Consumer Rebound Rolls On, Week in Review

4 Min. Read Time

Week in Review

- Asian equities started the week off lower and then rallied higher in the middle of the week as central bank rate hikes dominated market news, though China maintained its easing stance.

- January Manufacturing PMI, reported on Monday, was 50.1 versus expectations of 50.1 and December’s 47, while the Non-manufacturing (Service) PMI was 54.4 versus expectations of 52 and December’s 41.6. Both indicated an expansion, which was more pronounced in services.

- Baidu announced Tuesday that it would be rolling out a Chat GPT-like AI search feature.

- China’s onshore currency was relatively stable this week versus the US dollar, despite the latter's rise against a basket of other currencies.

Friday’s Key News

Asian equities had a strong night as India rebounded. Concerns of Adani’s implosion leading to a broader crisis lessened, though Mainland China and Hong Kong underperformed. Asia saw impressive equity performance overnight as Amazon, Apple, and Alphabet’s underwhelming earnings did not weigh on regional sentiment.

We had our first day of net sales by foreign investors via Northbound Stock Connect since January 3rd. Despite the sale of a net -$630 million worth of Mainland stocks today, foreign investors bought over +$5 billion worth of Mainland stocks for the week. There has been significant buzz about global investors’ allocation to Chinese stocks as many strategists have published research reports on the topic. I believe hedge funds, due to their trading focus, pivoted to go long China months ago. Meanwhile, I believe long-only funds, active mutual funds, and institutional investors are still underweight the space due to skepticism and scar tissue. Removing these underweights will take time as Q1 investment committee meetings are not until April. Yes, we are seeing a pause and a pullback, but this should provide some of those investors an opportunity to buy the dip.

Q4 financial results and, more importantly, their Q1 and 2023 outlooks will be released later this month, which could also be an important catalysts for certain investors to reenter the market. US stocks account for 60% of the MSCI All Country World Index, while Japan accounts for 5.5%, the UK accounts for 3.8%, and China accounts for only 3.6%, as of 12/31/2022. This reality also accounts for a great deal of underweighting China. Perhaps the next decade will look different then the past decade?

Hong Kong-listed internet stocks declined overnight, though not as much as their US-listed counterparts fell yesterday. Hong Kong’s most heavily traded stocks by value today were Tencent, which gained +0.52%, Alibaba, which fell -2.66%, and Meituan, which fell -2.15% as breadth was awful. The Hang Seng Index closed below 22,000 at 21,660, as the 21,500 level is an important area of support to watch.

US Secretary of State Antony Blinken postponed his trip to Beijing to a later date after the sighting of a balloon that originated in China flying over Montana. According to official statements, the balloon was nonmilitary and conducting climate research. Beijing acknowledged the intrusion into US airspace that was not on the vessel’s initial manifesto.

Shanghai Mayor Gong Zheng visited Ant and Meituan’s Shanghai offices in another sign of government support for internet companies due to their role in consumption.

The January Caixin Services PMI increased to 52.9 compared to an expected 51.1 and December’s 48, another sign that China’s consumption economy is rebounding following the end of the zero COVID policy. Why? Remember that, earlier this week, the January Caixin Manufacturing PMI was reported at 49.2, indicating a decline month over month. Consumption must be picking up the slack in the economy.

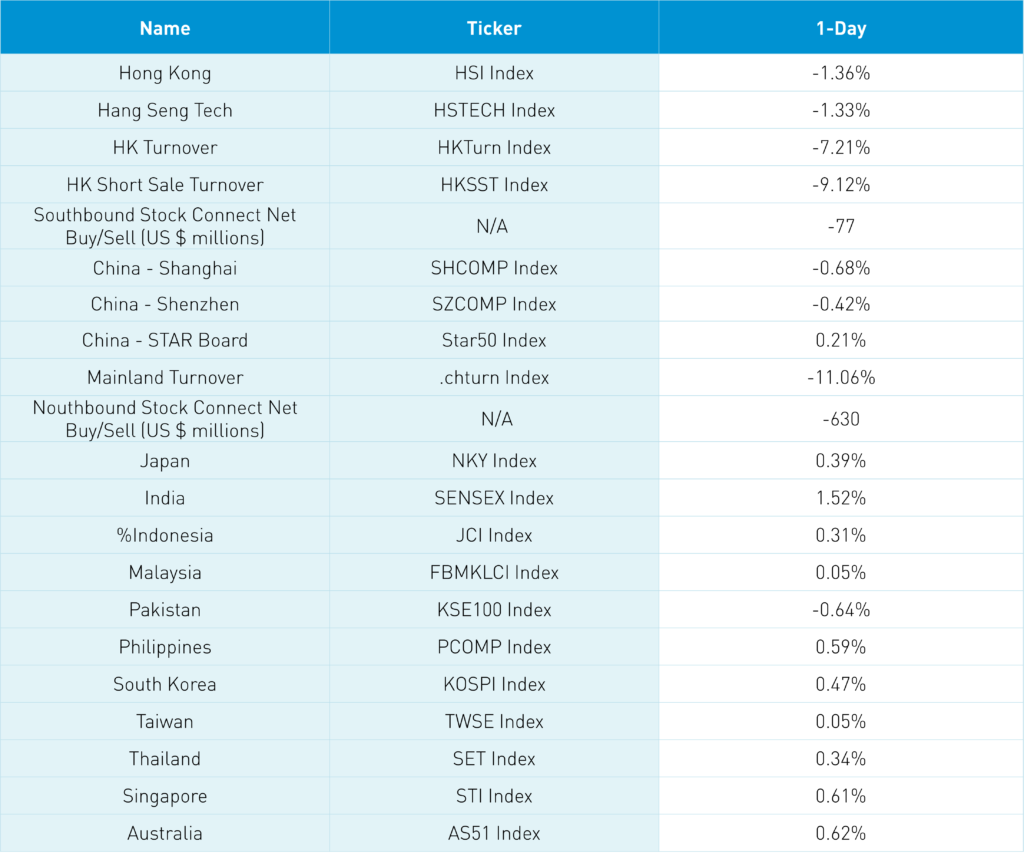

The Hang Seng and Hang Seng Tech indexes eased throughout the session to close -1.36% and -1.33%, respectively, on volume that declined -7.21% from yesterday, which is 103% of the 1-year average. 114 stocks advanced while 385 stocks declined. Main Board short sale turnover fell -9.13% from yesterday, which is 90% of the 1-year average, as 15% of turnover was short turnover. Growth and value factors were both weak as small caps “outperformed” large caps. All sectors were negative as real estate fell -2.41%, energy fell -2.38%, and materials fell -2.24%. The only positive subsector was media, while energy, retail, and autos were among the worst. Southbound Stock Connect volumes were light as mainland investors sold -$77 million worth of Hong Kong stocks as Kuaishou was a very small net sale, Tencent was a moderate sale, and Meituan was a large net sale.

Shanghai, Shenzhen, and the STAR Board diverged to close -0.68%, -0.42%, and +0.21%, respectively, on volume that decreased -11.06% from yesterday, which is 101% of the 1-year average. 1,736 stocks advanced while 2,882 stocks declined. Growth and value factors were both off, while small caps outpaced large caps. Communication was positive, gaining +0.43%, and tech was flat. Meanwhile, real estate fell -1.92%, consumer discretionary fell -1.69%, and materials fell -1.49%, making up the worst performing sectors. The top-performing subsectors were software, internet, and aerospace/military, while insurance, autos, and precious metals were among the worst. Northbound Stock Connect volumes moderate as foreign investors sold -$630 million worth of Mainland stocks as Kweichou Moutai was a moderate net sell, China Merchants Bank was a small buy, Longi and Ping An were very small sells. CNY gained slightly versus the US dollar, Treasury bonds rallied, while Shanghai copper and steel fell -0.46% and -1.39%, respectively.

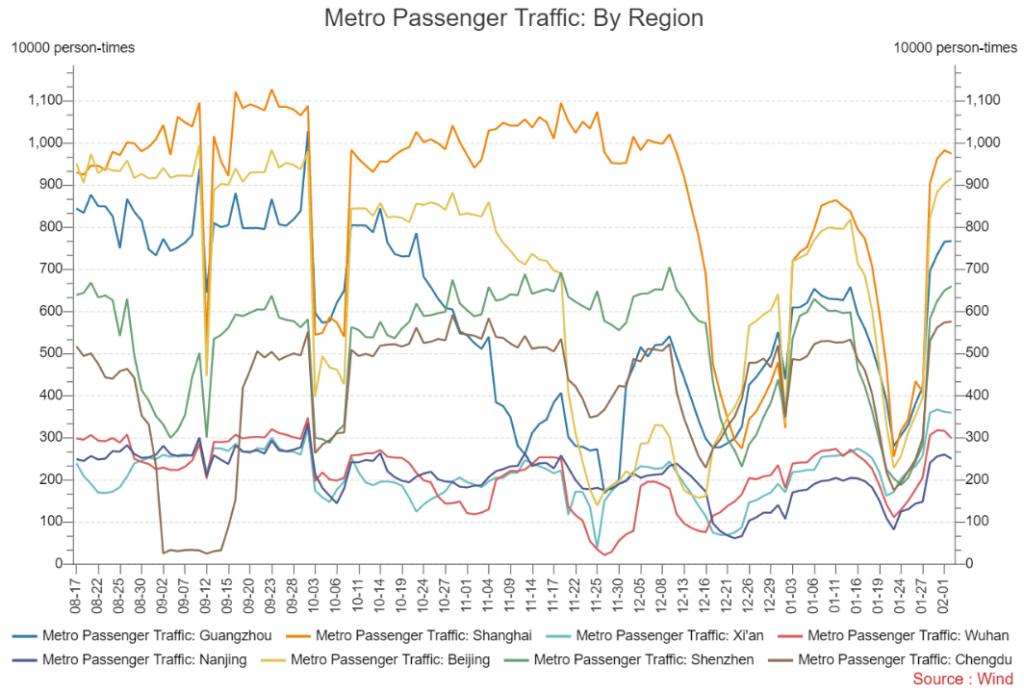

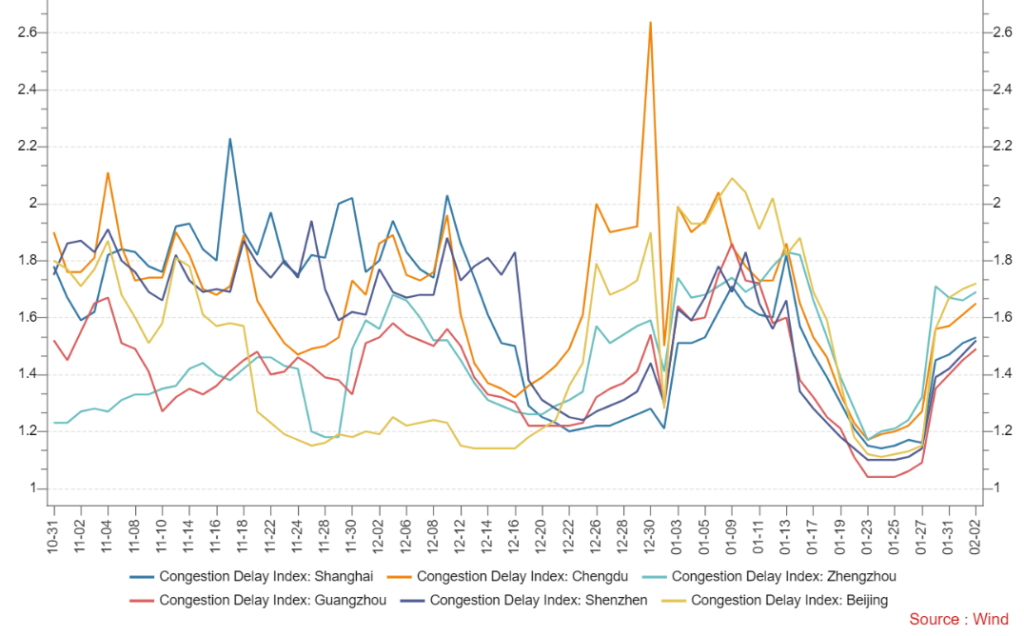

Major Chinese City Mobility Tracker

Life is back to normal in most Chinese cities.

Last Night's Performance

Last Night’s Exchange Rates, Prices, & Yields

- CNY per USD 6.77 versus 6.73 yesterday

- CNY per EUR 7.35 versus 7.35 yesterday

- Yield on 1-Day Government Bond 1.29% versus 1.33% yesterday

- Yield on 10-Year Government Bond 2.89% versus 2.90% yesterday

- Yield on 10-Year China Development Bank Bond 3.06% versus 3.06% yesterday

- Copper Price -0.46% overnight