JD.com’s 618 Sales Event Kicks Off, Caixin Manufacturing PMI Beats Expectations

2 Min. Read Time

Key News

Asian equities were mixed on the great news of a debt ceiling deal and some belief that the Fed may pause in June, though fixed income futures appear to disagree.

Caixin released the May Manufacturing PMI overnight, which came in at 50.9 versus expectations of 49.5 and April’s 49.5. The Caixin PMI survey is called the “private” as the survey, as it is conducted by private company IHS Markit (now owned by S&P) and focuses on small and medium enterprises (SMEs) versus the “official” PMI’s focus on large companies. However, the Caixin survey polls fewer people than the official PMI, leading to higher volatility.

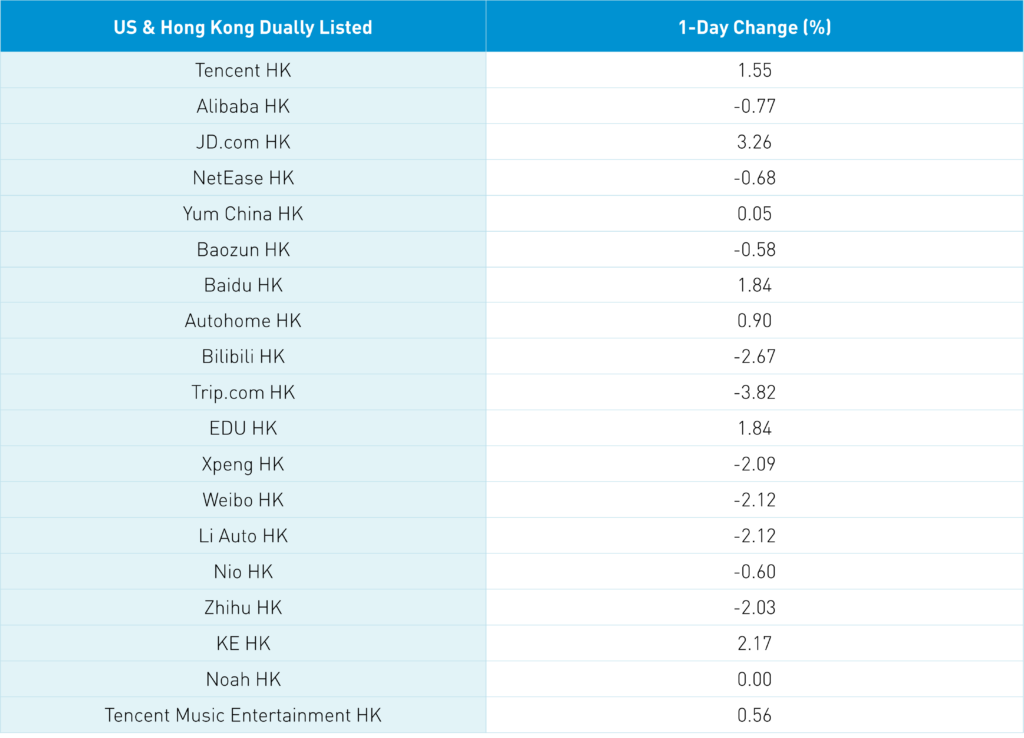

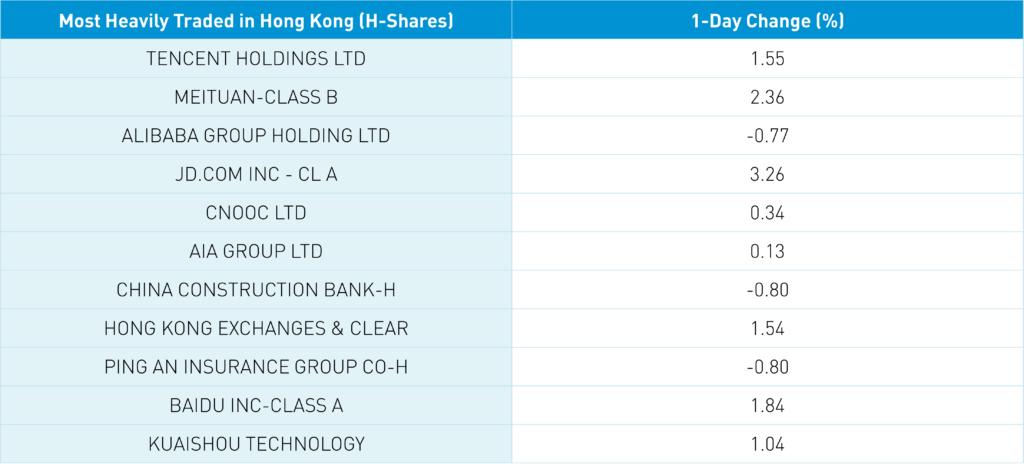

JD.com’s mid-year shopping festival, the "618 sales event", kicked off with an impressive start. JD.com stated that “23% more brands achieved the RMB 100-million-yuan sales milestone within the first ten minutes compared to last year.” JD.com’s strong start was evidenced by Hong Kong’s most heavily traded stocks today, which were concentrated in E-Commerce names. They included Tencent, which gained+1.55%, Meituan, which gained +2.36%, Alibaba, which fell -0.77% as short turnover fell to 11% today from yesterday’s 32%, and JD.com, which gained +3.26%. While Hong Kong-listed internet stocks outperformed, the broad market came off the intra-day highs to post small gains.

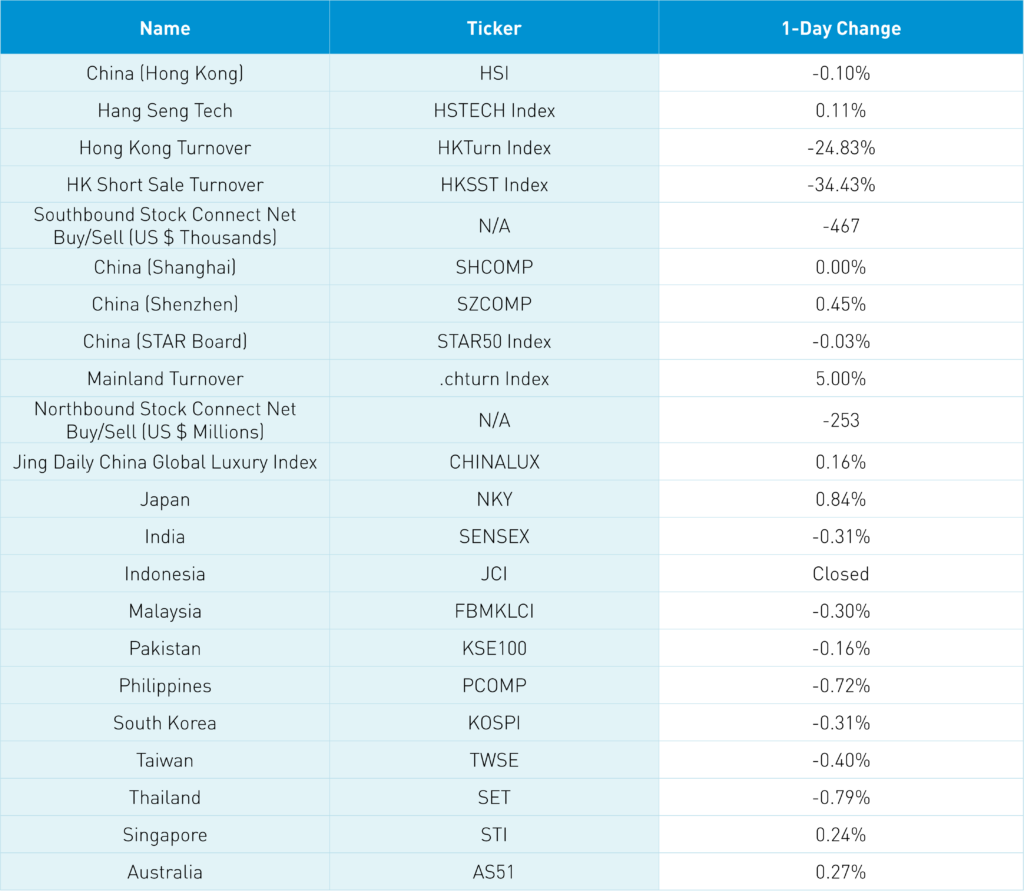

The Mainland market posted a flat day as support levels for Shanghai at 3,200 and Shenzhen’s 2,000 held steady.

Real estate was weak overnight in Hong Kong and Mainland China on expected light sales volumes for May.

After the close, May electric vehicle (EV) sales were released. BYD announced sales of over 240,220 new energy vehicles (NEVs) in May, bringing the year-to-date total to 1 million units sold, according to CnEVPost.com.

There is a rumor that Nvidia’s CEO Jensen Huang will visit China following trips this week from Elon Musk and Jamie Dimon.

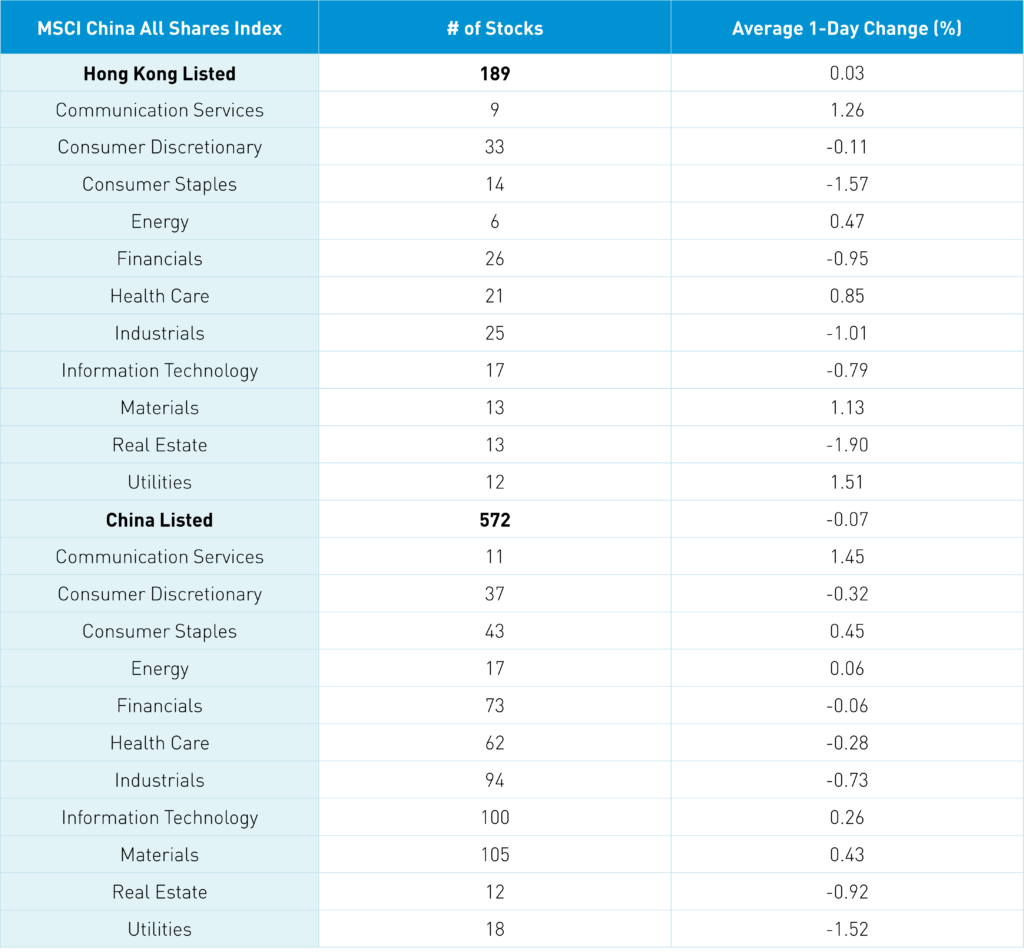

The Hang Seng and Hang Seng Tech indexes diverged to close -0.1% and +0.11%, respectively, on turnover that decreased -24.83% from yesterday, which is 109% of the 1-year average. 222 stocks advanced, while 277 stocks declined. Main Board short turnover declined -34.45% from yesterday, which is 114% of the 1-year average, as 18% of turnover was short turnover. Growth factors outperformed value factors as large caps outpaced small caps. The top-performing sectors were utilities, which gained +1.51%, communication services, which gained +1.26%, and materials, which gained +1.13%, while real estate fell -1.91%, consumer staples fell -1.57%, and industrials fell -1.01%. The top-performing subsectors were media, software, and materials. Meanwhile, food, transportation, beverages, and tobacco were among the worst. Southbound Stock Connect volumes were light as Mainland investors sold a net -$467 million worth of Hong Kong stocks as Tencent and Meituan were moderate net buys.

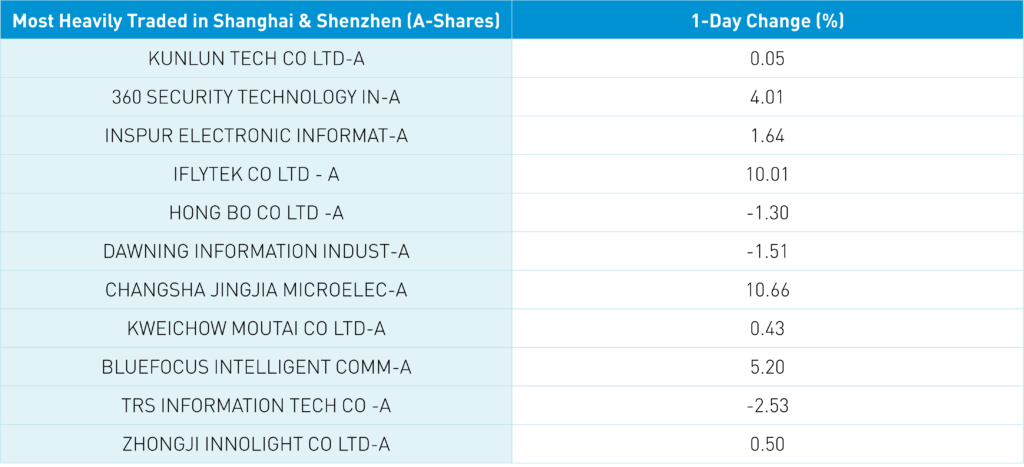

Shanghai, Shenzhen, and the STAR Board diverged to close 0.0%, +0.45%, and -0.03%, respectively, on volume that increased +5% from yesterday, which is 106% of the 1-year average. 2,790 stocks advanced, while 1,875 declined. Growth factors outperformed value factors, while large caps edged out small caps. The top-performing sectors were communication services, which gained +1.43%, consumer staples, which gained +0.43%, and materials, which gained +0.43%. Meanwhile, utilities fell -1.54%, real estate fell -0.93%, and industrials fell -0.75%, making up the worst-performing sectors. The top-performing subsectors were cultural media, software, and internet. Meanwhile, land transportation, airports, and aviation. Northbound Stock Connect volumes were moderate/light as foreign investors sold a net -$253 million worth of Mainland stocks though Foxconn was a small net buy. Kweichow Moutai was a moderate/high net sell and China Tourism Group Duty-Free was a moderate net sell. CNY eased -0.04% versus the US dollar while the Asia Dollar Index pulled a James Bond, gaining +0.07%. Treasury bonds rallied, along with copper and steel.

Last Night's Performance

Last Night’s Exchange Rates, Prices, & Yields

- CNY per USD 7.11 versus 7.11 yesterday

- CNY per EUR 7.62 versus 7.59 yesterday

- Asia Dollar Index +0.07% overnight

- Yield on 10-Year China Development Bank Bond 2.68% versus 2.69% yesterday

- Yield on 10-Year China Development Bank Bond 2.84% versus 2.85% yesterday

- Copper Price +0.71% overnight

- Steel Price +1.71% overnight