President Xi Addresses Domestic Consumption In Speech

3 Min. Read Time

Key News

Asian equities had a strong day following US stocks’ positive move yesterday, as the Philippines had a very strong day in advance of the Fed's rate decision today, which will be followed by rate hike decisions by the ECB and BOE.

Malaysia was closed for Federal Territory Day, which celebrates "the formation of the Federal Territory of Kuala Lumpur in 1974,” according to Google. President Xi attended and spoke at the CPC Central Committee, which focused on “accelerating the construction of new development pattern” i.e., DOMESTIC CONSUMPTION. I took the artistic license of highlighting where investors should be focused i.e., DOMESTIC CONSUMPTION. The speech also focused on “self-reliance and self-improvement in science and technology”. This was front page news in China AFTER the market close.

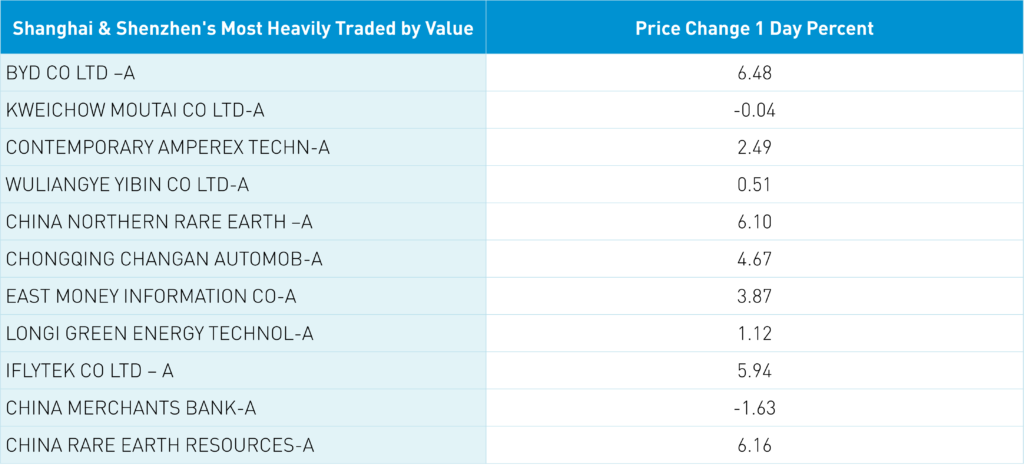

We are seeing a rebound today in US-listed Chinese stocks due to a nice Hong Kong rally overnight led by Hong Kong’s most heavily traded stocks: Tencent, which gained +0.73%, Meituan, which gained +3.15%, Alibaba, which gained +2.23%, and BYD, which gained +6.12% after yesterday’s massive profit spike, which we discussed yesterday (net income expected to rise +458% in 2022 versus 2021!). BYD’s strong results lifted electric vehicles (EVs) and autos in both Hong Kong and Mainland China as Li Auto gained +9.37%, XPeng gained +10.34%, Geely Auto gained +5.06%, and NIO gained +6.33%.

Baidu HK jumped +8.99% as Asian investors cheered their announcement on launching a ChatGPT like search functionality. Worth pointing out that Hong Kong mid-morning dipped negative but rallied over the course of the day, a sign that investors maybe bought the dip as the Hang Seng Index closed back above the big meaningless round number 22K level at 22,072.

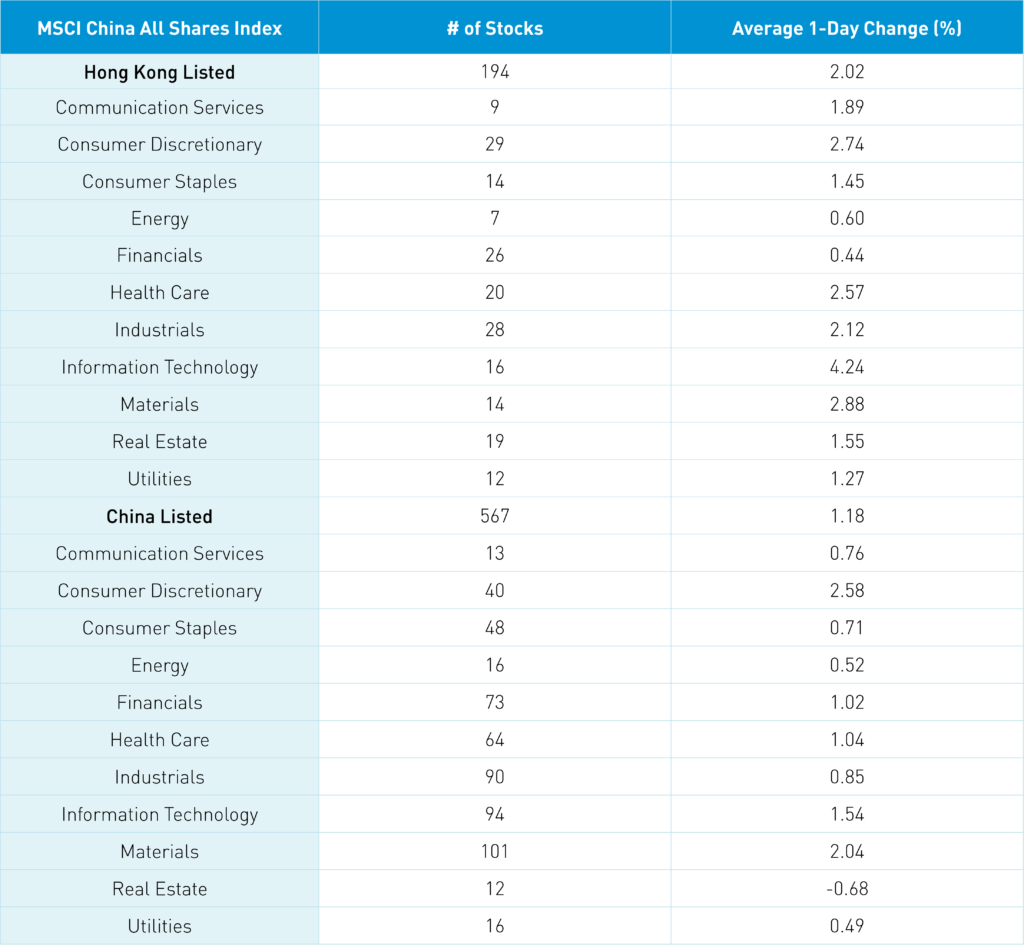

All sectors were positive in Hong Kong with only one negative sector in China with very strong breadth/advancers versus decliners. Hong Kong Main Board short turnover did increase with 20% of total Main Board turnover short. This is the first time that short turnover was 20% or more since October 18th, 2022. We also had another net sell day of Hong Kong stocks from Mainland investors via Southbound Stock Connect.

Fair amount of chatter about a Goldman Sachs research report highlighting that hedge funds are overweight China while long only/mutual funds are still underweight China. Remember hedge funds are traders/they don’t marry their positions. Mutual funds appear to be far more skeptical of this rebound. Ouch! Think about that big pension fund that cut its China weight back in October. Imagine what their Q1 recap meeting will be like! “So how did we do by cutting our China weight in half? Ugh…”. Maybe you shouldn’t invest emotionally! Hedge funds are doing it though, the China underweight is why the pain trade is higher in my opinion.

Mainland China’s nice rebound was led by growth stocks as foreign investors bought $1.034 billion of Mainland stocks via Northbound Stock Connect. News that a big pension plan has cut its private equity investments in China which may explain where all this Northbound Connect flow is coming from. Staying in big liquid mega/large caps makes sense versus the lock ups associated with private equity. On Twitter, @ahern_brendan, I put a nice chart of Shanghai and Shenzhen yesterday. Looks good!

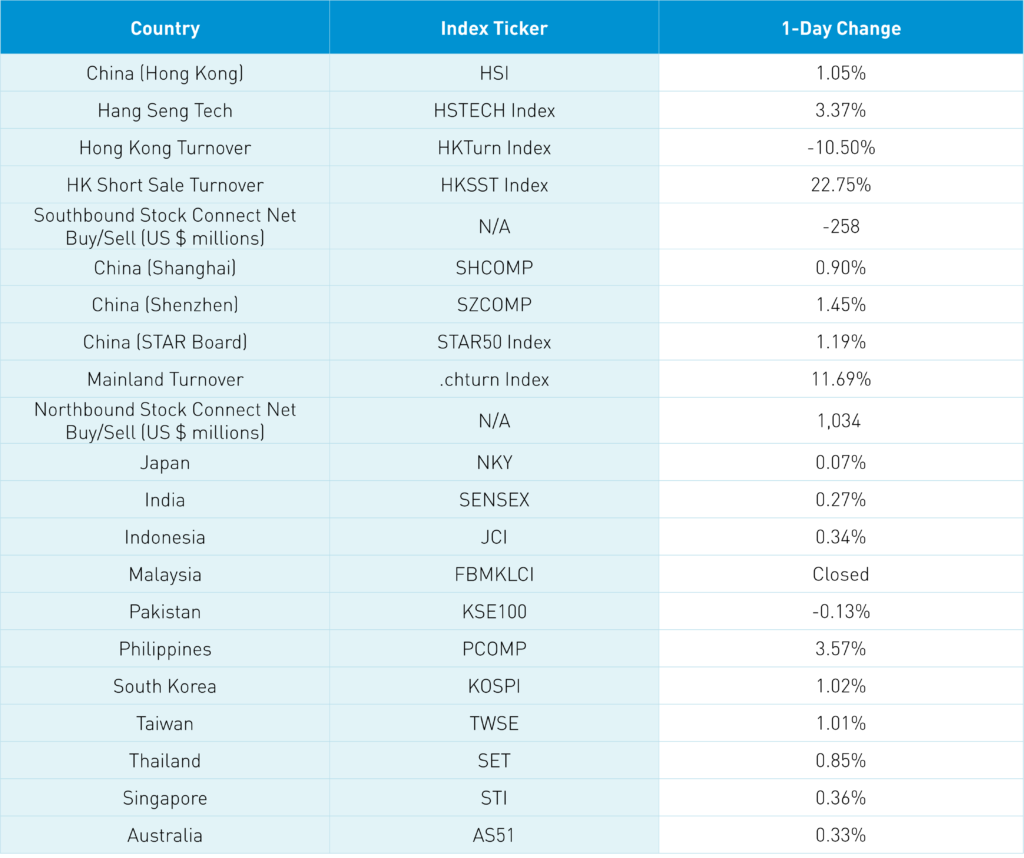

The Hang Seng and Hang Seng Tech gained +1.05% and +3.37% respectively on volume -10.5% from yesterday which is 124% of the 1-year average. 440 stocks advanced while 57 stocks declined. Main Board short turnover increased +22.68% from yesterday which is 142% of the 1-year average as 20% of turnover was short turnover. Growth factors outperformed value factors as small caps outperformed large caps. All sectors were positive with tech gaining +4.24%, materials finishing higher +2.88%, and discretionary up +2.75% while financials +0.44%. Top sub-sectors were auto, semis, and technical hardware/equipment while household products, banks, and insurance were among the worst. Southbound Stock Connect volumes were moderate/high as Mainland investors sold -$258 million of Hong Kong stocks with Tencent a small net sell though again a big decline from the last two days, Meituan a strong buy, Xpeng a small net sell, Li Auto a small net buy, and Kuaishou a very small net buy.

Shanghai, Shenzhen, and STAR Board gained +0.9%, +1.45%, and +1.19% respectively on volume +11.69% from yesterday which is 111% of the 1-year average. 3,951 stocks advanced while 539 stocks declined. All sectors were positive except real estate finishing lower -0.68%, with discretionary gaining +2.58%, materials up +2.05%, and tech finishing higher +1.55%. Top sub-sectors were auto, diversified financials, and office supplies while power generation equipment, banking, and construction machinery lagged. Northbound Stock Connect volumes were moderate/high as foreign investors bought $1.034 billion of Mainland stocks with mega/large caps stocks favored. CNY gained +0.23% versus the US dollar closing at 6.739, Treasury bonds sold off slightly, Shanghai Copper +0.16%, while Shanghai Steel Rebar closed lower -1.39%.

Major Chinese City Mobility Tracker

Back to work!

Last Night's Performance

Last Night's Exchange Rates, Prices, & Yields

- CNY per USD 6.73 versus 6.75 yesterday

- CNY per EUR 7.34 versus 7.32 yesterday

- Yield on 10-Year Government Bond 2.91% versus 2.89% yesterday

- Yield on 10-Year China Development Bank Bond 3.07% versus 3.05% yesterday

- Copper Price +0.16% overnight