March EV Deliveries Deliver, Macau’s Mojo

4 Min. Read Time

Key News

Asian equities were higher as Taiwan closed for Children’s Day which is “… celebrated annually on April 4, emphasizes the importance of future generations and endeavors to promote their general wellbeing.”

Tech stocks were strong performers in Hong Kong, where the sector gained +1.09% and Mainland China, where the sector gained +3.37%, as China’s security review of Micron lifted local semiconductor names. Political rhetoric and tit-for-tat policies disrupt established business relationships, which, in turn, create voids that get filled.

Macau gaming stocks including Sands China, which gained +6.96% and Wynn Macau, which gained +8.79%, ripped higher as March gaming revenue increased by nearly +247% year-over-year as the gambling hub benefits from China and broader Asia’s reopening. Unfortunately, casino stocks are not considered part of the MSCI China Index due to their Hong Kong domicile!

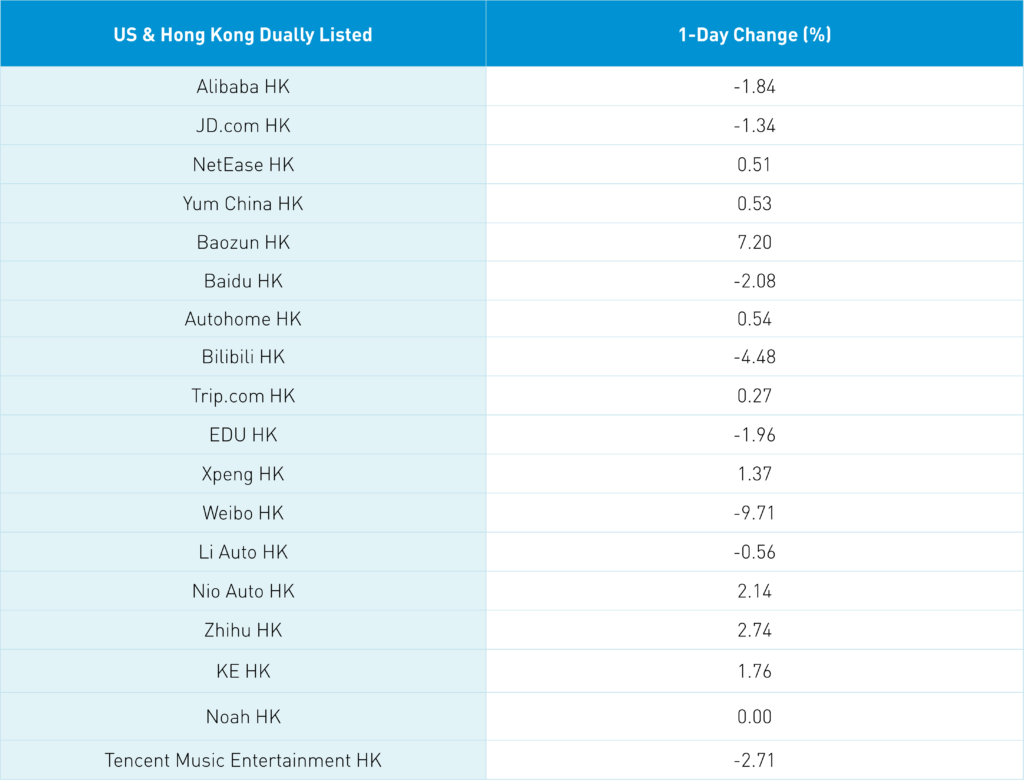

Hong Kong-listed electric vehicle (EV) names were largely higher as March deliveries were released as month-over-month (MoM) percent changes. BYD sold +6.9% more vehicles last month (207,080 vehicles delivered) and its stock gained +0.70%, Li Auto sold +25% more vehicles last month (20,823 vehicles delivered) and its stock gained +0.56%, Xpeng gained +1.37% on a MoM delivery increase of +16.5% (7,002 vehicles delivered), and NIO gained +2.14% despite a MoM decline in deliveries of -14.6% (10,378 vehicles delivered).

Real estate was the best-performing sector in Hong Kong, where it gained +1.96%, and the top sector in Mainland China, where it gained +2.23% as the left-for-dead sector/”China’s Lehman Moment” posted strong sales data in March. Mainland China volumes were Strong, up +31.76% from Friday, which is 140% of the 1-year average. Maybe Chinese investors in China are waking up to the economy’s pick up leading to animal spirits? Hong Kong volumes, including short volume, were light and will likely remain light this week due to market holidays. Mainland investors bought a very healthy $667 million worth of Hong Kong stocks today as Tencent was a moderate net buy.

There were a few items that did not matter overnight, though are becoming headlines this morning. Energy stocks in Hong Kong and Mainland China were off slightly as OPEC’s supply cut was a yawn. Also, the morning release of the Caixin Manufacturing PMI was another yawn at 50 versus expectations of 51.4 and February’s 51.6. Last week, we had the release of the “official” PMI, which surveys large companies, while the Caixin PMI surveys smaller companies, though exporters face the headwind of a slowing global economy. CNY is off slightly versus the US dollar.

The Hang Seng and Hang Seng Tech indexes were mixed to close +0.04% and -0.03%, respectively, on volume that was down -14.34% from Friday, which is 100% of the 1-year average. 254 stocks advanced while 234 declined. Main Board short turnover increased +4.15% from Friday, which is 91% of the 1-year average as 16% of turnover was short turnover. Growth factors outperformed value factors as large caps outpaced small caps. The top-performing sectors were real estate, which gained +1.96%, technology, which gained +1.09%, and communication services, which gained +0.23%. Meanwhile, utilities fell -2.84%, discretionary fell -1.7%, and materials fell -1.35%. The top-performing subsectors were semiconductors, consumer services, and real estate. Meanwhile, media, food/staples, and retailers were the worst. Southbound Stock Connect volumes were moderate/high as Mainland investors bought $667 million worth of Hong Kong stocks as Tencent was a moderate/strong net buy, Kuiashou was a small net buy, and Meituan was a small net sell.

Shanghai, Shenzhen, and STAR Board gained +0.72%, +1.14% and +4.16% on volume +31.76% from Friday which is 140% of the 1-year average. 3,043 stocks advanced while 1,600 stocks declined. Growth and value factors were mixed as small caps outpaced large caps. Top sectors were communication +4.25%, tech +3.36% and real estate +2.19% while healthcare -1.48%, utilities-0.96% and energy -0.87%. Top sub-sectors were computer hardware, internet, and software while marine/shipping, precious metals and motorcycles were the worst. Northbound Stock Connect volumes were high as foreign investors bought $84mm of mainland stocks. CNY eased versus the US dollar. Treasury bonds sold off while Shanghai copper and steel were lower.

Book Review - Shut Up & Keep Talking by Bob Pisani, CNBC Correspondent

Have you ever eaten at a Kona Grill? I have not, though I owned the stock personally a long time ago based on a recommendation from a friend. The restaurant chain’s thesis at the time was a diverse menu that could provide a one stop for everyone in the family ranging from steaks to sushi to seafood. Bob Pisani’s book Shut Up & Keep Talking reminded me of Kona Grill as the book provides a diverse menu of delicious topics that impacted Bob’s career and investors over the last thirty plus years. The book starts with the evolution of trading at the New York Stock Exchange (NYSE) from physical market makers to electronic trading along with a look at the cast of characters at the NYSE such as Art Cashin. It provides a very good overview on how market structure has evolved dramatically with significant consequences, both positive and negative, for companies, exchanges, employees, and investors. I really enjoyed the deep dive on forecasting, behavioral finance, and academic investing scholars’ impact on Bob’s thinking and investing. His examination of Isaiah Berlin’s essay on forecasting titled The Hedgehog and the Fox and Philip Tetlock’s book Superforecasting were just brilliantly written. Hedgehogs only look out of a hole, i.e. an ideologue, versus a fox, which is always looking around, i.e. new ideas and learning. Of course, there are the celebrities and NYSE interviews too. When you think you are done, the Appendix has three bonus sections on ETFs and the Origin of Indexing, Understanding Bubbles, and Bob’s 58 Maxims on Life, Television, and the Stock Market. Bob is a self-admitted “Bogle-head” due to John Bogle’s influence on him. I am showing some personal bias, but no mention of either Barclays Global Investors nor iShares? Yes, Bob looks at the first index strategy run by Wells Fargo Investment Management, which became Barclays Global Investors, which was subsequently bought by BlackRock in the Great Financial Crisis (GFC). It was likely a miss by BGI that we didn’t speak to Bob! All told, a very well written, thoughtful, entertaining, and educational read. Kudos to Bob!

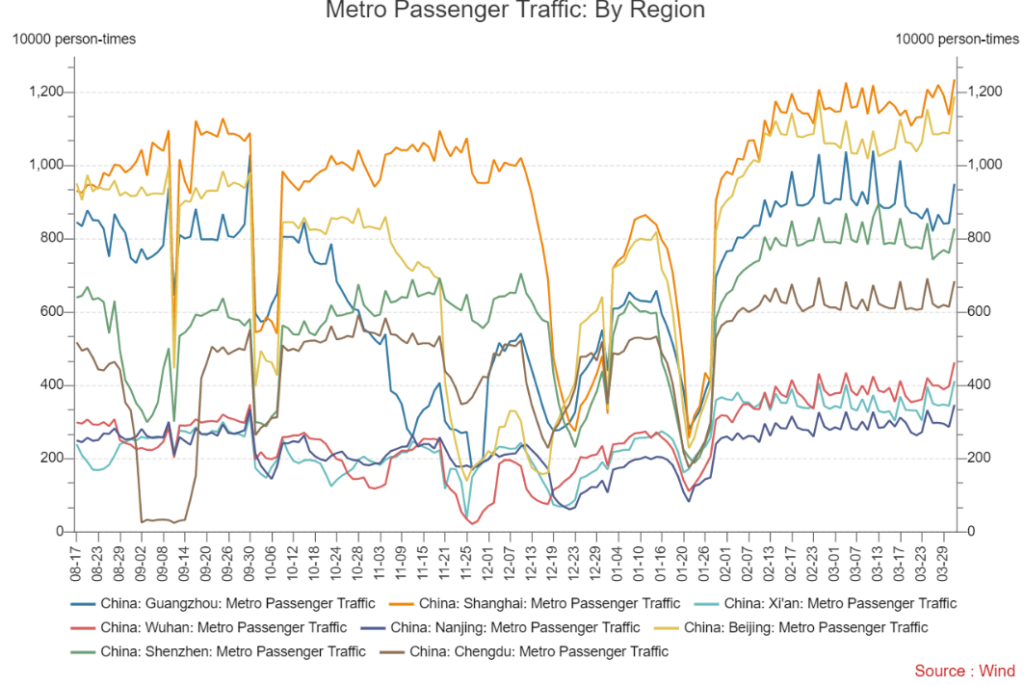

Major Chinese City Mobility Tracker

Last Night's Performance

Last Night’s Exchange Rates, Prices, & Yields

- CNY per USD 6.88 versus 6.87 Friday

- CNY per EUR 7.49 versus 7.46 Friday

- Yield on 1-Day Government Bond 1.55% versus 1.59% Friday

- Yield on 10-Year Government Bond 2.86% versus 2.85% Friday

- Yield on 10-Year China Development Bank Bond 3.03% versus 3.03% Friday

- Copper Price -0.10% overnight

- Steel Price -1.60% overnight