US-China Greenshoots, Does Peak Pessimism + Poor Positioning = Rally?

4 Min. Read Time

Key News

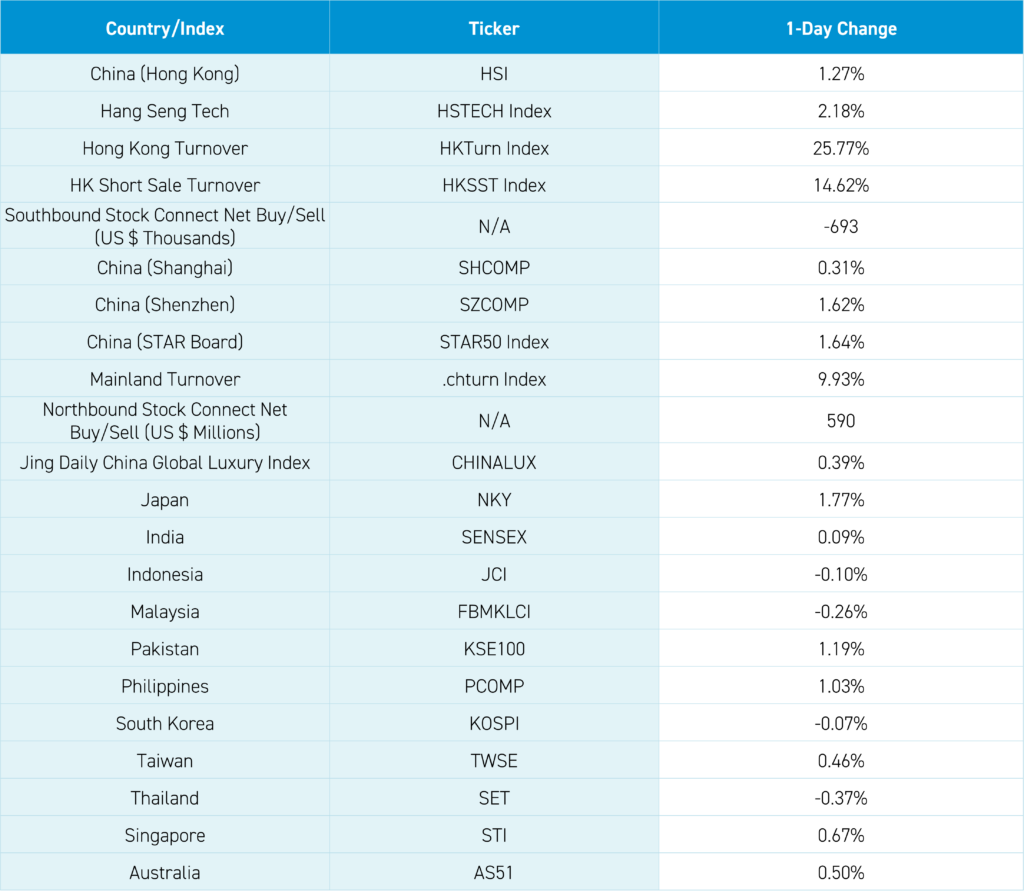

Asian equities had a strong day on decent volumes, as multiple markets gained +1%, including Japan, Hong Kong (not a typo), Mainland China's Shenzhen Composite, and the Philippines.

Hong Kong posted its first positive day in 2024, while Shanghai and Shenzhen posted their second positive day, which the negative nabobs of negativity are dismissing as a “technical rebound.” I agree that one day is one day, though there are both short-term catalysts behind today’s rally and several behind-the-scenes developments.

An interest rate cut is likely coming, though I would beg, “Where’s the beef?” (stolen from the 1980s slogan of US hamburger chain Wendy’s). China’s bond market saw a second day of profit-taking, indicating that it could be soon. According to Bloomberg News, the People's Bank of China (PBOC), China's central bank, tapped the brakes on CNY (Renminbi) weakness versus the US dollar while Deputy Governor Lu Lei met with economists on how to best support the economy. Mainland China news highlighted Deputy Prime Minister He's meeting with the China Securities Regulatory Commission (CSRC) International Advisory Committee on China’s continuing commitment to financial opening up. The National Development and Reform Commission (NDRC) is hosting a “symposium with private entrepreneurs” with the goal of supporting private enterprises.

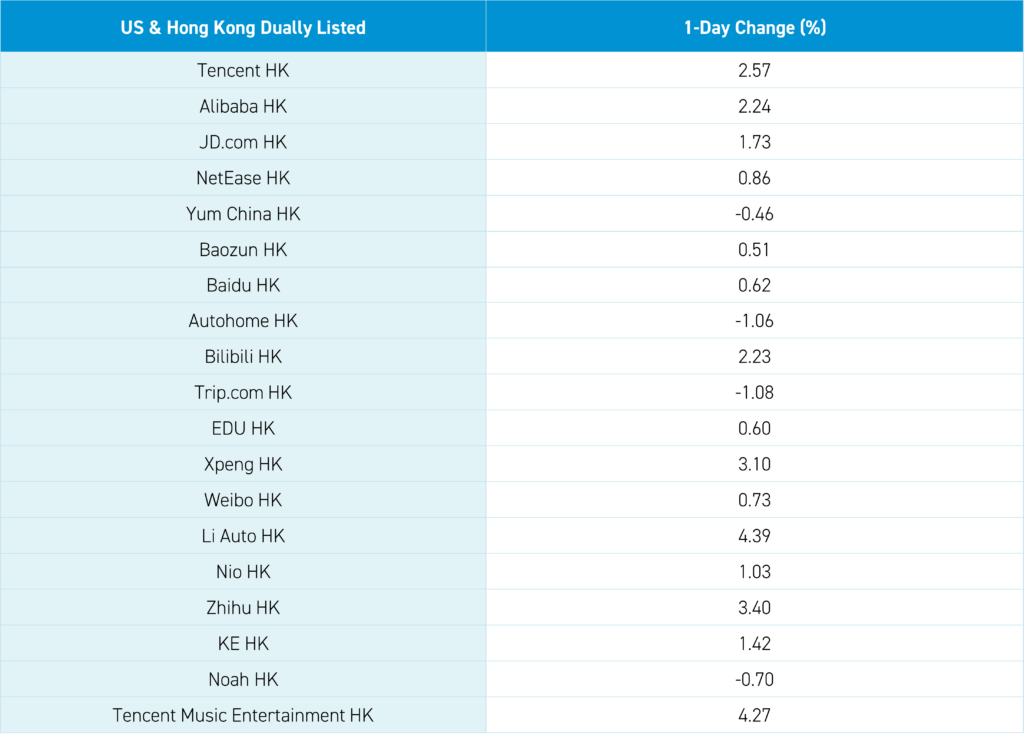

Food delivery company and super app Meituan gained +5.37% after announcing the first-ever buyback in the company’s history as they bought 5.6 million shares worth HKD 400 million after the stock slid from its Feb 2021 high of HKD $450 to today’s HKD $75.60 (revenue +149% from 2020 to 2023 estimated revenue). Tencent, which gained +2.57%, bought another 1.7 million shares worth HKD 500 million today as their epic buyback run continues. BYD gained +3.81% after launching their T5 light commercial truck. Wuxi Biologics gained +8.75% after yesterday’s +6.27% on strong financial results and guidance and Monday’s 52-week low.

Growth stocks/sectors led the way in both Hong Kong and China, which is a good sign as these are the names favored by domestic and foreign investors. Volumes were decent overall, though we’d like to see them even higher. Mainland investors punted their Hong Kong ETFs as their buy/sell behavior remains inexplicable. Mainland Chinese media noted the call option activity of a US-listed China ETF as a positive. Widely held growth stocks were leaders with the Mainland’s most heavily traded by value EV/solar battery maker CATL +2.76%, Tainqi Lithium +7.9%, Isoftstone Information +14.58%, Longi Green Energy +0.58% and BYD’s Mainland share class +3.41%. Foreign investors bought a healthy +$590mm of Mainland stocks via Northbound Stock Connect.

The bigger picture was several positives on stabilizing US-China diplomatic relations and poor/non-existent investor China positioning. Yesterday, President Xi wrote to his Iowa friends about the importance of US-China relations and Chinese military officials meeting their US equivalents in the first Pentagon meeting in 4 years. China’s Ambassador to the US gave a speech focused on the “positive measures to further open up and facilitate China-US exchanges and cooperation,” including China’s approval of Mastercard in China, Broadcom’s acquisition of VMware and Boeing 737 MAXs for flying in China (might want to consider that last one…….). Senior diplomat Liu Jianchao spoke at the Council on Foreign Relations on the importance of US-China relations. Mainland media noted, “The recent slew of interactions between the two countries shows that China is willing to enhance communication with the US at various levels and demonstrates China’s sincerity in trying to stabilize bilateral relations.” Diplomat Liu also met with a Deputy National Security Advisor. Notice the lack of US/Western media attention? Notice the lack of meetings with members of Congress? Rebuilding trust and confidence will take time, though I would argue it is happening.

Bloomberg News had an interesting article on a US bond manager buying distressed Chinese bond developers’ US bonds because “It’s bottomed here, but it’s still a long way to go to recover.” The FT noted a hedge fund doing the same! I can’t get anyone to look at our US $ Asia high-yield strategy. Bloomberg also had an article on US pensions reducing their China allocations: "We sense that international investors are just giving up trying to read China…” The article notes a London-based think tank survey of 100 pension and sovereign wealth managers that “found none of them have a positive outlook on China. " If that isn’t the sign of the bottom or at least being close to it I don’t know what is!!!! Not one! That’s absurd. It is also how bull markets are built!

The Hang Seng and Hang Seng Tech gained +1.27% and +2.18%, respectively, on volume that increased +25.77% from yesterday, which is 91% of the 1-year average. 342 stocks advanced, while 142 declined. Main Board short turnover increased by +14.62% from yesterday, which is 77% of the 1-year average, as 15% of turnover was short turnover. The growth factor and large caps outpaced the value factor and small caps. The top sectors were discretionary +2.32%, communication +2.11%, and tech +1.84%, while energy -1.71% and materials -0.28%. The top sub-sectors were media, auto, and retailing, with energy, consumer services, and telecom services being the worst. Southbound Stock Connect volumes were moderate as Mainland investors sold -$693mm of Hong Kong stocks and ETFs with Meituan, CCB, and Kuaishou small net buys while Tencent was a small net sell, Hong Kong Tracker ETF, HS China Enterprise ETF were moderate net sells.

Shanghai, Shenzhen, and STAR Board gained +0.31%, +1.62%, and +1.64%, respectively, on volume that increased +9.93% from yesterday, which is 82% of the 1-year average. 4,281 stocks advanced, while 657 declined. The growth factor and small caps outpaced the value factor and large caps. The top-performing sectors were Communication Services, which gained +2.86%, Technology, which gained +1.88%, and Consumer Discretionary, which gained +1.6%. Meanwhile, Energy fell -1.42% and Utilities fell -0.7%. The top-performing subsectors were internet, education, and fine chemicals, while petrochemicals, coal, and oil/gas were the worst. Northbound Stock Connect volumes were moderate as foreign investors bought $590mm of Mainland stocks, with BYD having a large net buy, TLC and Tongwei small net buys while Long Green Energy had a large net sell, Changan Auto and Kweichow Moutai moderate net sales. CNY and the Asia dollar index gained versus the US dollar. Treasury bonds were off small while copper gained and steel fell.

Last Night's Performance

Last Night’s Exchange Rates, Prices, & Yields

- CNY per USD 7.16 versus 7.16 yesterday

- CNY per EUR 7.86 versus 7.84 yesterday

- Yield on 10-Year Government Bond 2.49% versus 2.49% yesterday

- Yield on 10-Year China Development Bank Bond 2.71% versus 2.70% yesterday

- Copper Price +0.15%

- Steel Price -0.18%