Month-End Politburo Meeting Happens Sooner Than Expected

3 Min. Read Time

Key News

Asian equities were largely higher as Hong Kong and Mainland China outperformed the region on high volume and very strong breadth after the month-end politburo meeting took place four days earlier than expected.

President Xi presided over the meeting and the issuance of a stronger-than-anticipated communique. Here is the key for investors: the release is just the start, and we may see formalized measures outlined likely starting next week.

Do you think global investors are positioned for this? Neither do I. Western media coverage of this very significant event is scarce. The rally into month-end will lead to discomfort for active portfolio managers who are underweight China as they will need to disclose their holdings. If the rally can sustain itself, this discomfort will magnify going into quarter-end.

What was in the release and what has been the effect on stocks overnight?

- The fact that this meeting took place days before anticipated indicates the government’s acknowledgement of economic challenges.

- The tone of the release acknowledges the economic “difficulties and challenges, mainly due to insufficient domestic demand.” Solving this issue will require “counter-cyclical adjustments and policy reserves, as well as a proactive fiscal policy and a prudent monetary policy” and “improve and implement the tax and fee reduction policy”, support of “small and medium enterprises” (private companies).

- The importance of RMB stability was also mentioned.

- As mentioned yesterday, the absence of the “housing is for living, not for speculation” mantra, along with hints of supportive policies made real estate the top-performing sector in Hong Kong, where it gained +13.4%, and on the Mainland, where it gained +7.51%.

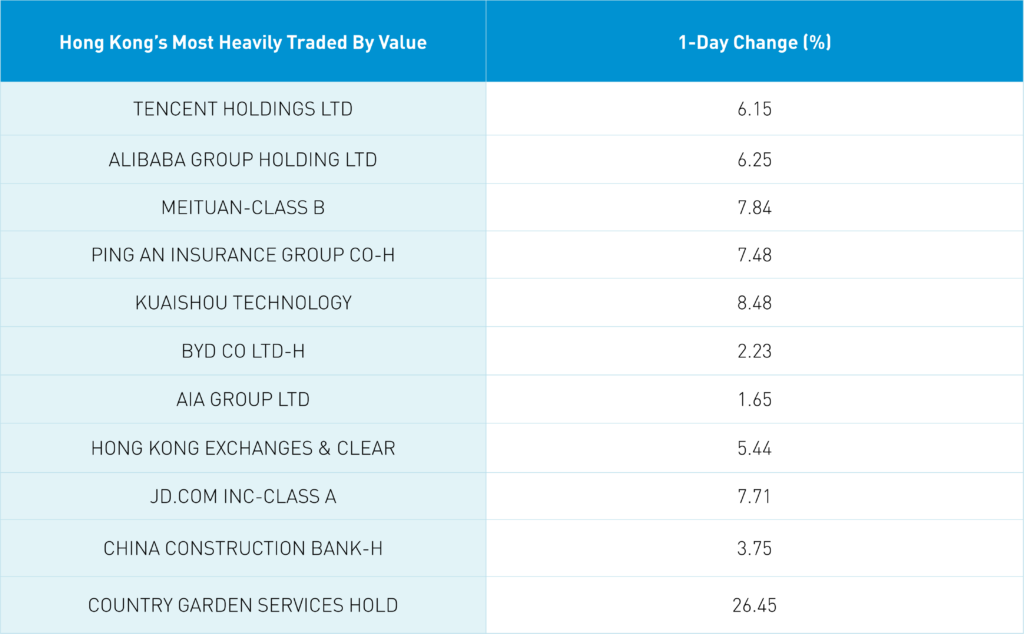

- Overnight, Hong Kong-listed internet stocks outperformed their US-listed counterparts. The statement mentioned internet companies, which are referred to as the “platform economy”, specifically. Hong Kong’s most heavily traded stocks were Tencent, which gained +6.15% versus yesterday’s US gain of +2.28%, Alibaba, which gained +6.25% versus yesterday's US gain of +4.54%, and Meituan, which gained +7.84% versus yesterday's US gain of +3.97%.

- “Activating” the stock market is an interesting term, though is clearly alludes to addressing poor investor sentiment.

- Addressing local government debt will require “a package of debt plans”.

- The Politburo also stated that “It is necessary to boost the mass consumption of automobiles, electronic products, and home furnishing”. From this, Hong Kong-listed electric vehicle (EV) companies gained, led by BYD, which gained +2.23%, Xpeng, which gained +12.75%, Li Auto, which gained +5.27%, and NIO, which gained +2.15%. On the Mainland, home appliance makers Gree and Midea gained +5.68% and +3.89%, respectively.

Nonetheless, investors will want actionable plans implemented quickly as talk is cheap. Was short covering part of today’s rip higher? I would assume so, though the tone of the release, if accompanied by tangible measures, could give the rally legs.

Northbound Stock Connect volumes were high as foreign investors bought a healthy $2.7 billion worth of Mainland stocks. Southbound Stock Connect saw net outflows, though they appear to be driven by a large outflow from Hong Kong-listed ETFs as Tencent, Kuaishou, and Meituan were all large net buys. We also saw technical break outs as the Hang Seng closed above the 19,000 level, Shanghai is now above 3,200, and Shenzhen is above the 2,000 level.

Yesterday, I met with one of the largest Chinese asset managers who is visiting New York. I also attended a meeting with two members of Congress. I will discuss my insights from these meetings in tomorrow's edition!

The Hang Seng and Hang Seng Tech indexes gained +4.1% and +6.04%, respectively, on volume that increased +51.98% from yesterday, which is 126% of the 1-year average. 478 stocks advanced while 35 declined. Main Board short turnover declined -6.99% from yesterday, which is 120% of the 1-year average, as 16% of turnover was short turnover. The growth factor outperformed the value factor as small caps outpaced large caps. All sectors were positive as real estate gained +13.39%, communication services gained +6.23%, and consumer discretionary gained +6.12%. All subsectors were positive as real estate, retail, and software companies were the top performers. Southbound Stock Connect volumes were high as Mainland investors sold a net $783 million worth of Hong Kong stocks and ETFs, including Xpeng, a small net sell, Meituan, a moderate net buy, Tencent, a large net buy, and Kuaishou, a large net buy.

Shanghai, Shenzhen, and the STAR Board gained +2.13%, +2.19%, and +1.46%, respectively, on volume that increased +44.35% from yesterday, which is 106% of the 1-year average. 4,066 stocks advanced while 702 declined. Value factors outperformed growth factors while large caps outpaced small caps. The top-performing sectors were real estate, which gained +7.49%, financials, which gained +5.11%, and consumer discretionary, which gained +4.57%. Meanwhile, utilities constituted the only negative sector, falling -0.52%. The top-performing subsectors were insurance, real estate, and household products. Meanwhile, agriculture and the power industry were the only negative subsectors. Northbound Stock Connect volumes were high as foreign investors bought a healthy $2.66 billion worth of Mainland stocks including Kweichow Moutai, a very large net buy, Ping An Insurance, a large net buy, and China Tourism Duty Free, a moderate net buy. CNY gained +0.58% versus the US dollar to close at 7.14 CNY per USD while the Asia Dollar Index gained +0.37%. Treasury bonds sold off while copper and steel gained.

Last Night's Performance

Last Night’s Exchange Rates, Prices, & Yields

- CNY per USD 7.14 versus 7.19 yesterday

- CNY per EUR 7.87 versus 7.96 yesterday

- Yield on 1-Day Government Bond 1.30% versus 1.30% yesterday

- Yield on 10-Year Government Bond 2.66% versus 2.60% yesterday

- Yield on 10-Year China Development Bank Bond 2.78% versus 2.74%

- Copper Price +0.60% overnight

- Steel Price +0.71% overnight