“You’re Going the Wrong Way!” as the US Raises Tariffs and China Cuts Tariffs

3 Min. Read Time

Key News

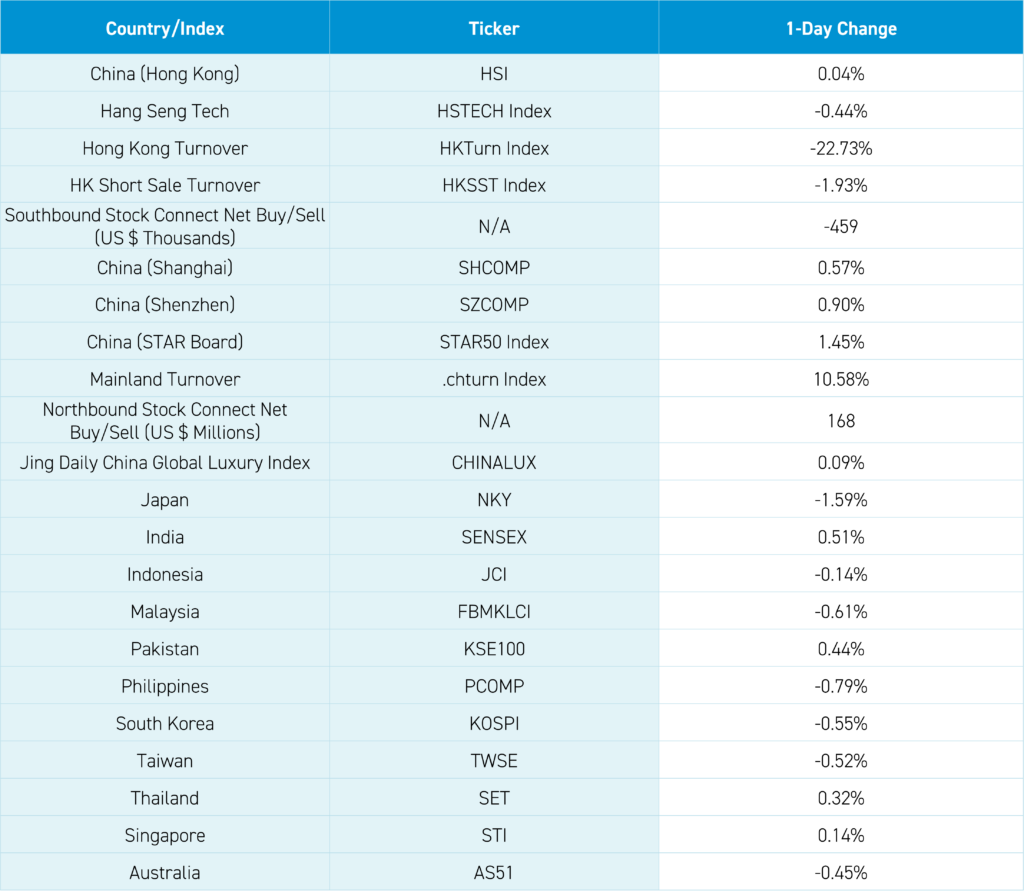

Asian equities were mixed, as Mainland China, Hong Kong, and India outperformed while Japan, Taiwan, and South Korea underperformed. However, Hong Kong and China opened lower following a rare fall in US stocks. Chinese ADRs ground higher to close positive.

The Shanghai Composite dipped below the 2,900 level in morning trading as I might have to redraw my line in the sand from 3,100 to 2,900. There continues to be chatter of more policy support, though investors will want tangible action to rebuild confidence. According to Bloomberg, state-owned banks announced deposit ratios will be cut on Friday, with ICBC’s 1-year deposit decreasing to 1.45% from 1.55%. The move makes parking cash in the bank less appealing versus investing in stocks or spending it. Bonds rallied on the news, with the Chinese 10-year Treasury yield falling to 2.59%. Bloomberg noted that the spread between the 10-year Treasury Yield and dividend yield on Mainland stocks is the lowest ever. I’ll post on X (@ahern_brendan) about the ratio of Mainland stock dividend yield divided by the 10-year government bond yield, which is also at a record level.

The Wall Street Journal is reporting that the Biden Administration is looking to raise tariffs on China-made electric vehicles (EVs) from today’s 25% level. In Shenzhen, EVs and hybrids are everywhere, unlike in the US. I rode in a gorgeous BYD minivan that I cannot buy in the US. Ironically, the State Council Tax Commission will lower tariffs on 1,010 commodities starting January 1. It reminds me of the great line from the holiday classic Planes, Trains and Automobiles: “You are going the wrong way!” and “How do they know where we are going?”.

The news weighed on Hong Kong-listed EV stocks including Li Auto, which fell -4.87%, XPeng, which fell -3.53%, and NIO, which fell -8.63%. Hong Kong’s most heavily traded stocks by value were Tencent, which fell -.51%, Meituan, which gained +1.1%, and Alibaba, which gained +1.1%. It is also fascinating that the Mainland’s most heavily traded stocks by value included EV battery giant CATL, which gained +4% with nice foreign buying via Northbound Stock Connect, LONGi Green Energy, which gained +4.93%, also a net buy from foreign investors, and Kweichow Moutai, which gained +1.23%.

The US military confirmed that they spoke with their Chinese equivalents today. Bloomberg announced that China’s Juneyao Airlines will buy the first Boeing 787 Dreamliner since 2021. It is likely that we will see the 737 Max approved soon.

Beijing and Shanghai’s recent lifting of home purchase restrictions are having an immediate effect, with sales rising dramatically, while more than thirty cities noted that home prices increased last week. Remember, this is key to raising consumer confidence, though one week is the first baby steps that hopefully continue. Do you think investors are positioned for further good news? Me neither!

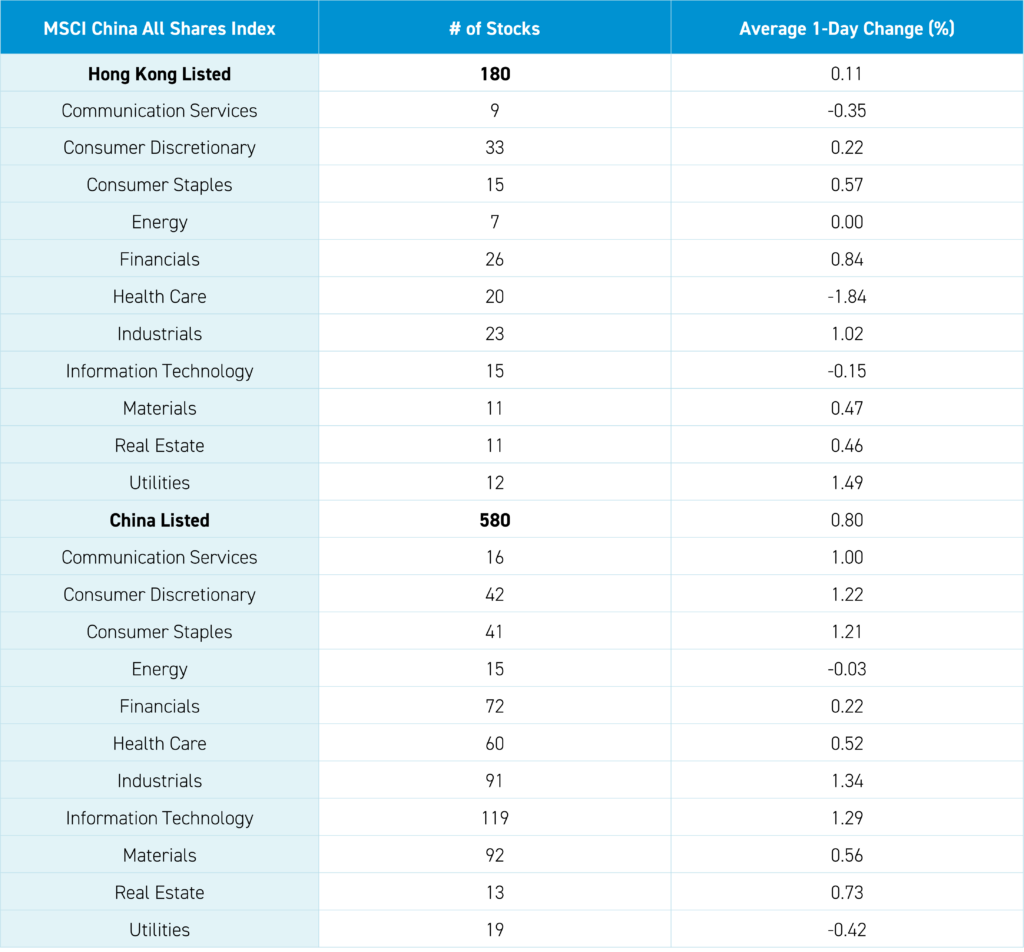

The Hang Seng and Hang Seng Tech diverged to close +0.04% and -0.44%, respectively, on volume that decreased -23% from yesterday, which is 66% of the 1-year average. 331 stocks advanced, while 149 declined. Main Board short turnover declined -2% from yesterday, which is 58% of the 1-year average as 15% of turnover was short turnover (remember Hong Kong short turnover includes ETF short volume, which is driven by market makers’ ETF hedging). The value factor and small caps outperformed the growth factor and large caps. The top-performing sectors were Utilities, which gained +1.5%, Industrials, which gained +1.02%, and Financials, which gained +0.85%. Meanwhile, Health Care fell -1.84%, Communication Services fell -0.34%, and Information Technology fell -0.15%. The top-performing subsectors were transportation, utilities, and banks. Meanwhile, pharmaceuticals, autos, and food retailers were among the worst-performing. Southbound Stock Connect volumes were light as Mainland investors sold a net -$459 million worth of Hong Kong-listed stocks and ETFs, including CNOOC and Tencent. Meanwhile, Meituan, the Hong Kong Tracker ETF, and the Hang Seng Tech ETF were moderate net buys.

Shanghai, Shenzhen, and the STAR Board gained +0.57%, +0.90%, and +1.45%, respectively, on volume that increased +11% from yesterday, which is 84% of the 1-year average. 3,393 stocks advanced, while 1,301 declined. The growth factor and small caps outperformed the value factor and large caps. The top-performing sectors were Industrials, which gained +1.37%, Technology, which gained +1.31%, and Consumer Discretionary, which gained +1.25%. Meanwhile, Utilities fell -0.39% and Energy fell -0.01%. The top-performing subsectors were power generation equipment, tourism, and leisure products. Meanwhile, telecom, marine, and education were the worst. Northbound Stock Connect volumes were moderate as foreign investors bought a net $168 million worth of Mainland stocks, including CATL, a large buy. Meanwhile, BYD and LONGi were moderate net buys. CNY and the Asia Dollar Index fell slightly versus the US dollar. Treasury bonds rallied while copper was off and steel gained.

Last Night's Performance

Last Night’s Exchange Rates, Prices, & Yields

- CNY per USD 7.14 versus 7.13 yesterday

- CNY per EUR 7.84 versus 7.80 yesterday

- Yield on 10-Year Government Bond 2.59% versus 2.62% yesterday

- Yield on 10-Year China Development Bank Bond 2.74% versus 2.77% yesterday

- Copper Price -0.06% overnight

- Steel Price +0.41% overnight