China Markets Rally

2 Min. Read Time

Key News

Asian equities had a strong day, as Mainland China and Hong Kong outperformed while Japan underperformed as the US dollar weakened overnight.

The Renminbi (CNY) and the Asia Dollar Index gained +0.49% and +0.42%, respectively, as the former closed at a level of 7.1, not seen since early June 2023.

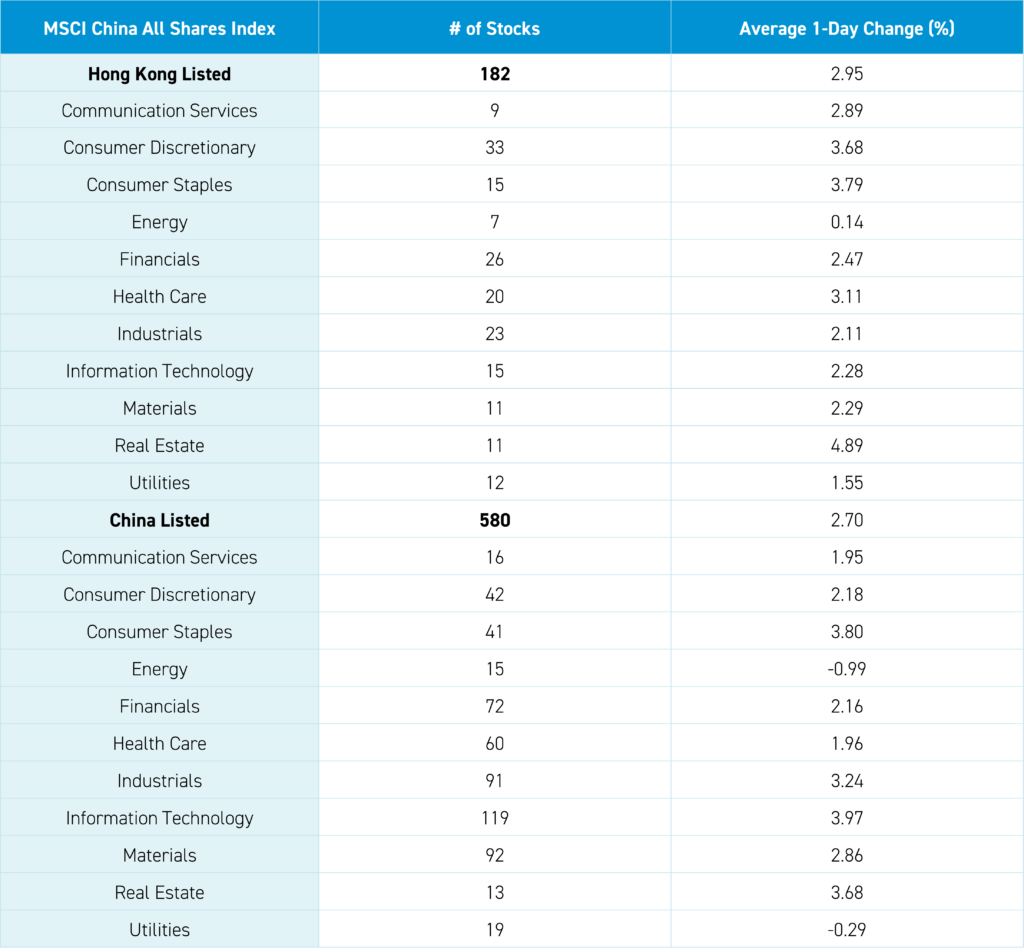

Hong Kong and Mainland China had strong performance days marked by strong breadth (advancers vs. decliners) and volumes as the clean technology sector (electric vehicles, battery, solar, and wind) outperformed.

Yesterday, I read a sell-side research piece on how inexpensive Chinese internet stocks are with two companies’ market caps less than their cash position.

Overnight, there was increased chatter that an interest rate cut might be coming, the Social Security Fund could be increasing its equity allocation, and the CSRC might be clamping down on strategic investors selling their stakes. This all contributed to the rebound.

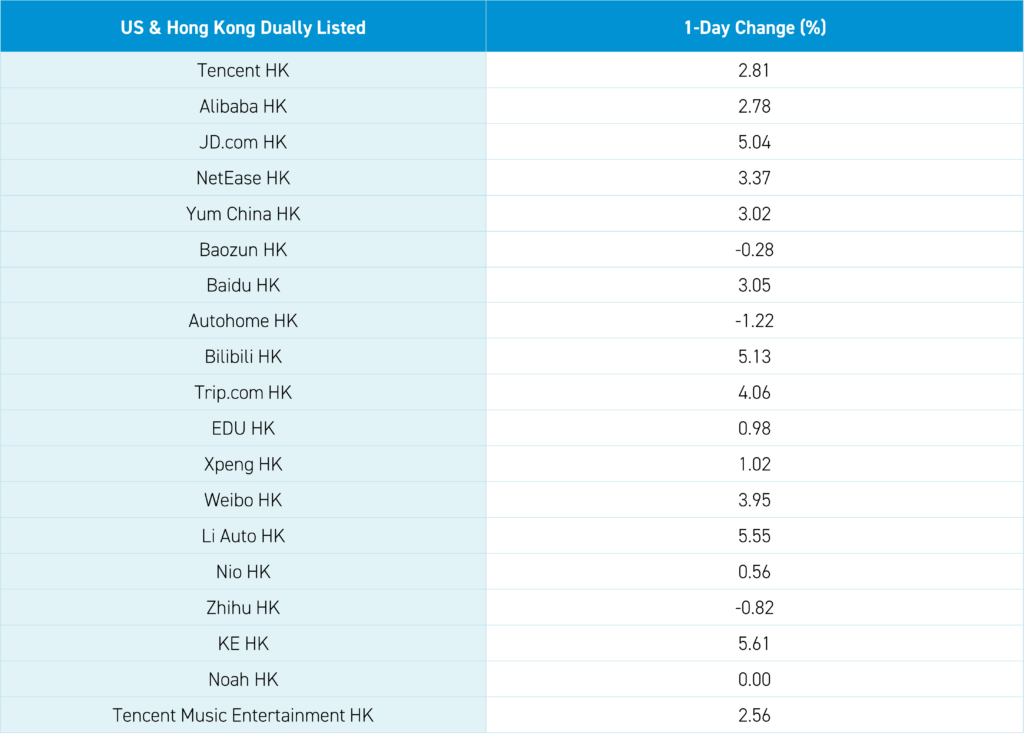

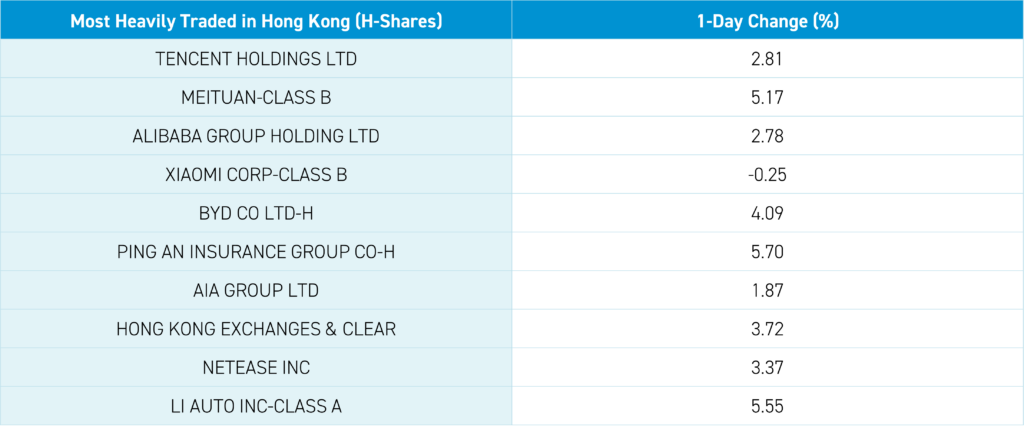

Foreign investors bought a net nearly $2 billion worth of Mainland stocks via Northbound Stock Connect overnight. Hong Kong’s most heavily traded were Tencent +2.81% on 2X normal volumes, Meituan +5.17%, Alibaba HK +2.78%, Xiaomi -0.25%, and BYD +4.09%. Only 4 of the top 100 most heavily traded stocks were down, as all Hong Kong sectors and sub-sectors were positive today. The market has recouped last Friday’s downdraft. The only negative in Hong Kong was that Mainland investors sold $251mm of Hong Kong stocks today. Mainland China also ground higher all day, with large/mega cap growth stocks favored by domestic and foreign investors outperforming, though the breadth wasn’t quite as strong as Hong Kong. Hopefully, today’s positive momentum will continue throughout 2024.

I’m spending time with the family in a shockingly warm New England as Mother Nature is raining on our parade. Our proximity to New Hampshire has led to a healthy dose of primary political TV commercials. I am shocked at a GOP candidate’s commercials, which are almost entirely anti-China-focused. The more US politicians talk about China, the less they are talking about the issues people care about, IMO: crime, inflation, immigration, and the US government’s exploding debt.

The Hang Seng and Hang Seng Tech indexes gained +2.52% and +3.41%, respectively, on volume that increased +11% from yesterday, which is 104% of the 1-year average. 477 stocks advanced, while 31 declined. Main Board short turnover increased +16.88% from yesterday, 92% of the 1-year average, as 15% of turnover was short turnover (remember Hong Kong short turnover includes ETF short volume, which is driven by market makers’ ETF hedging). The growth factor and small caps outperformed the value factor and large caps. All sectors were positive, with real estate +4.92%, staples +3.82% and discretionary +3.71%. All sub-sectors were positive, with retailing, semis, and insurance outperforming. Southbound Stock Connect volumes were high as Mainland investors sold -$251mm of Hong Kong stocks and ETFs with Tencent, CNOOC, and Meituan small/moderate net buys, while the Hong Kong Tracker and HS Tech ETFs were moderate net sells.

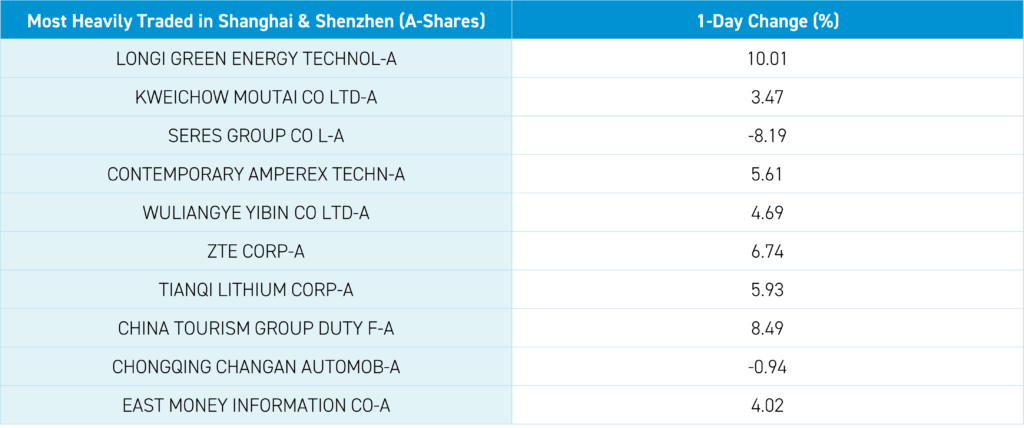

Shanghai, Shenzhen, and the STAR Board gained +1.38%, +2.30%, and +2.45%, respectively, on volume that increased +39.41% from yesterday, which is 101% of the 1-year average. 4,229 stocks advanced, while 721 stocks declined. The growth factor and small caps outperformed the value factor and large caps. Top sectors were tech +3.97%, staples +3.79%, and real estate +3.67% while energy -1% and utilities -0.29%. The top sectors were power generation equipment, catering, and electric power grid, while coal, marine, and highway were the worst. Northbound Stock Connect volumes were high/moderate as foreign investors bought $1.907B of Mainland stocks, with Longi Green Energy, Wuliangye, and Kweichow Moutai seeing large net buys while Changan Auto was a large net sell.

Last Night's Performance

Last Night’s Exchange Rates, Prices, & Yields

- CNY per USD 7.10 versus 7.14 yesterday

- CNY per EUR 7.88 versus 7.91 yesterday

- Yield on 10-Year Government Bond 2.56% versus 2.55% yesterday

- Yield on 10-Year China Development Bank Bond 2.70% versus 2.70% yesterday

- Copper Price -0.62%

- Steel Price +0.05%