Li Auto Shifts Into High Gear on Consumer Upgrade, Policy Support

3 Min. Read Time

Key News

Asian equities were largely lower except for Japan overnight. The Mainland market was mixed as small caps outpaced large caps while Hong Kong was hit with profit-taking.

Mainland China-listed consumer discretionary stocks were up +1.1%, led higher by home appliance makers and autos following President Xi’s press release last Friday on policy support for consumer upgrades, though thus far we lack specifics.

It was a quiet night before a busy week as we will have Vipshop and Baidu’s Q4 financial results on Wednesday, and then NetEase’s Q4 report and MSCI’s rebalance on Thursday after the close.

Next week is the “Two Sessions” policy meetings, which are China’s annual political meetings, comprised of the Chinese People’s Political Consultative Conference (CPPCC) and the National People’s Congress (NPC). These meetings will begin on Monday, March 4th. Policy support will be fully articulated into actionable items taken from December’s Central Economic Work Conference (CEWC), which focused on economic support through fiscal and monetary policy.

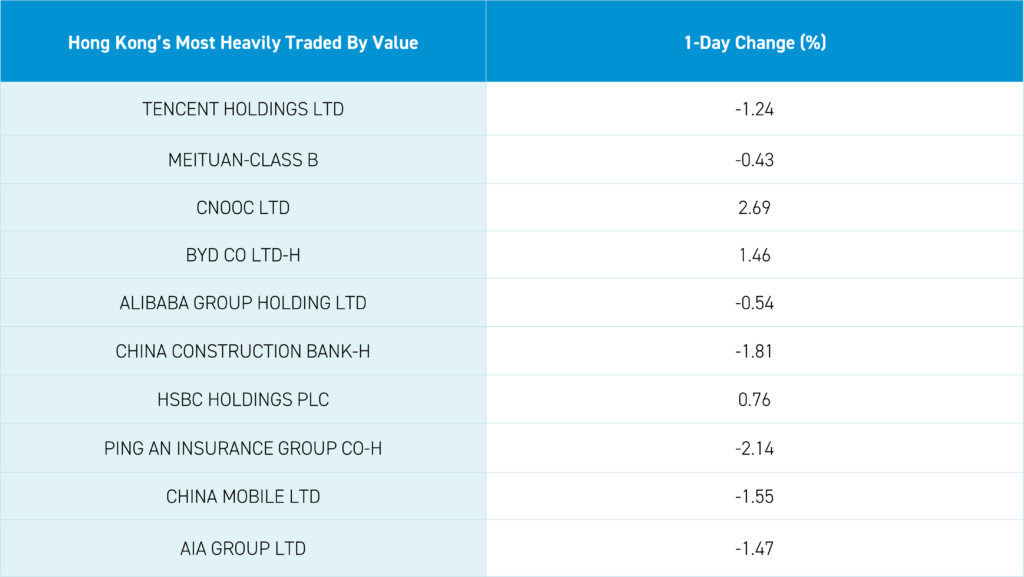

Hong Kong was off small though Mainland investors bought the dip via Southbound Stock Connect. Hong Kong’s most heavily traded stocks by value were Tencent, which fell -1.24%, Meituan, which fell -0.43%, energy giant CNOOC, which gained +2.69%, and BYD, which gained +1.46% on buyback announcements, and Alibaba, which fell -0.54%.

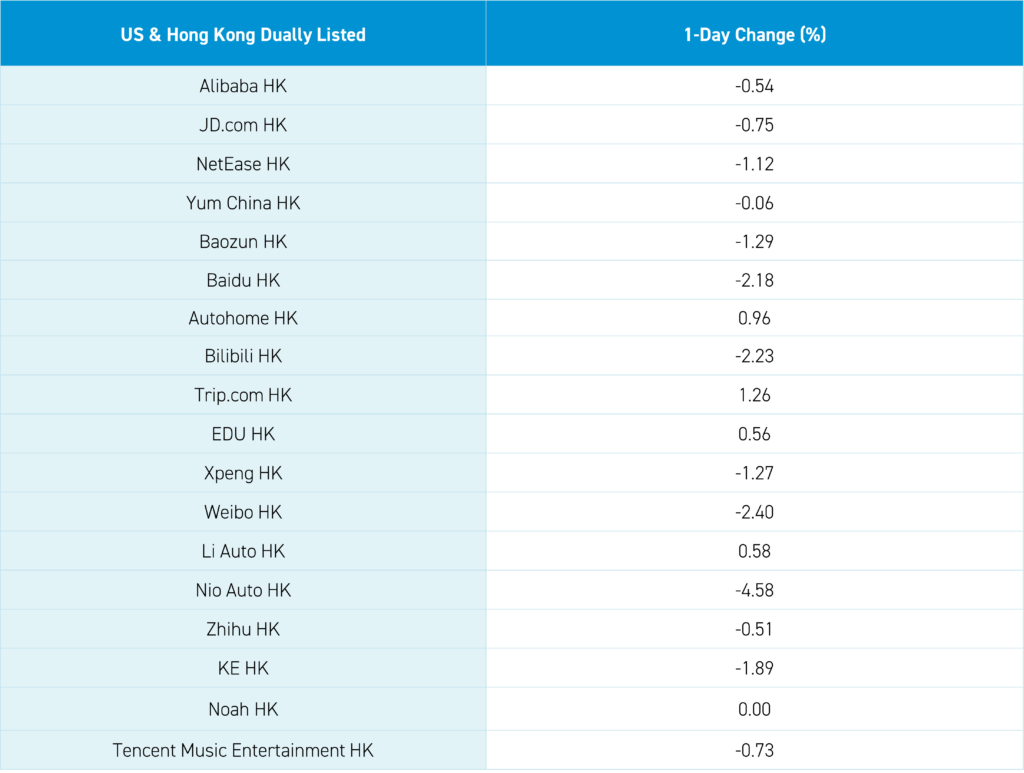

Electric SUV maker Li Auto gained +0.58% before reporting Q4 results that beat estimates on revenue, which was RMB 41.73 billion ($5.88 billion) compared to an expected RMB 39.79 billion ($5.39 billion). The company reported adjusted net income of RMB 4.59 billion ($646 million) versus an estimated RMB 3.45 billion ($480 million) and adjusted EPS of RMB 4.23 ($0.60), which was in line with estimates. Their Q1 revenue forecast was a touch light at RMB 31 billion versus an expected 32.

There was chatter on Congress looking at Pinduoduo’s Temu though remember committees and inquiries do not make laws! Additionally, a key proponent of the proposal is leaving Congress soon. The US is suffering from inflation but, ironically, still pushing import tariffs to make goods more expensive.

You may have seen a chart showing the decline of an Emerging Market ETF AUM versus the AUM growth of an EM ex China ETF from the nattering nabobs of negativity. I had dismissed commenting on the chart as I assumed most investors would recognize the EM ETF used has been in a secular decline for fifteen years. If one used any of the most popular broad EM ETF you would see strong AUM growth despite the China exposure. I was surprised to see a respected source use the same chart to validate their China underweight thesis. It is very disconcerting to see the cherry picking of bad/flawed data IMO. I’ll put a chart up on Twitter later today (@ahern_brendan).

The Hang Seng and Hang Seng Tech indexes fell -0.54% and -0.19%, respectively, on volume that decreased -13% from Friday, which is 84% of the 1-year average. 194 stocks advanced while 293 stocks declined. Main Board short sale turnover was relatively flat at +0.33% from Friday, which is 98% of the 1-year average as 20% of the turnover was short turnover (remember Hong Kong short turnover includes ETF short volume, which is driven by market makers’ ETF hedging). The growth factor and small caps “outperformed” (i.e. fell less than) the value factor and large caps. The top-performing sectors were Industrials, which gained +0.38%, Technology, which gained +0.37%, and Health Care, which gained +0.12%. Meanwhile, Materials fell -1.7%, Financials fell -1.64%, and Energy fell -1.38%. The top-performing subsectors were food, autos, and technical hardware. Meanwhile, insurance, telecom, and banks were among the worst-performing. Southbound Stock Connect volumes were moderate/light as Mainland investors bought a net $224 million worth of Hong Kong-listed stocks and ETFs, including CNOOC, which saw another large net buy, Li Auto, which was a moderate net buy, and Meituan, which was a small net buy. Meanwhile, the Hong Kong Tracker ETF, Tencent, and ICBC were all small net sells.

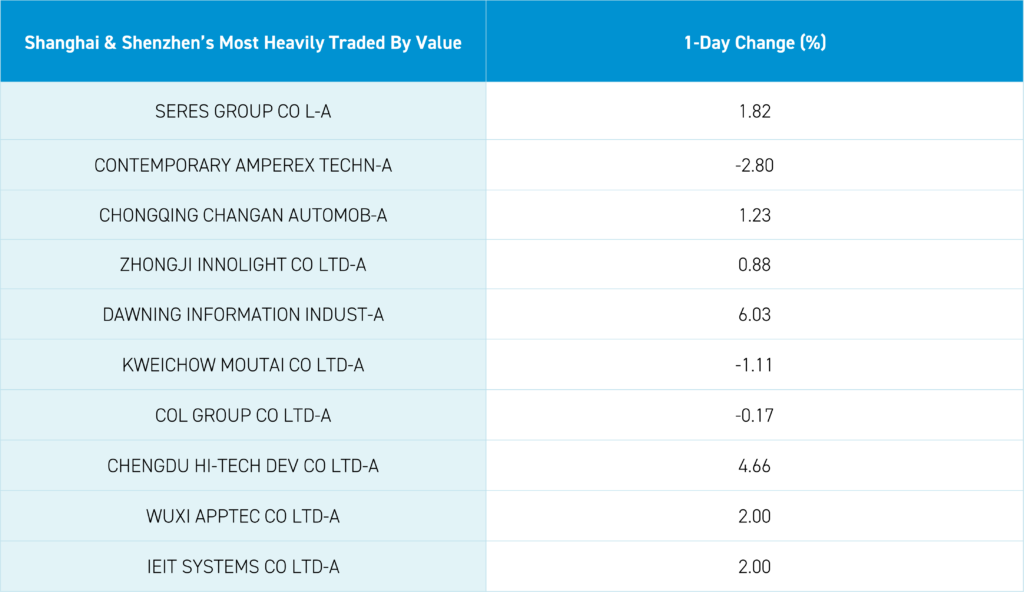

Shanghai, Shenzhen, and the STAR Board diverged to close -0.93%, +0.44%, and +0.52%, respectively, on volume that increased +7% from Friday, which is 115% of the 1-year average. 3,494 stocks advanced while 1,405 declined. The growth factor and small caps “outperformed” (i.e. fell less than) the value factor and large caps. The top-performing sectors were Consumer Discretionary, which gained +1.09%, Technology, which gained +0.23%, and Health Care, which flat. Meanwhile, Utilities fell -2.7%, Financials fell -2.05%, and Energy fell -1.93%. The top-performing subsectors were industrial machinery, education, and computer hardware. Meanwhile, insurance, banking, and the power industry were among the worst-performing. Northbound Stock Connect volumes were moderate as foreign investors sold a net -$182 million worth of Mainland stocks. Midea, Foxconn, and China Merchants Bank (CMB) were moderate net buys. Meanwhile, Changan Auto, CATL, and Haier were small net sells. CNY and the Asia dollar index were off slightly versus the US dollar, treasury bonds rallied, and copper and steel were lower.

Last Night's Performance

Last Night’s Exchange Rates, Prices, & Yields

- CNY per USD 7.20 versus 7.20 yesterday

- CNY per EUR 7.81 versus 7.79 yesterday

- Yield on 1-Day Government Bond 1.48% versus 1.48% yesterday

- Yield on 10-Year Government Bond 2.38% versus 2.40% yesterday

- Yield on 10-Year China Development Bank Bond 2.53% versus 2.56% yesterday

- Copper Price -0.33% overnight

- Steel Price -0.92% overnight