Trip.com Beats as Chinese Travelers Pack Their Bags, Markets React to Major Policy Makers’ Speeches in Shanghai

4 Min. Read Time

Trip.com Earnings Overview

This is a big review as Trip.com provided a good look into domestic consumption. The company very well-run, in my opinion, and management are straight shooters. The company's results annihilated analyst expectations. Its China-focused domestic travel business saw robust year-over-year growth (YoY), as domestic travel returned to pre-COVID levels, driving an impressive 124% year-over-year (YoY) gain in revenue. Accommodation reservation revenue increased 40% YoY, which represents a growth rate of 106% quarter-over-quarter, which is 15% higher than pre-COVID (2019). Hotel bookings and transportation ticketing revenue increased 40% and 24%, respectively, from pre-pandemic levels. Corporate travel revenue increased 100% YoY and 61% quarter over quarter, which is 87% higher than the 2019 level. The domestic China travel business is clearly back, though the company’s upside has been capped by limited outbound travel and inbound foreign tourists. Outbound hotel and air reservations are at 60% of 2019 levels, with most travelers headed to Hong Kong, Macau, Thailand, and Singapore. As governments communicate with one another, we should see an increase in flights to China and Asia, for that matter. Getting from Europe and the East Coast of the US to China on a non-Chinese airline isn’t easy though Trip.com should benefit as more airline routes come back online. Hat tip to management for keeping costs down as many sell-side analysts questioned the company about their decade-high margins. When asked about the state of China’s consumers, CFO Cindy Xiaofan Wang responded, “..we are confident in the long-term outlook of the travel consumption in China. The demand for travel as part of the service consumption recovery is expected to keep increasing in China…”.

- Revenue +124% YoY to RMB 9.2 billion ($1.3 billion) versus analyst expectations of RMB 8.05 billion.

- Adjusted net income increased to RMB 2.065 billion ($300 million) from a loss of RMB -36 million versus analyst expectations of RMB 1.254 billion.

- Adjusted EPS increased to RMB 3.07 ($0.45) from a loss of RMB -0.06 versus analyst expectations of RMB 1.82.

Key News

Asian equities were largely lower except for Hong Kong, Mainland China, and Thailand, which outperformed.

The Bangles might need to rename their ‘80s hit to "Hazy Shade of Summer" as we are fogged/smoked in here in New York.

The Lujiazui Forum kicked off in Shanghai today with speeches from the heads of the PBOC (central bank), CSRC (China’s SEC), CBIRC (insurance/bank regulator), SAFE (currency regulator), and the National Social Security Fund Council. The opening and keynote speech was from Li Yunze of the CBIRC, who stated, “We grasp the key task of restoring and expanding effective demand… increase support for new consumption and service consumption finance, promote major consumption areas such as new energy vehicles and green home appliances.” I wonder where we should invest? Mainland investors did not need a treasure map as Gree Electric Appliances (00651 CH) gained +2.96%, and peer Midea Group (000333 CH) gained +2.97%. He also noted his “support for the transformation of urban villages in large and megacities.”

What was the best performing sector in Mainland China and Hong Kong overnight? Real estate, which gained +1.77% and +2.62% in both markets, respectively. Chinese real estate bonds denominated in the offshore US dollar look tempting despite investors’ lack of interest, in my opinion.

Autos were off on recent outperformance, despite the Ministry of Commerce releasing a statement on supporting auto consumption.

The economic focus from policymakers and bank deposit interest rate cut has raised expectations that the loan prime rate will be next week when the medium-term lending facility rate is announced. A bank reserve requirement ratio cuts may follow this. Financials gained +1.65% in China and +1.05% in Hong Kong. I would argue that there will be better news coming rather than bad news in the weeks and months ahead (fingers crossed, of course). Remember, this is against the backdrop of low investor allocation, i.e., pain trade higher.

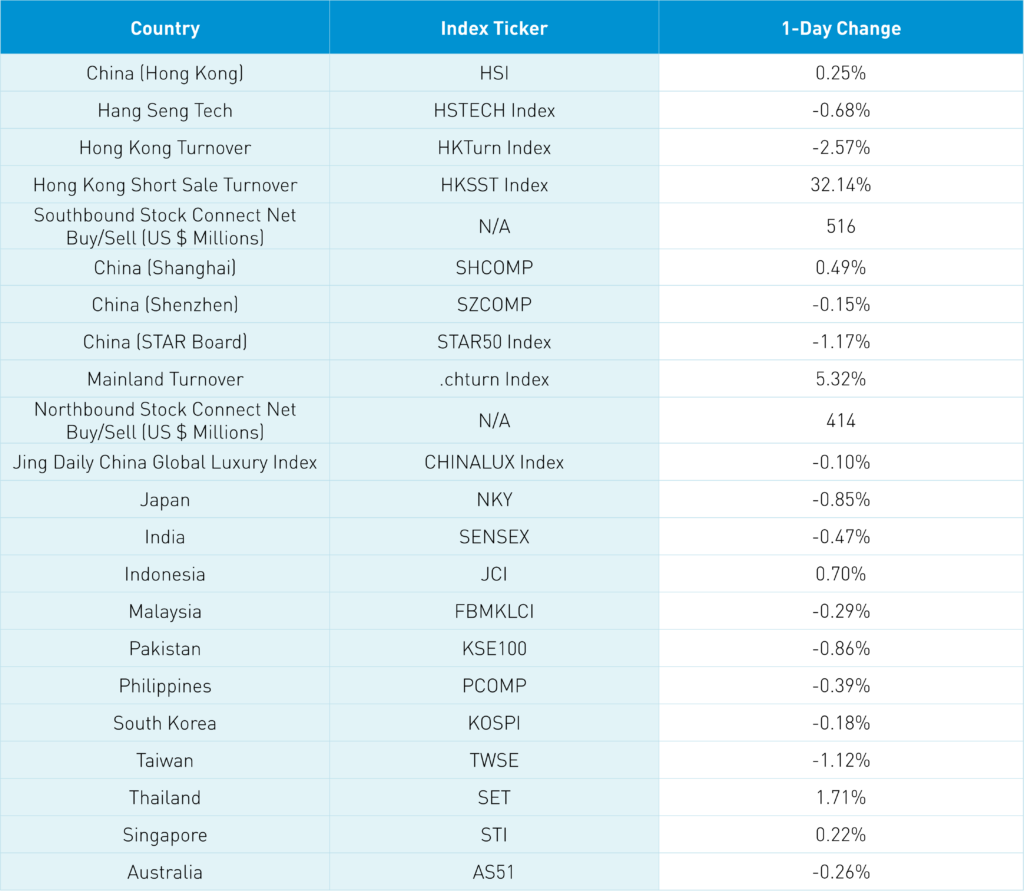

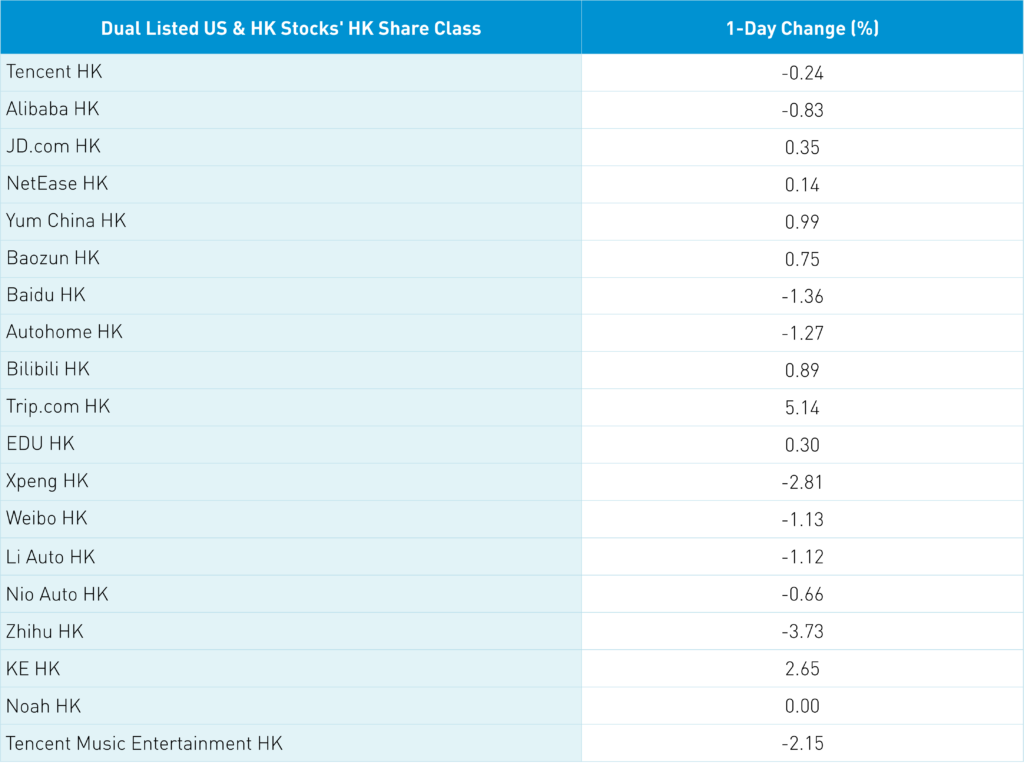

The Hang Seng posted a small gain, closing above the 19k level as Hong Kong’s most heavily traded stocks were Tencent, which fell -0.24%, Alibaba, which fell -0.83%, and Meituan, which gained +0.73% along with Kuiashou, which fell -2.82%, JD.com, which gained +0.35%, NetEase, which gained +0.65%, and Baidu, which fell -1.36%. Hong Kong Main Board short turnover jumped +32% from yesterday, with short activity focused on Hong Kong-listed ETFs versus individual stocks, as 19% of the volume was high short volume. Value stocks and sectors led Shanghai higher as real estate and financials were higher on the policy, along with energy having a good day. Growth-focused Shenzhen and STAR Board were both off. Buying in the Mainland via foreign investors and in Hong Kong from Mainland investors via the Northbound and Southbound Connect programs.

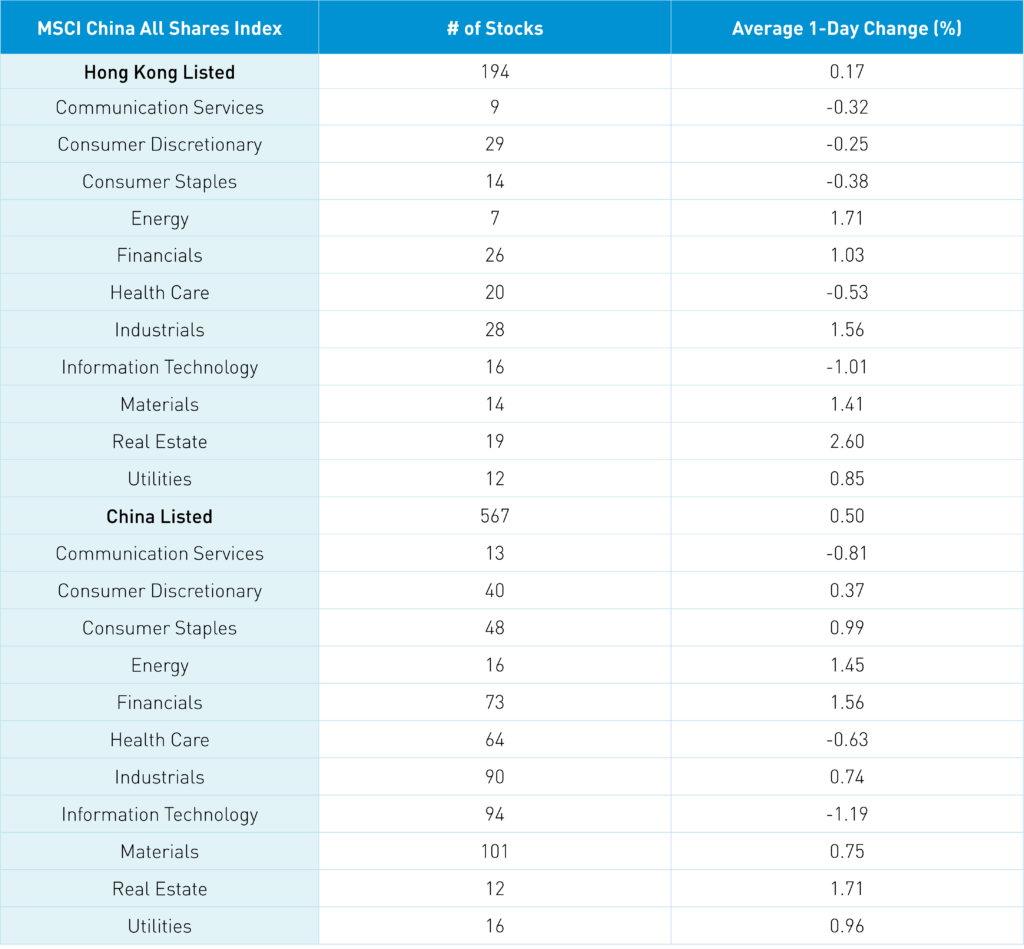

The Hang Seng and Hang Seng Tech diverged to close +0.25% and -0.68%, respectively, on volume that increased +32.14% from yesterday, which is 71% of the 1-year average. 260 stocks advanced, while 228 stocks declined. Main Short turnover increased by +32.21% from yesterday, which is 83% of the 1-year average, as 19% of turnover was short turnover. Value factors outperformed growth factors as small caps outpaced large caps. The top sectors were real estate +2.6%, energy +1.71%, and industrials +1.56%, while the worst were tech -1.01%, healthcare -0.53%, and staples -0.38%. The top sub-sectors were energy, insurance, and food, while semis, auto, and healthcare equipment were the worst. Southbound Stock Connect volumes were light as Mainland investors bought +$516 million of Hong Kong stocks, with Li Auto a small net buy, and Tencent, Meituan, and Kuiashou were small net sells. Citibank’s CEO joined the list of Western executives visiting China.

Shanghai, Shenzhen, and the STAR Board diverged to close +0.49%, -0.15%, and -1.17%, respectively, on volume that increased +5.32%, which is 93% of the 1-year average. 1,814 stocks advanced, while 2,841 stocks declined. Value factors outperformed growth factors as large caps outperformed small caps. The top sectors were real estate +1.7%, financials +1.56%, and energy +1.44%, while tech -1.19%, communication -0.81%, and healthcare -0.63% were the worst. The top sub-sectors were construction machinery, forest, and agriculture, while education, leisure, and cultural media were the worst. Northbound Stock Connect volumes were light as foreign investors bought $414 million of Mainland stocks, with volume leaders Ping An, Kweichow Moutai, and China Tourism Duty-Free all small net sells. CNY and the Asia dollar index fell slightly versus the US dollar as the Treasury curve flattened. Copper and steel made small gains.

Last Night's Performance

Last Night’s Exchange Rates, Prices, & Yields

- CNY per USD 7.12 versus 7.11 yesterday

- CNY per EUR 7.64 versus 7.62 yesterday

- Yield on 10-Year Government Bond 2.68% versus 2.68% yesterday

- Yield on 10-Year China Development Bank Bond 2.83% versus 2.83% yesterday

- Copper Price +0.12% overnight

- Steel Price +0.58% overnight