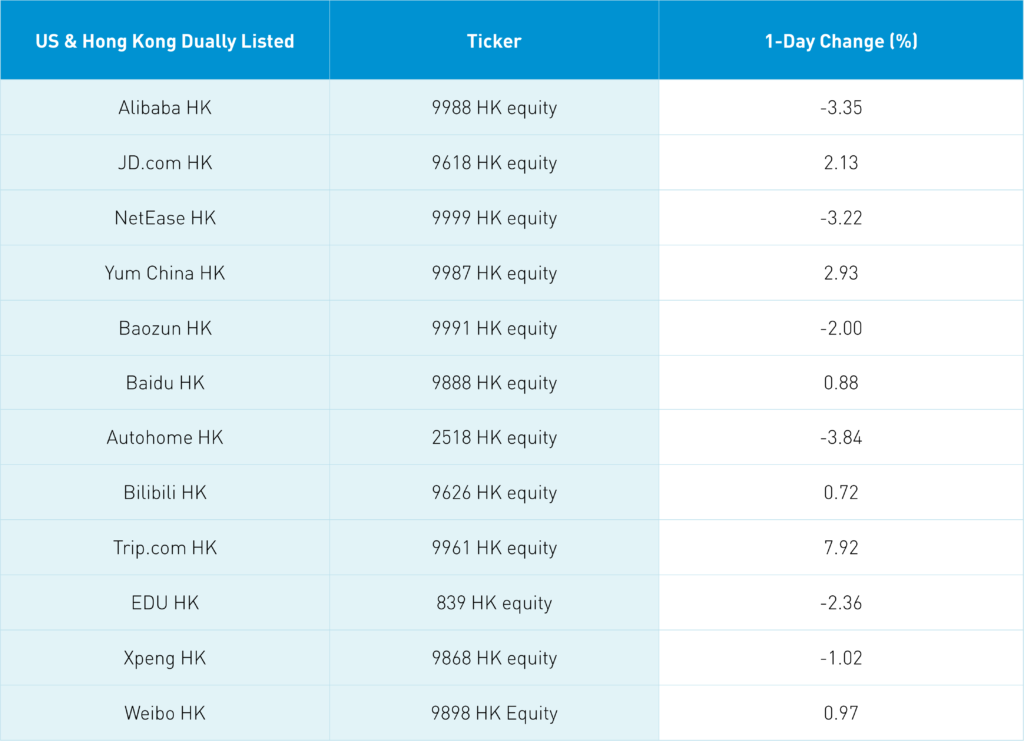

The Hang Seng was up +2.36% for the week while Shanghai was up +0.26% thanks to its value skew and Shenzhen was down -1.74% thanks to its growth skew. Overnight, the Hang Seng gained +0.05% on volume that was down -13.57% from yesterday, which is 95% of the 1-year average. That’s not a bad volume day for Hong Kong as the Hang Seng is right at the 25,000 level. Hong Kong-listed internet stocks were mixed overnight as the highest volume stocks by value traded were Tencent, which gained +0.68%, Alibaba HK, which fell -3.35%, and Meituan, which was flat.

Tencent’s WeChat and Bytedance’s TikTok are being included in the US technology anti-trust bill though the bill might have trouble passing. TikTok has already moved its US customer servers to American soil while Tencent has very few US users (not even my wife will use WeChat).

Tencent and Meituan saw another day of net buying from Mainland investors via Southbound Stock Connect. The Financial Times is reporting that a Chinese TV documentary on corruption included Ant’s purchase of land at a discount. I am not seeing this in Mainland media as an FYI, though the article appears credible. Cities and states tend to give companies breaks on land and tax deals all the time, so I am not sure how damning this is.

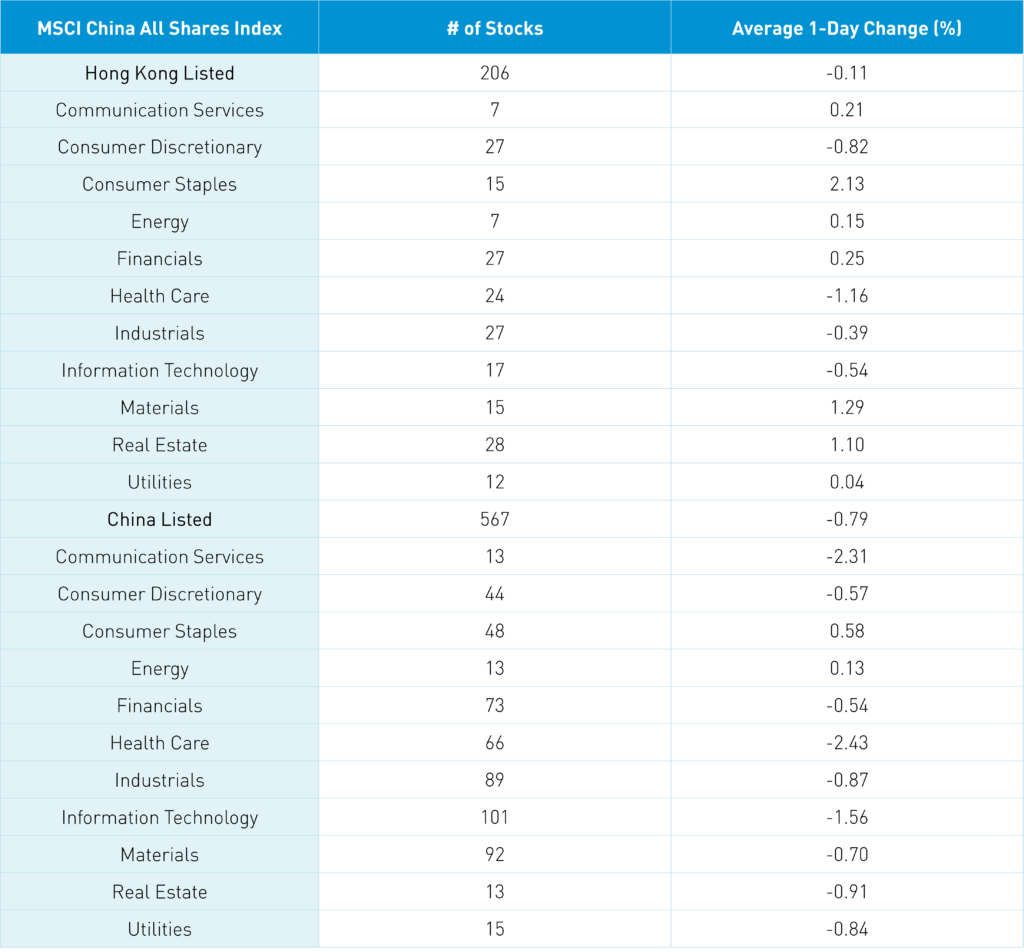

Hong Kong-listed consumer staples names gained +2.15% led by liquor stocks ahead of Chinese New Year’s, materials gained +1.3% as construction inputs including cement gained following yesterday’s LPR cut.

Real estate gained +1.11% on the LPR cut and chatter that Evergrande is bringing in more advisors to navigate its debt situation. Property developer Country Garden issued $500 million worth of convertible bonds, bolstering their balance sheet as some financing restrictions have been lifted for developers.

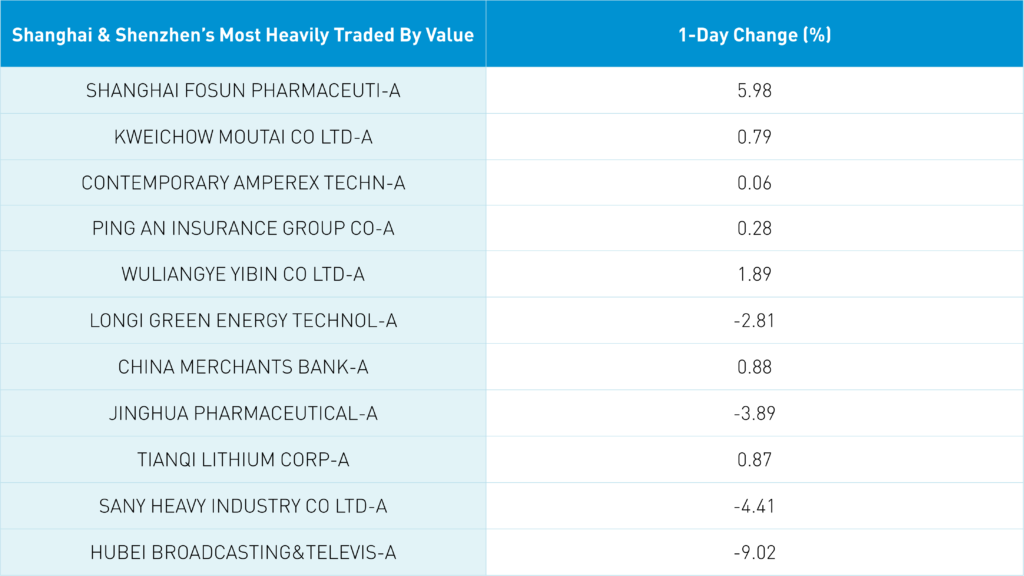

Mainland markets were off despite coverage of Premier Li’s talk of economic policy support as Shanghai fell -0.91, Shenzhen fell -1.32%, and the STAR Board fell -1.2%. Volumes were off -12.81% from yesterday, which is 95% of the 1-year average. Liquor stocks gained overall as Kweichow Moutai rose +0.79% and Wuliangye Yibin rose +1.89%.

Healthcare was weak in both Hong Kong and China though Fosun Pharma gained +5.98% on a new covid drug.

We are still in value/growth rotation in China as favored growth themes and sectors are balanced out with value plays. Breadth was off with nearly 2 decliners versus 1 advancer as large/mega caps (value) held up better than mid and small (growth). We had another big day of buying from foreign investors via Northbound Stock Connect as today’s total was $1.382B, which brings the week’s total to $4.602 billion. Wow! Chinese Treasury bonds rallied again along copper and CNY was flat.

Last Night’s Exchange Rates, Prices, & Yields

- CNY/USD 6.34 versus 6.34 yesterday

- CNY/EUR 7.19 versus 7.19 yesterday

- Yield on 1-Day Government Bond 1.89% versus 1.86% yesterday

- Yield on 10-Year Government Bond 2.71% versus 2.72% yesterday

- Yield on 10-Year China Development Bank Bond 3.01% versus 3.03% yesterday

- Copper Price +0.64% overnight