As the World Tightens, China Prepares to Ease

2 Min. Read Time

Key News

Asian equity markets were off following yesterday’s US equity market meltdown, as Australia reopened with a thud while China and Hong Kong outperformed. Both Hong Kong and China were down nearly -2% before rallying later in the day. Mainland investors were buyers of Hong Kong stocks, especially Meituan and, to a lesser degree, Tencent, Kuaishou, and Li Auto.

Tomorrow marks the anticipated 10 bps cut to the Medium-term Lending Facility (MLF) along with the release of May industrial production and retail sales data. Markets are expecting decent May figures, which may allow for 1 & 5 Year Loan Price Rates to be cut again over the weekend.

Foreign investors bought a respectable $585 million worth of Mainland stocks overnight via Northbound Stock Connect. Brokers rallied after the China Securities Regulatory Commission (CSRC) denied reporting that foreign bankers’ pay would be supervised. As I mentioned on Twitter yesterday (@ahern_brendan), US-listed China ADRs were trading at steep discounts to their Hong Kong close yesterday. With Hong Kong not falling and, in some cases, stocks rising, we are seeing a rebound in US-listed China ADRs today.

Hong Kong and China semiconductor stocks were weak following the WSJ article on Congress’ effort to require approval for US investments in China. This is called capital control. The US government will decide what you can and can’t do with your money? It feels like a slippery slope though there appears to be significant pushback on the idea.

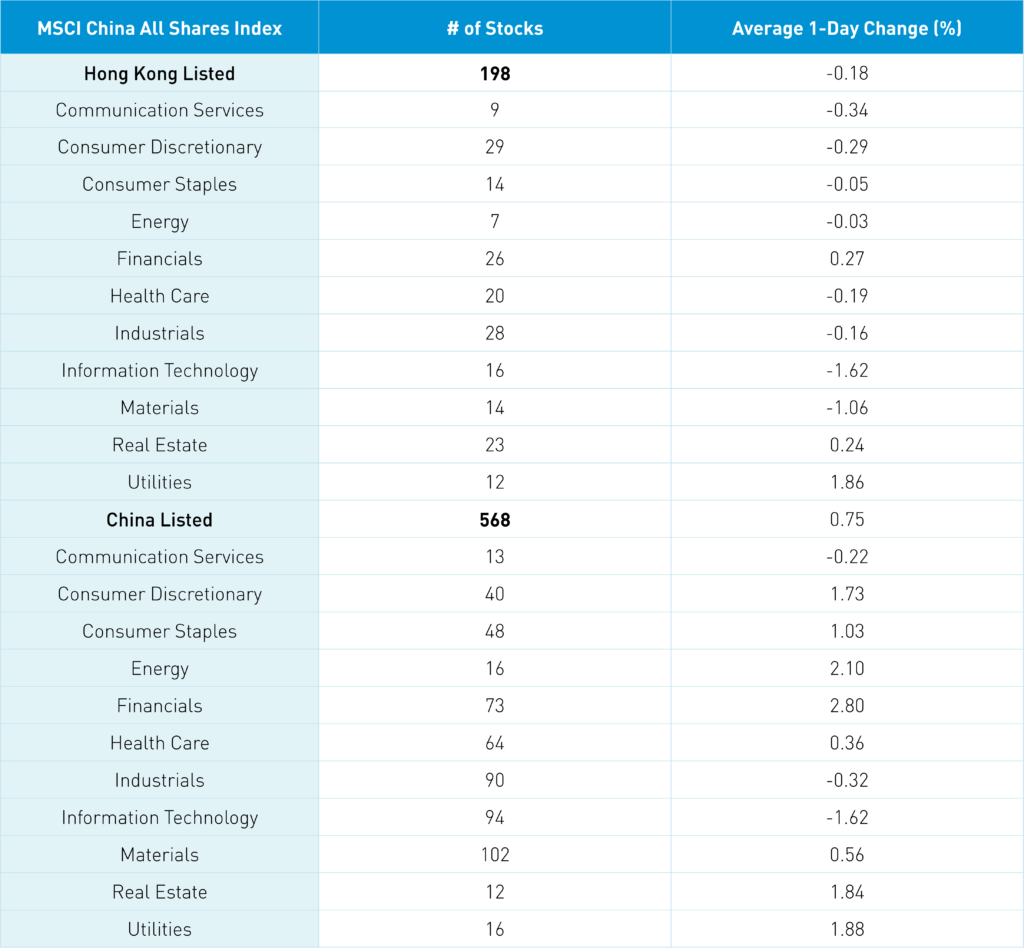

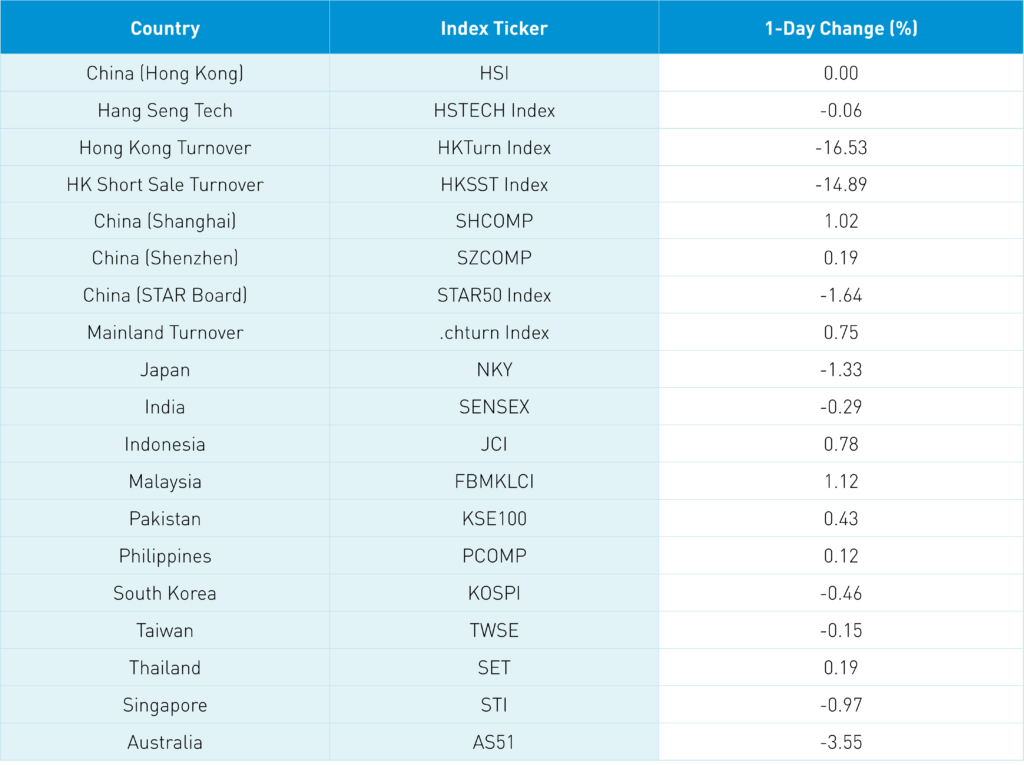

The Hang Seng and Hang Seng Tech were flat and -0.06% on volume -16.53% from yesterday, which is 93% of the 1-year average. There were 157 advancing stocks, while 316 declined. Hong Kong short sale turnover declined by -14.89% from yesterday, which is 104% of the 1-year average. Growth factors were mixed versus value and dividend factors, while large caps outperformed small caps. Top sectors were utilities +1.86%, +0.27% and real estate +0.24% while tech -1.62%, materials -1.06% and communication -0.34%. The top sub-sectors were online education, power companies, and internet medicine, while tobacco, e-cigarettes, and semis were off. Southbound Connect volumes were moderate/high as Mainland investors were buyers of Hong Kong stocks, with Meituan seeing a strong inflow while Kuiashou, Tencent, and Li Auto saw small net buying.

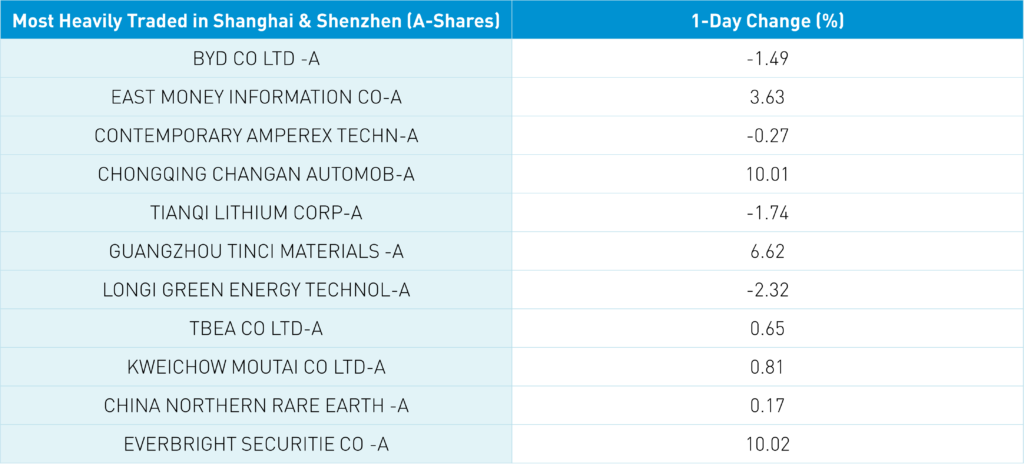

Shanghai, Shenzhen, and the STAR Board closed 1.02%, +0.19%, and -1.64%, respectively, on volume that was +0.75% from yesterday, which is 102% of the 1-year average. 1,499 stocks advanced while 2,890 stocks declined. Value and dividend factors outperformed growth factors, while large caps outperformed small caps by a small margin. Top sectors were financials +2.82%, energy +2.12% and utilities +1.9% while tech -1.6%, industrials -0.31% and communication -0.2%. The top sub-sectors were financial brokers, auto, and lithium, while semis and solar were off. Northbound Stock Connect volumes were moderate as foreign investors bought +$585mm of Mainland stocks today. CNY was off -0.28% versus the US $, yield curve flattened slightly, while copper was off -0.78% (again).

Last Night’s Exchange Rates, Prices, & Yields

- CNY/USD 6.74 versus 6.74 yesterday

- CNY/EUR 7.04 versus 7.05 yesterday

- Yield on 10-Year Government Bond 2.77% versus 2.77% yesterday

- Yield on 10-Year China Development Bank Bond 2.98% versus 2.98% yesterday

- Copper Price -0.78% overnight