Beijing & Shanghai Lower Down Payments for First-Time Home Buyers

3 Min. Read Time

Key News

Asian equities cheered the Fed’s interest rate cut outlook, except for Japan and China, while the Philippines outperformed.

The US dollar fell as China’s currency the Renminbi (CNY) gained +0.54%, closing at 7.13 CNY per USD from yesterday’s 7.17, the Bloomberg Asia Dollar Index gained +0.8%, and the Bloomberg Dollar Index fell -0.36%. CNY has appreciated versus the dollar from 7.32 on November 2nd to today’s 7.13 CNY per USD. Usually, this would be a good tailwind for Chinese stocks, though it has yet to materialize.

Mainland investors were hoping for more domestic consumption support from the Central Economic Work Conference (CEWC) yesterday, which has weighed on sentiment. Remember yesterday’s loan and financing data release, which occurred after the market’s close and missed expectations? No one seemed to mention/notice the data improved month over month as the beatings will continue until morale improves.

The Shanghai, Shenzhen, and the Hang Seng Index all opened higher by +0.37%, +0.41%, and +1.18%, respectively, but slid throughout the day. It was a relatively quiet night except for President Xi finishing his trip to Vietnam amid rumors he will attend Davos in January. There has been an apparent change in the tone and tenor of China's rhetoric toward the West, particularly the US. Trust must be rebuilt, but something has changed for those willing to notice.

After the market close, both Beijing and Shanghai reduced their down payment ratios for first-time home buyers to 30%, the second home purchase down payment ratio was lowered to 50%, and the mortgage rate was lowered. As we noted yesterday, real estate continues to be a concern, though policymakers are very aware. Overnight distress property developer Country Garden raised $428 million by selling its stake in mall operator Dalian Wanda. The move follows yesterday’s unexpected bond repayment.

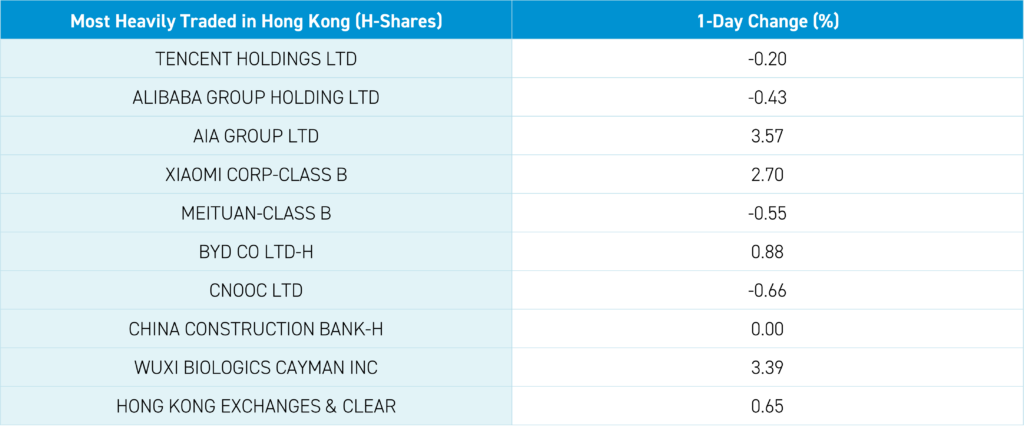

Hong Kong’s most heavily traded stocks by value were Tencent, which fell -0.20%, Alibaba, which fell -0.43%, AIA, which gained +3.57%, Xiaomi, which gained +2.7%, and Meituan, which fell -0.55% even though it is likely to benefit from the cold weather in northern China as blizzards hammer the region. The Hong Kong Tracker ETF saw its largest net outflow via Southbound Stock Connect since September 11th as Mainland investors sold a net HKD 6.7 billion worth of Hong Kong stocks ($850 million). The inflow/outflow from Southbound is bizarre to me. Foreign investors turned to net buyers of Mainland stocks today via Northbound Stock Connect.

The Hang Seng and Hang Seng Tech indexes gained +1.07% and +0.34%, respectively, on volume that increased +35% from yesterday, which is 97% of the 1-year average. 346 stocks advanced, while 119 declined. Main Board short turnover increased +4% from yesterday, which is 75% of the 1-year average, as 13% of turnover was short turnover (remember Hong Kong short turnover includes ETF short volume, which is driven by market makers’ ETF hedging). The growth factor and small caps outpaced the value factor and large caps. The top-performing sectors overnight were Technology, which gained +3.15%, Health Care, which gained +2.52%, and Utilities, which gained +2.11%. Meanwhile, Communication Services was the only negative sector, falling -0.63%. The top-performing subsectors were technical hardware, utilities, consumer durables, and apparel. Meanwhile, food, software, and transportation were among the worst-performing. Southbound Stock Connect volumes were moderate as Mainland investors sold a net -$1.24 billion worth of ETFs and stocks, as the Hong Kong Tracker ETF had a very large net outflow.

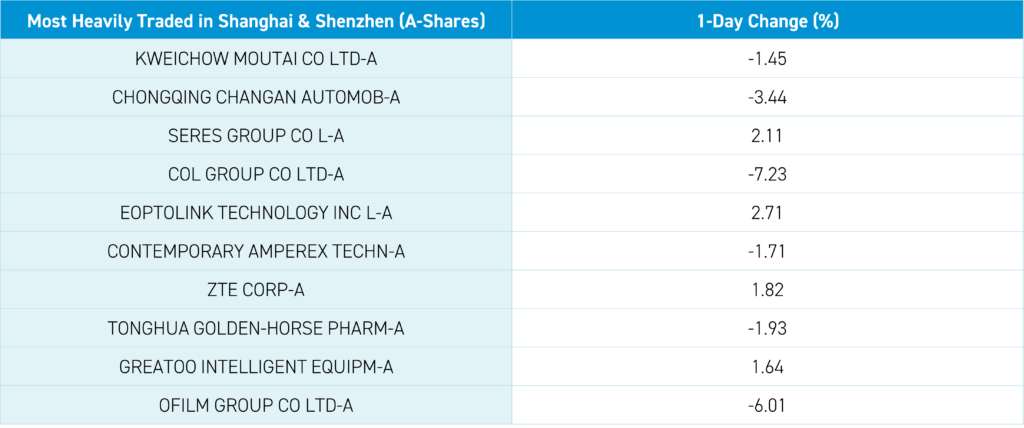

Shanghai, Shenzhen, and the STAR Board fell -0.33%, -0.55%, and -0.62%, respectively, on volume that declined -4% from yesterday, which is 85% of the 1-year average. 1,902 stocks advanced, while 2,866 declined. The value and growth factors performed in line while small caps outperformed large caps. The top-performing sectors overnight were Utilities, which gained +0.72%, Materials, which gained +0.59%, and Energy, which gained +0.59%. Meanwhile, the worst-performing sectors were Consumer Staples, which fell -0.68%, Communication Services, which fell -0.16%, and Real Estate, which fell -0.06%. The top-performing subsectors were gas, leisure products, and water. Meanwhile, education, liquor, and healthcare were among the worst-performing. Northbound Stock Connect volumes were light/moderate as foreign investors bought a net $485 million worth of Mainland stocks including Wanhua, O-Film, the world's largest battery maker Contemporary Amperex Technology (CATL), and Changan Auto. Meanwhile, foreign investors sold Kweichow Moutai and Ping An Insurance. CNY and the Asia Dollar Index rallied versus the US dollar. Treasury bonds sold off slightly, copper gained, and steel fell.

Last Night's Performance

Last Night’s Exchange Rates, Prices, & Yields

- CNY per USD 7.13 versus 7.17 yesterday

- CNY per EUR 7.79 versus 7.74 yesterday

- Yield on 10-Year Government Bond 2.63% versus 2.62% yesterday

- Yield on 10-Year China Development Bond 2.76% versus 2.75% yesterday

- Copper Price +0.21% overnight

- Steel Price -1.08% overnight