Alibaba Bounces as China Outperforms on Muted Inflation, Week in Review

2 Min. Read Time

Week in Review

- On Monday, it was reported that the cybersecurity review of Didi had been completed. The review’s conclusion should allow Didi, along with Full Truck Alliance, to eventually relist in Hong Kong.

- Q1 earnings reports this week included Nio, which beat expectations on earnings per share (EPS), and Bilibili, which came short of expectations on EPS.

- Ant Group received an initial go-ahead on a potential public listing. The company may file a preliminary prospectus as soon as next month, though the date of an IPO remains uncertain.

- China internet stocks had a somewhat of a comeback this week on Q1 earnings that were, for the most part, stronger than expected, though expectations were low going into the releases due to lockdowns.

Key News

Asian equities were off today, though China internet and tech stocks continued their outperformance from earlier in the week.

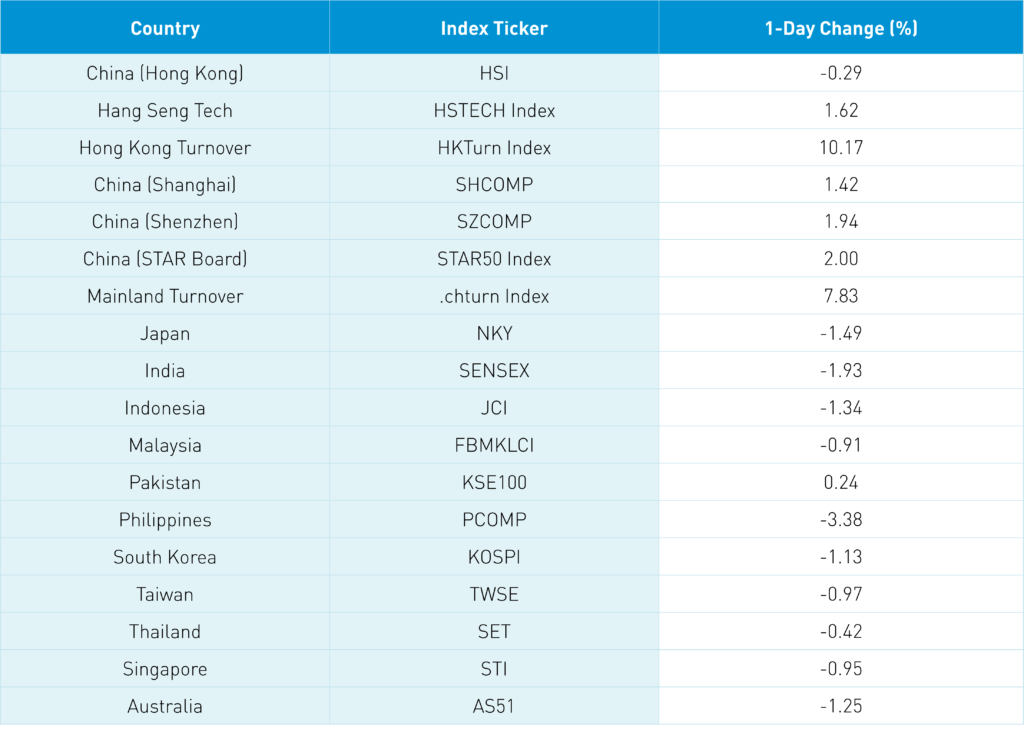

For the week, onshore China: Shanghai Composite gained +3.15% while Shenzhen Composite +2.4%. The STAR Board posted a positive gain of +2.13%, while offshore China: Hang Seng was up +3.43% and the Hang Seng Tech Index gained +9.75%.

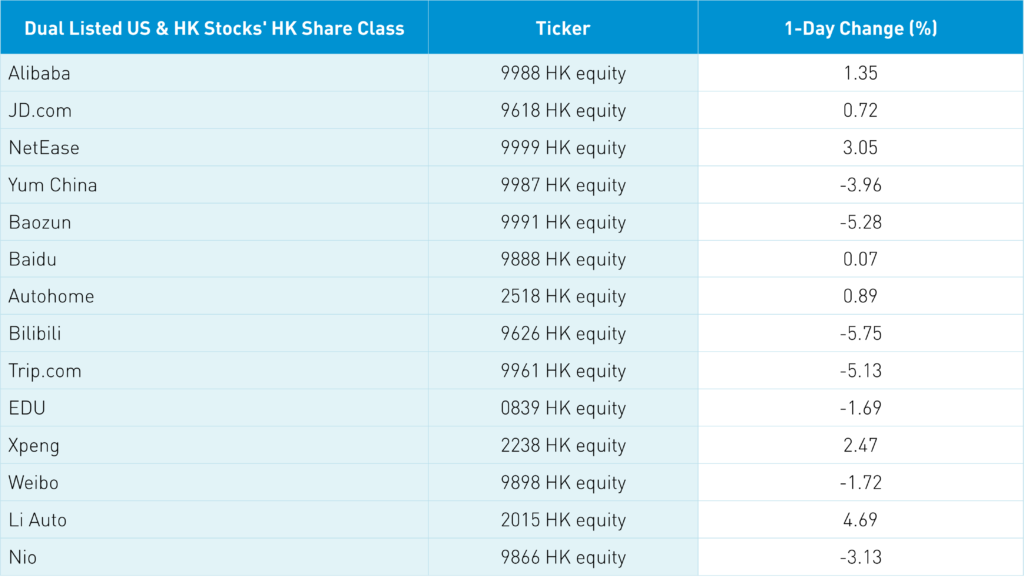

Europe looks to be down about -3% to -4%, and the United States down about -4% for the week. The divergence is interesting considering the Ant IPO news sent Alibaba’s US ADR down -8.13% while Alibaba HK gained +1.35%!

The question arises, why are US investors so pessimistic? Ant Group has received an initial go-ahead from regulators on an IPO, but it may take some time for the company to finally list shares on public markets. Many Hong Kong stocks were similar to Alibaba in that they did not fall as much as Bilibili's US ADR, which was down -14.78%, though its Hong Kong share class was down -5.75%.

Yesterday’s fall in US-listed China ADRs was likely some fast money profit-taking after a strong run since mid-March. Overnight, China reported muted inflation data for May (PPI +6.4% and CPI 2.1%), which gives policymakers further room to ease. Today was also the rebalance day for many Hong Kong and China indices, which led to strong volumes. Foreign investors noticed the performance disparity in the onshore market (SH & SZ) as they bought $1.736B of mainland stocks today, which brings the weekly total to $5.513B.

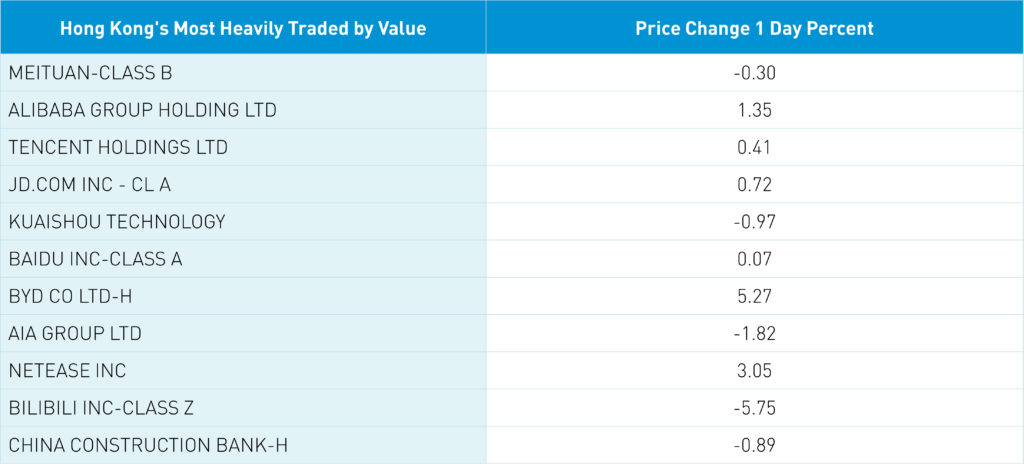

The mainland’s most heavily traded and best performers were foreign and domestic favorites such as BYD (00254 CH), which was up +8.19%, CATL (300750 CH), which was up +5.25% as well as Kweichow Moutai (600519 CH), which gained +2.57%. Mainland investors were also buyers of Hong Kong stocks today though Tencent was sold small and Kuiashou and Meituan were bought small. There was a fair amount of western media coverage on Shanghai and Beijing lockdowns, though the response looks very localized as opposed to the cities being shut down.

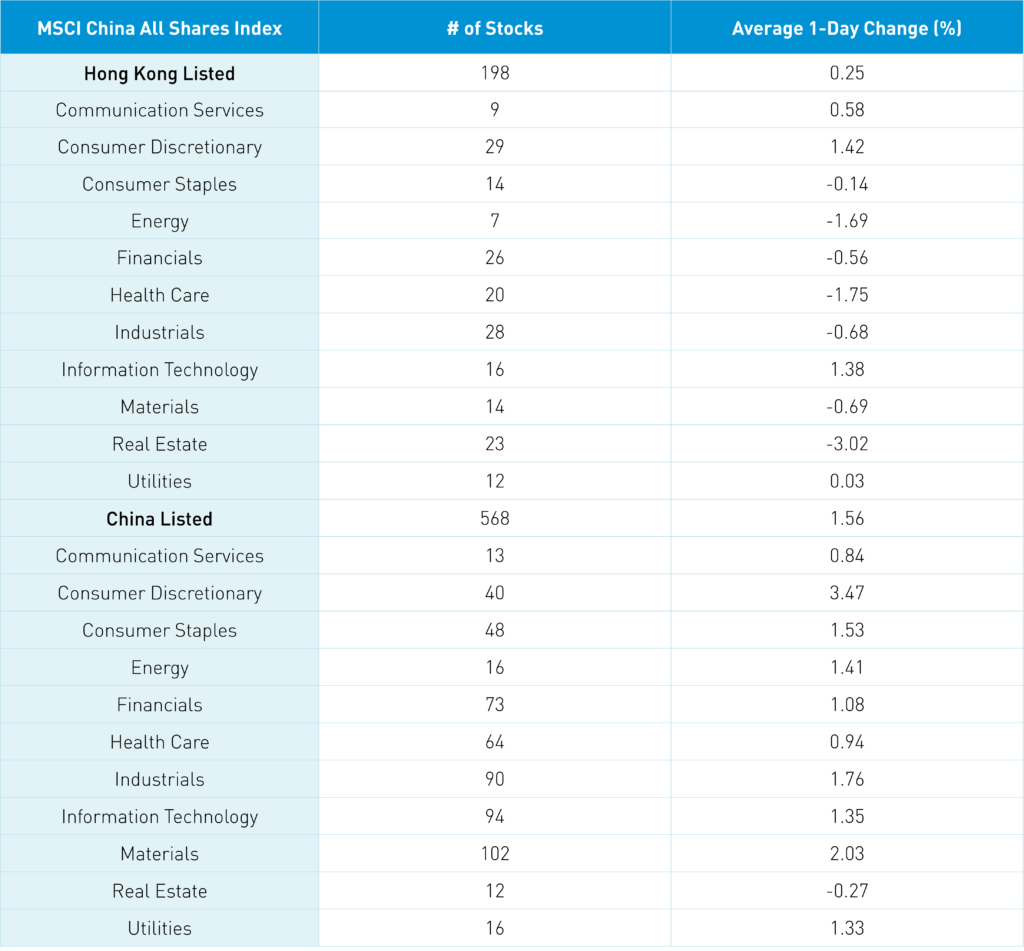

The Hang Seng and Hang Seng Tech diverged positively gaining -0.29% and +1.62% respectively on volume +10.17% from yesterday which is 127% of the 1-year average. 157 stocks advanced while 316 stocks declined. Hong Kong short sale turnover increased 16.11% from yesterday which is 137% of the 1-year average. Growth factors outperformed value factors while small caps outperformed large caps. Top sectors were discretionary +1.425%, tech +1.38%, and communication +0.58% while real estate was down -3.02%, healthcare -1.75% and energy -1.69%. Semis and autos outperformed. Southbound Connect volumes were moderate/high as mainland investors were small/medium sellers of Tencent and buyers of Meituan and Kuiashou.

Shanghai, Shenzhen and STAR Board gained +1.42%, +1.94%, and +2% on volume +7.83% from yesterday which is 97% of the 1-year average. 3,743 stocks advanced while 632 stocks declined. Top sectors were discretionary +3.45%, materials +2.01%, and industrials +1.74% while real estate was the only down sector -0.29%. Auto, EV and lithium plays were outperformers today. Growth factors outperformed today as did small caps. Northbound Connect volumes were moderate/high as foreign investors bought a healthy $1.736B of mainland stocks today. Chinese Treasury bonds gained, CNY was off versus the US $ to 6.69, and copper eased -0.41%.

Last Night’s Exchange Rates, Prices, & Yields

- CNY/USD 6.69 versus 6.67 yesterday

- CNY/EUR 7.11 versus 7.15 yesterday

- Yield on 10-Year Government Bond 2.75% versus 2.76% yesterday

- Yield on 10-Year China Development Bank Bond 2.98% versus 2.98% yesterday

- Copper Price -0.41% overnight