No Inflation, Real Estate Rebound, & Electric Vehicle Sales Up +34% YoY

3 Min. Read Time

Key News

Asian equities were higher overnight.

The most significant catalyst overnight was China’s inflation numbers which are the envy of central bankers globally as CPI was 0.7% versus expectations of 1% and February’s 1%, and PPI was -2.5% versus expectations of -2.5% and February's -1.4%. The data provides policy makers stimulus runway. March aggregate financing, money supply (M2), and new loans all beat expectations (RMB 5.38 trillion versus expectations RMB 4.5 trillion; M2 was up +12.7% versus expectations 12.7%; New Loans RMB 3.89 trillion versus expectations RMB 3.3 trillion). Within the loan data, housing loan demand increased, which we knew from sales data released a week ago following a bottoming in February.

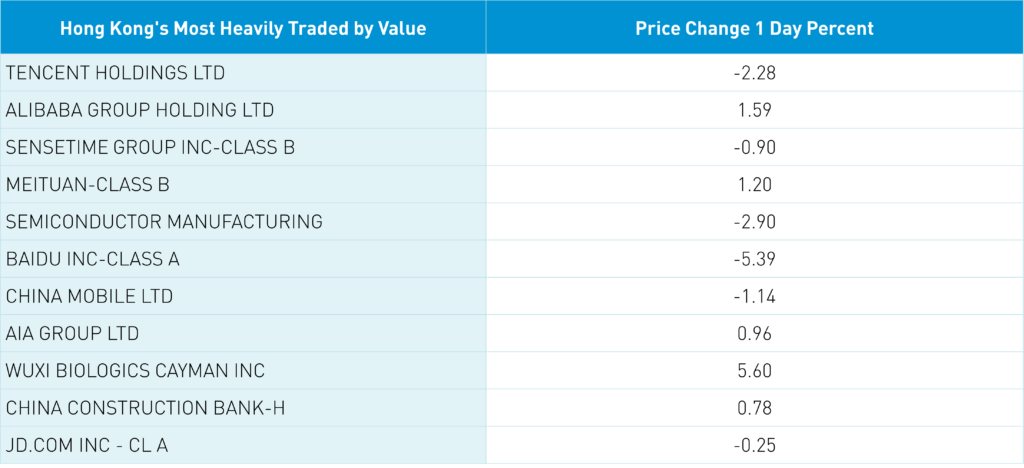

Hong Kong real estate was the top sector, gaining +7% as China’s “Lehman moment” appears to have been avoided. I’ll be curious to look up how the real estate companies’ US dollar high yield bonds did today. Foreign Direct Investment was a touch light at 5.1% versus expectations of 6%. Alibaba gained +1.59% after Alibaba Cloud Intelligence announced the launch of its AI driven large language model named Tongyi Qianwen, which means “truth from a thousand questions”, which will be integrated into applications across Alibaba’s ecosystem. JD.com HK fell -0.25% after it announced it too will be launching a ChatGPT like offering. The National Internet Information Office asked for comments on its draft of AI regulations which should be a surprise to nobody.

There has been jawboning talking down retail investors’ enthusiasm for anything AI-driven, which weighed on Baidu, which fell -5.39% overnight.

The China Association of Automobile Manufacturers announced sales of new energy vehicles increased 34.8% year over year to 653,000 while total auto sales were up 9.7% YoY to 2.45 million. EV’s penetration rate is now 26.6%! Hong Kong had a strong day on high volumes with communication being the only down sector due to Tencent falling -2.28%. Short turnover was only 13% of total turnover indicating shorts are not “challenging” the market’s strength (or at least today). Mainland China was mixed overnight with Shanghai down -0.05% and Shenzhen up +0.14%. There has been a significant change in the Mainland’s most heavily traded stocks as semis/self-sufficient tech/a bit of AI are garnering investor attention.

The Hang Seng and Hang Seng Tech gained +0.76% and +0.25%, respectively, on volume +24.79% from last Thursday which is 105% of the 1-year average. 403 stocks advanced while 101 declined. Main Board short turnover increased +25.88% from last Thursday which is 82% of the 1-year average as 13% of turnover was short turnover. Growth factors outpaced value factors as small caps outpaced large caps. Top sectors were real estate up +7%, healthcare closing higher +4.09%, and materials gaining +3.82%, while communication was the only negative sector closing lower -2.24%. Top sub-sectors were pharma, food, and materials while software, semis, and telecom underperformed. Southbound Stock Connect volumes were high as Mainland investors bought $508 million of Hong Kong stocks with Tencent a large net sell, Sense Time was a moderate net buy, and Meituan was a small net buy.

Shanghai, Shenzhen, and STAR Board diverged to close -0.05%, +0.14%, and -0.66%, respectively, on volume -11.06% from yesterday which is 119% of the 1-year average. 1,843 stocks advanced while 2,793 stocks declined. Value factors outpaced growth factors while small caps outpaced large caps. Top sectors were communication up +1.9%, real estate closing higher +1.24%, and materials gaining +0.92%, while staples fell -1.58%, industrials closed lower -0.52%, and healthcare finished down -0.44%. Top sub-sectors were cultural media, precious metals, and computer hardware while telecom, liquor, and aviation were the worst. Northbound Stock Connect volumes were elevated as foreign investors bought $381 million of Mainland stocks. CNY closed -0.01% versus the US dollar at 6.88 while Treasury bonds rallied. Shanghai copper and steel were both off.

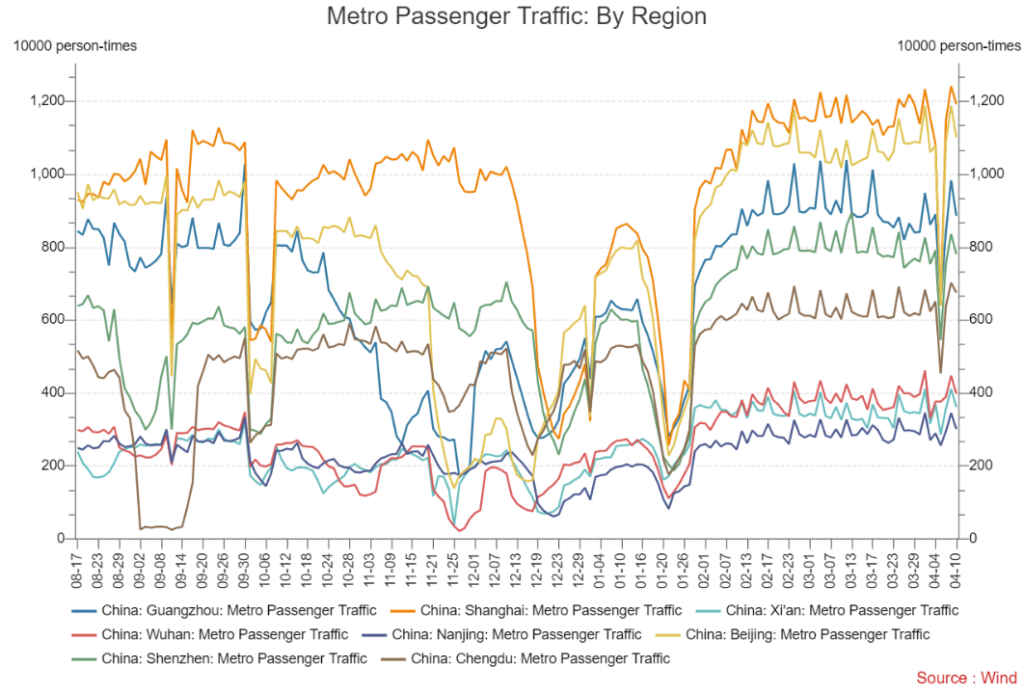

Major Chinese City Mobility Tracker

Last Night's Performance

Last Night’s Exchange Rates, Prices, & Yields

- CNY per USD 6.88 versus 6.87 yesterday

- CNY per EUR 7.51 versus 7.49 yesterday

- Asia Dollar Index -0.01% overnight

- Yield on 10-Year Government Bond 2.82% versus 2.85% yesterday

- Yield on 10-Year China Development Bank Bond 3.00% versus 3.02% yesterday

- Copper Price -0.32% overnight

- Steel Price -1.09% overnight