Markets Look Forward As Beijing & Guangzhou Are Past COVID Peak

3 Min. Read Time

Key News

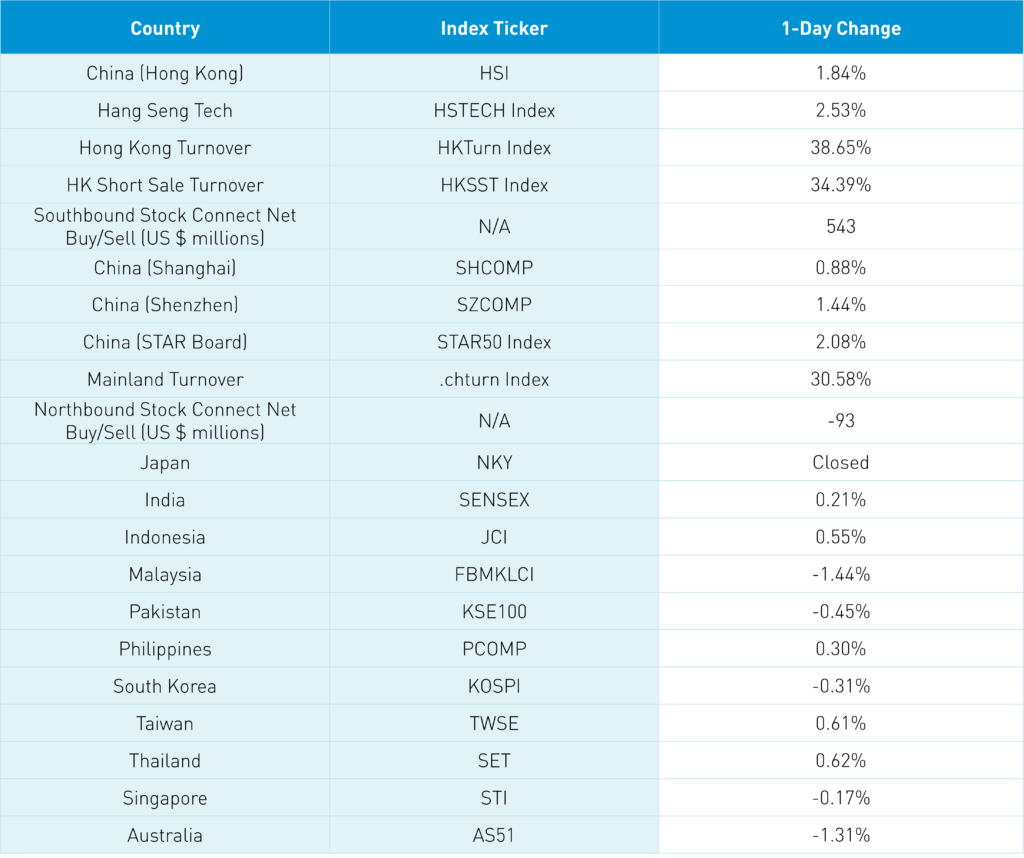

Asian equities were largely higher to start 2023 except for Japan, which took another day off today.

Both Hong Kong and China opened lower with the Hang Seng down -2.41%/Hang Seng Tech down -2.66%/Shanghai down -0.52%/Shenzhen down-0.45% though markets grinded higher across the trading day with growth stocks leading the way. Worth pointing out the very strong breadth on healthy volumes as advancers outpaced decliners significantly in both Hong Kong and China.

Little market-moving news as several significant cities, including Beijing and Guangzhou, appear to be through the peak of their COVID outbreaks with the January 8th foreign traveler restriction removal on the horizon. President Xi mentioned COVID in his New Year speech stating that “we have now entered a new phase of COVID response where tough challenges remain. Everyone is holding on with great grit, and the light of hope is right in front of us.” China is a big country geographically, as several cities are still in the thick of the outbreak. China’s COVID reopening trade against the backdrop of investors allocation is why we believe markets can grind higher. Markets didn’t care about the December Caixin Manufacturing PMI reading of 49 versus expectations of 49.1 and November’s 49.4 as the global economy reduces demand from the world’s factories.

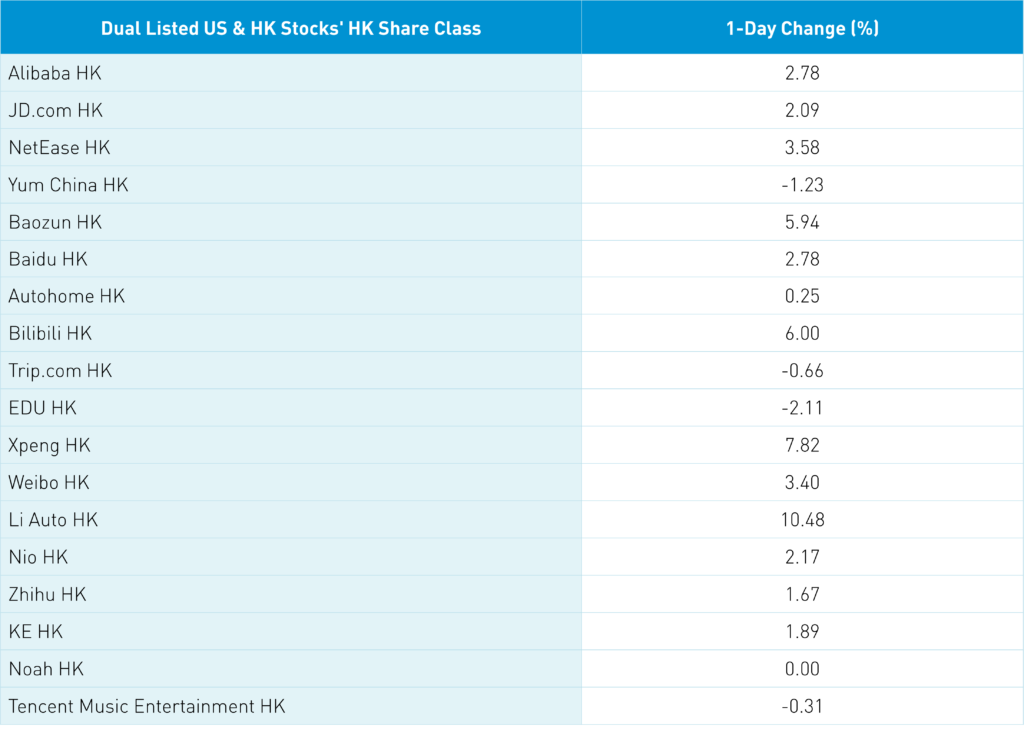

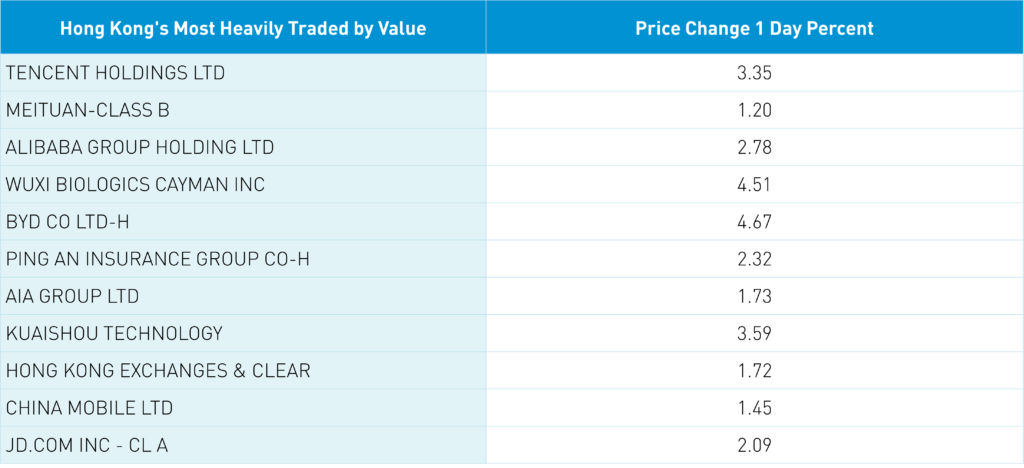

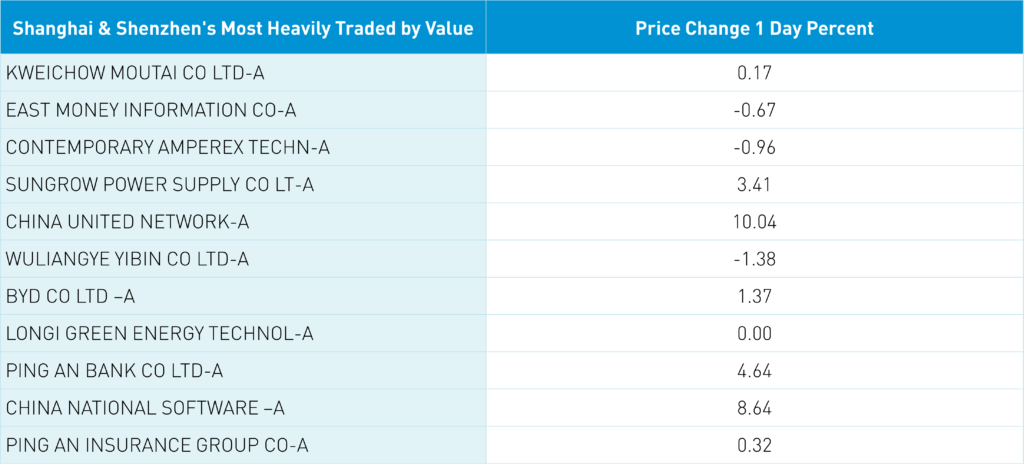

A good start to US China political relations as Secretary of State Antony Blinken and former China Ambassador to the US and new Foreign Minister Qin Gang spoke on New Year’s Day. Hong Kong was led by healthcare, reopening plays such as Macao casinos, airlines, and restaurants. EVs climbed higher as Li Auto HK gained +10.48%, Xpeng HK +7.82%, and global EV leader BYD HK +4.67% on strong December sales with Nio HK lagging +2.17%. Hong Kong internet plays had a strong day with Hong Kong’s most heavily traded by value Tencent +3.35%, Meituan +1.2%, and Alibaba HK +2.78%. Hong Kong short volume has picked up though remains moderate as Alibaba’s short turnover jumped to 21% of total turnover from Friday’s 8%. Growth stocks led Mainland China higher as the Shenzhen gained +1.44% versus the Shanghai’s +0.88%. Large cap growth stocks favored by both domestic and foreign investors were largely higher though a few prominent names were off slightly. Foreign investors sold -$93 million of Mainland stocks. CNY fell slightly versus the dollar after a strong gain into year end.

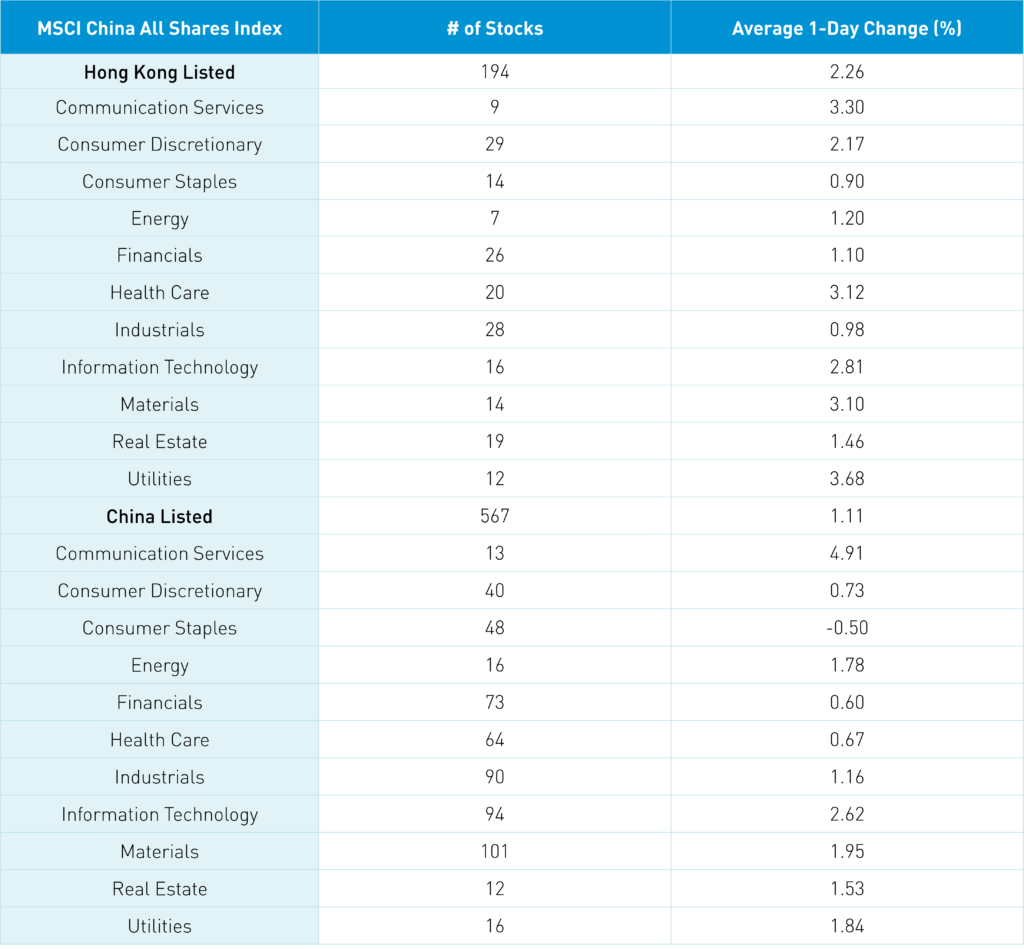

The Hang Seng and Hang Seng Tech gained +1.84% and +2.53% on volume +38.65% from Friday which is 96% of the 1-year average. 396 stocks advanced while 88 stocks declined. Main Board short turnover increased +34.18% from Friday which is 90% of the 1-year average as 16% of turnover was short turnover. Growth and value factors were mixed as large caps outpaced small caps. All sectors were positive with utilities +3.68%, communication +3.3% and healthcare +3.12%. Top sub-sectors were autos, food and software while household/personal products was the only negative sub-sector. Southbound Stock Connect volumes were light/moderate as mainland investors bought $543mm of HK stocks with Tencent a moderate buy, Kuaishou a small net buy, and Meituan a moderate net sell.

Shanghai, Shenzhen, and STAR Board gained +0.88%, +1.44%, and +2.08% respectively on volume +30.58% from Friday which is 85% of the 1-year average. 4030 stocks advanced while 665 stocks declined. All sectors were positive except staples -0.46% with communication up +4.95%, tech up +2.66%, and materials finishing higher +1.99%. Top sub-sectors were telecom, software, and computer hardware while airports, soft drinks, and restaurants were among the worst. Northbound Stock Connect volumes were moderate/light as foreign investors sold -$93 million of Mainland stocks. CNY fell -0.23% versus the US dollar to 6.91, Treasury bonds rallied, and copper fell -0.68%.

Major Chinese City Mobility Tracker

Unfortunately, we ran into a data issue this morning. Apologies! Once available we will post on Twitter via @ChinaLastnight.com and @ahern_brendan

Last Night's Performance

Last Night’s Exchange Rates, Prices, & Yields

- CNY per USD 6.91 versus 6.90 Friday

- CNY per EUR 7.28 versus 7.36 Friday

- Yield on 10-Year Government Bond 2.82% versus 2.84% Friday

- Yield on 10-Year China Development Bank Bond 2.97% versus 3.01% Friday

- Copper Price -0.68% overnight