Mainland Marches On

3 Min. Read Time

Key News

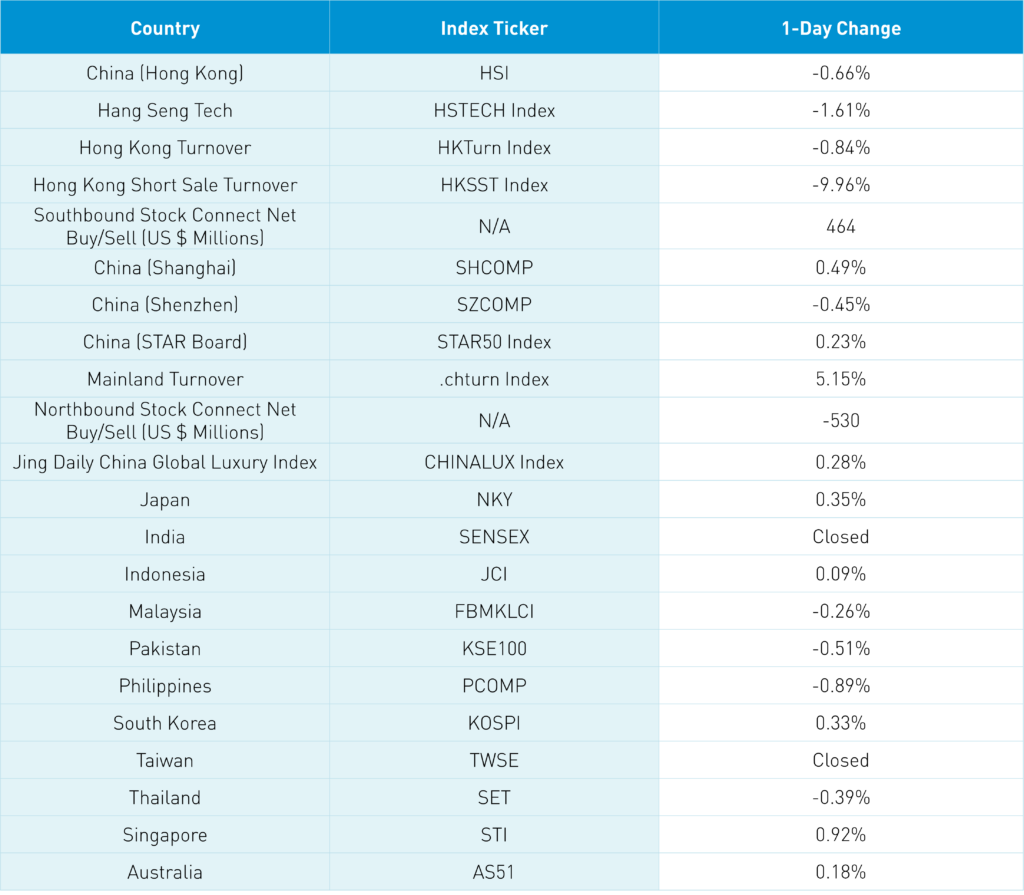

Asian equities were largely higher/mixed on lower volume while Taiwan and India were off on holiday.

There are many market holidays this week which explains the light volumes in the region which can lead to more volatility. It was interesting that Mainland China was mixed/higher but on very high volumes, reaching 146% of the 1-year average. Both the Shanghai and Shenzhen appear to be in intermediate uptrends with the Shanghai outperforming the Shenzhen. Shanghai’s mega/large cap State Owned Enterprises (SOEs) are outperforming Shenzhen’s large/mid/small cap private companies. SOE reforms are a factor but also sector composition. Another factor is China’s consumer confidence is rising off the lows posted during the April Shanghai lockdown (86.7 from March’s 113) and after zero-COVID was removed in October, it led to many people falling ill (85.5). January’s 91.2 was followed by February’s 94.7.

Overnight, the PBOC released a survey of 20,000 urban bank depositors across China indicating that in Q1, consumption and investing both increased slightly from Q4 2022 while the savings rate decreased slightly. Foreign investors sold -$530 million of Mainland stocks via Northbound Stock Connect, likely driven by the holidays, but the potential for headlines on Taiwan’s President meeting with House Speaker McCarthy tomorrow remains. Worth noting that France’s President Macron will visit China later this week while Australia’s Prime Minister is expected to visit in the fall. Worth pointing out that due to elections in Taiwan next year, the Taiwan President, who is in her final term, doesn’t want McCarthy to visit Taiwan because it helps her political opposition who won handily after Pelosi’s visit.

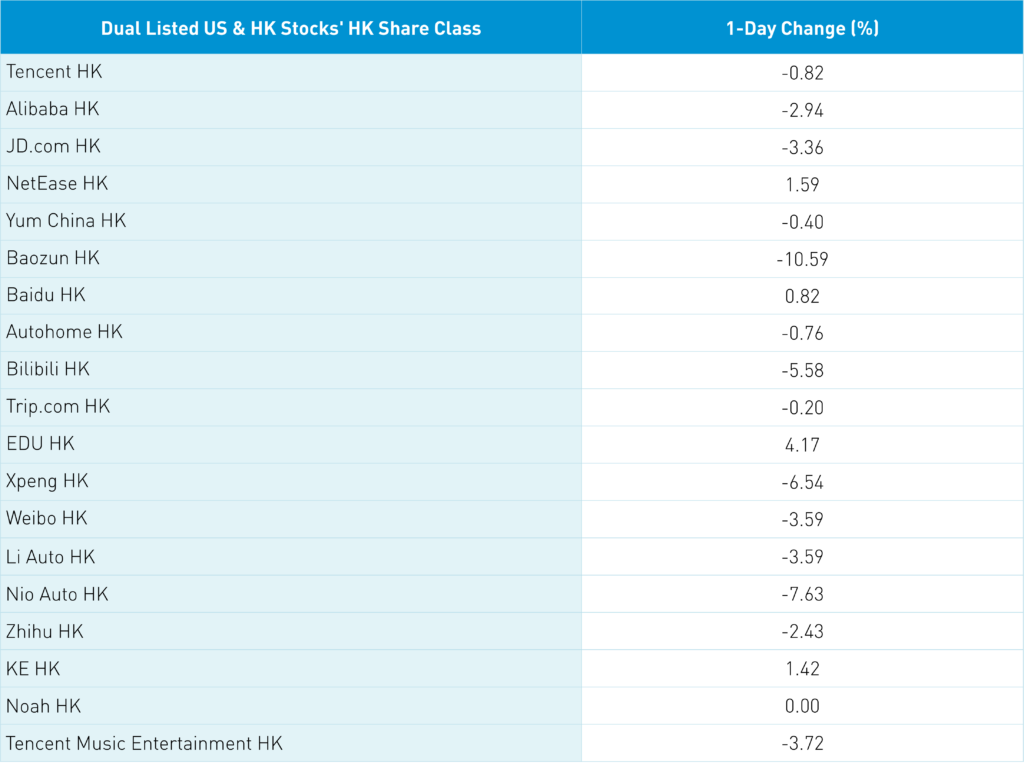

Hong Kong was off led by Hong Kong’s most heavily traded SenseTime which gained +12.8% on ChatGPT launch rumors, Meituan closing lower -4.36% as a major sell via Southbound Stock Connect due to Tencent’s spin off, Tencent closed at -0.82% despite buying 910,000 of its own stock for the 7th day in a row, and Alibaba HK fell -2.94% despite increased enthusiasm for the corporate restructuring. Alibaba owns a piece of SenseTime as an FYI. EVs were off in Hong Kong with BYD closing lower -1.82%, XPeng -6.54%, Li Auto -3.95%, and NIO -7.63% as price war fears weigh on the space. There is no report tomorrow with China and Hong Kong is closed.

The Hang Seng and Hang Seng Tech fell -0.82% and -2.94% respectively on volume -0.84% from yesterday which is 99% of the 1-year average. 196 stocks advanced while 298 stocks declined. Main Board short turnover declined -9.96% from yesterday which is 82% of the 1-year average. Value factors outperformed growth factors as large caps outperformed small caps. Top sectors were energy gaining +1.68%, industrials closing higher +0.34%, and materials finishing up +0.21% while discretionary fell -3%, tech closed lower -1.64%, and real estate finished down -1.56%. Top sub-sectors were telecom, energy, and household products while auto, retailing, and media were the worst. Southbound Stock Connect volumes were moderate as Mainland investors bought $464 million of Hong Kong stocks with SenseTime a large net buy, Tencent a small net sell, and Meituan a large net sell.

Shanghai, Shenzhen, and STAR Board closed +0.49%, -0.45%, and +0.23% respectively on volume +5.15% from yesterday which is 146% of the 1-year average. 1,188 stocks advanced while 3,518 stocks declined. Value factors outperformed growth factors while large caps outperformed small caps. Top sectors were healthcare gaining +1.06%, staples closing higher +1.02%, and communication finishing up +0.98% while discretionary fell -1.22%, materials closed lower -0.68%, and real estate finished down -0.41%. Top sub-sectors were telecom, construction, and precious metals while education, power generation equipment, and electric power grid. Northbound Stock Connect volumes were high as foreign investors sold -$530 million of Mainland stocks with nine of the top ten Connect volume stocks were sells. CNY sold off slightly versus the US dollar. Treasury bonds gained while Shanghai copper and steel were down.

Major Chinese City Mobility Tracker

Last Night's Performance

Last Night’s Exchange Rates, Prices, & Yields

- CNY per USD 6.88 versus 6.88 yesterday

- CNY per EUR 7.50 versus 7.49 yesterday

- Asia Dollar Index +0.03% overnight

- Yield on 10-Year Government Bond 2.85% versus 2.86% yesterday

- Yield on 10-Year China Development Bank Bond 3.03% versus 3.03% yesterday

- Copper Price -0.29% overnight

- Steel Price -2.11% overnight