JD.com Beats as Financial Heads Hold a Two Sessions Press Conference

3 Min. Read Time

Key News

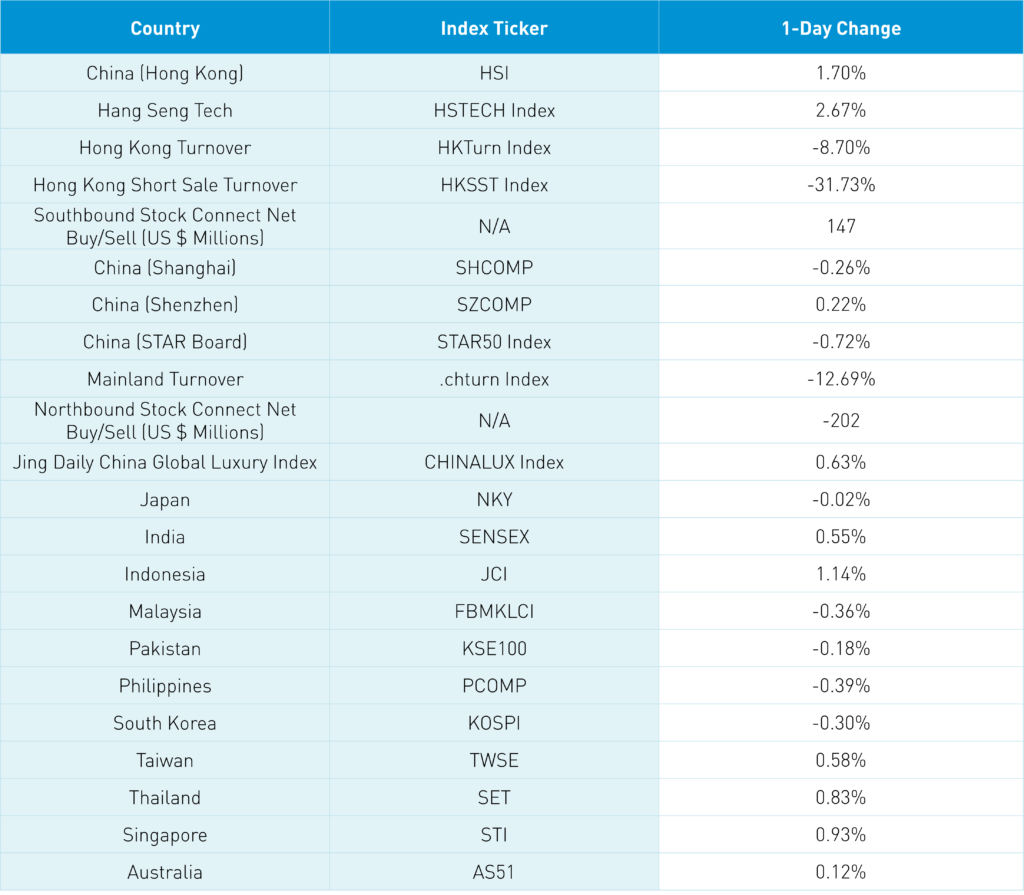

Asian equities were largely higher as Hong Kong and Indonesia outperformed.

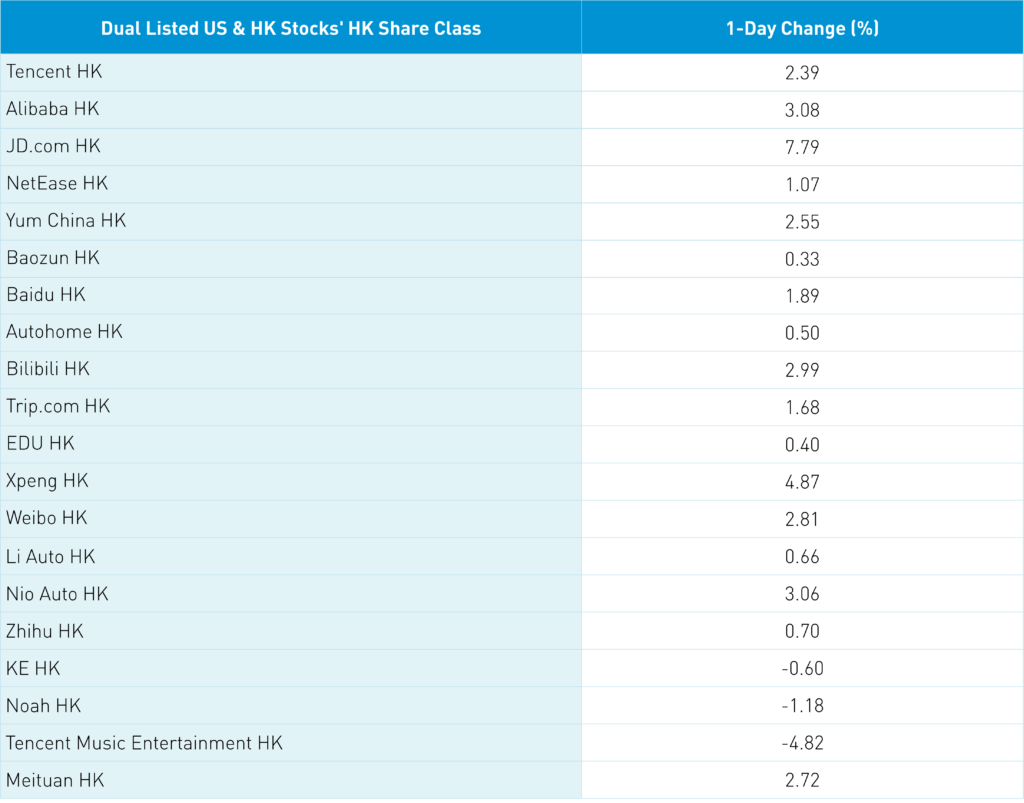

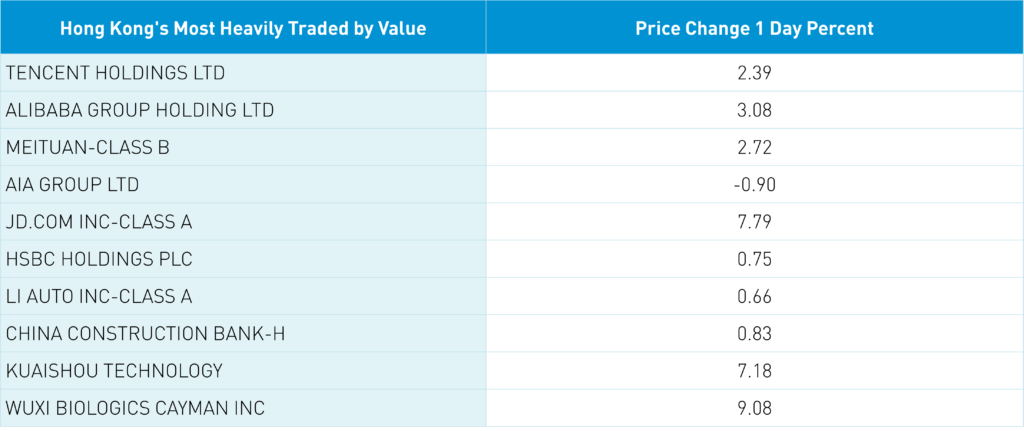

Hong Kong had a strong day, led by growth stocks on above-average volumes, as all sectors were positive. Breadth (advancers versus decliners) was strong after an ugly start to the week. However, volume was off a touch versus yesterday’s down day and we would prefer strong buying. Anticipation of the Two Sessions press conference and JD.com’s financial results beating estimates might have been a factor as Hong Kong’s most heavily traded stocks by value were Tencent, which gained +2.39%, Alibaba, which gained +3.08%, Meituan, which gained +2.72%, AIA Group, which fell -0.90%, and JD.co, which gained +7.79%.

Mainland investors were net buyers of Hong Kong stocks to the tune of $147 million, including Tencent, which saw two days of net buying after six days of net sells. Mainland China was mixed as foreign investors were net sellers of -$202 million worth of Mainland China stocks via Northbound Stock Connect. A Mainland media source noted that yesterday was the strongest inflow day ever for Mainland equity ETFs with RMB 30.711B ($4.266B) in net inflow. The two large-cap, equity ETFs favored by the National Team, with tickers of 510310 and 510300, had $1.14 billion and $696 million worth of inflow yesterday, respectively, while three other ETFs inflows of $583 million (mid-caps), $410 million (large-caps), and $404 million (micro-caps). Wow!

We will not have the usual post-Two Sessions press conference from the Premier, but there was an all-star press conference held by financial department heads today after the Mainland’s close. Participants included National Development and Reform Commission (NDRC) Director Zheng Shanjie, Minister of Finance Lan Fo’an, Minister of Commerce Wang Wentao, PBOC Governor Pan Gonsheng, and CSRC (China’s SEC) Chairman Wu Qing.

JD.com Earnings Highlights

JD.com (JD US, 9618 HK) reported Q4 results after the Hong Kong close/pre-US open. The results beat on the big three: revenue, adjusted net income, and adjusted EPS. JD.com founder and Chairman Richard Liu is clearly fed up about JD.com’s position versus other e-commerce players and is taking action. Crazy stat: Since 12/31/2020 through yesterday’s close, JD’s US ADR/stock has underperformed its US dollar bond due in 2030 by 67%!

- Revenue increased by +3.6% to RMB 306.1B ($43.1B) versus expectations of RMB 299B ($41.68B)

- Adjusted net income was RMB 8.4B ($1.2B) versus Q4 2022 RMB 7.7B, and expectations of RMB 7.2B ($1.01B), which implied -7% YoY

- Adjusted EPS was RMB 5.30 ($0.75) versus Q4 2022 RMB 4.81, and expectations of RMB 4.56 ($0.63), which implied -6% YoY

- JD.com will pay a dividend of $0.38 for US ADR (paying out $1.2B)

- Announced a new share repurchase program of $3B over the next 36 months

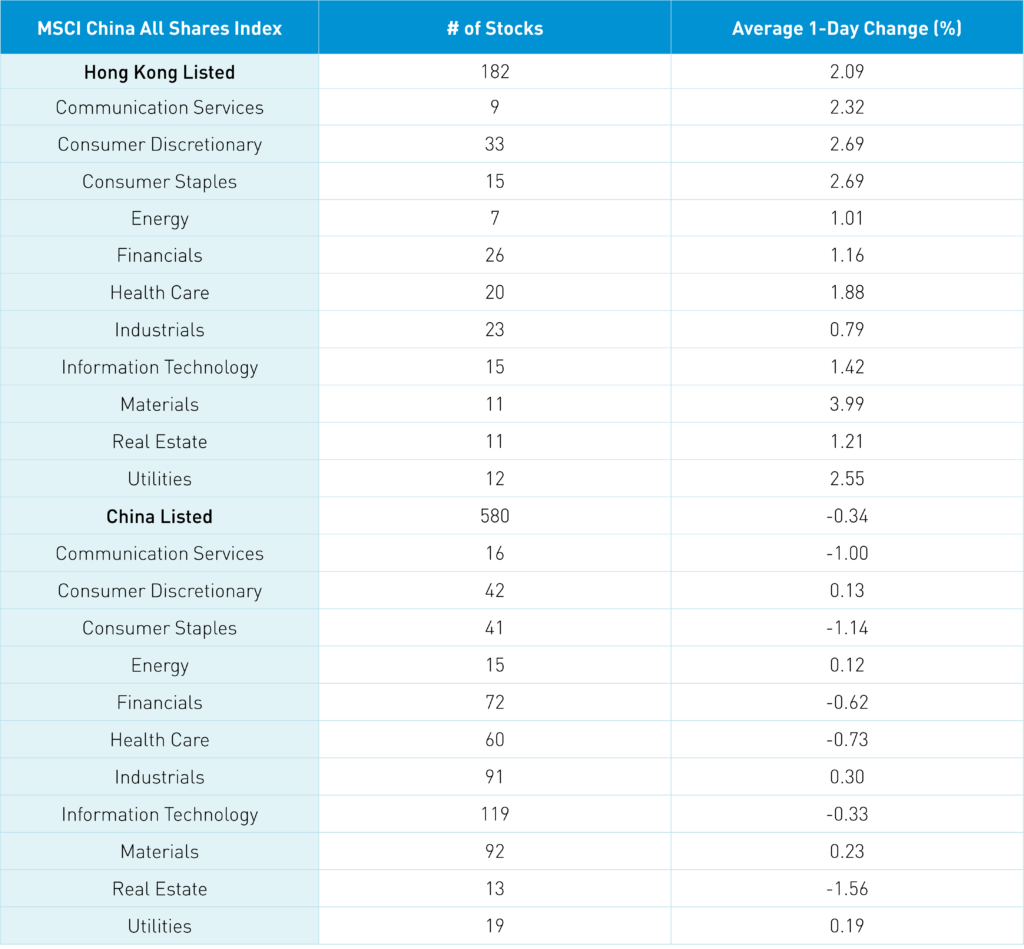

The Hang Seng and Hang Seng Tech indexes gained +1.70% and +2.67%, respectively, on volume that decreased -8.7% from yesterday, which is 103% of the 1-year average. 385 stocks advanced, while 96 declined. Main Board short turnover declined -31.73% from yesterday, which is 90% of the 1-year average turnover (remember Hong Kong short turnover includes ETF short volume, which is driven by market makers’ ETF hedging). All factors were positive, as the growth factor and small caps outperformed the value factor and large caps. All sectors were positive led by Materials, which gained +3.98%, Consumer Discretionary, which gained +2.68%, and Consumer Staples, which gained +2.68%. The top-performing subsectors were software, retail, and materials. Meanwhile, media and business products were among the worst-performing. Southbound Stock Connect volumes were moderate/light as Mainland investors bought a net $147 million worth of Hong Kong-listed stocks and ETFs, including Tencent, which was a moderate/large net buy, China Mobile and CNOOC, which were small net buys. Meanwhile, PetroChina, ICBC, and China Construction Bank (CCB) were small net sells.

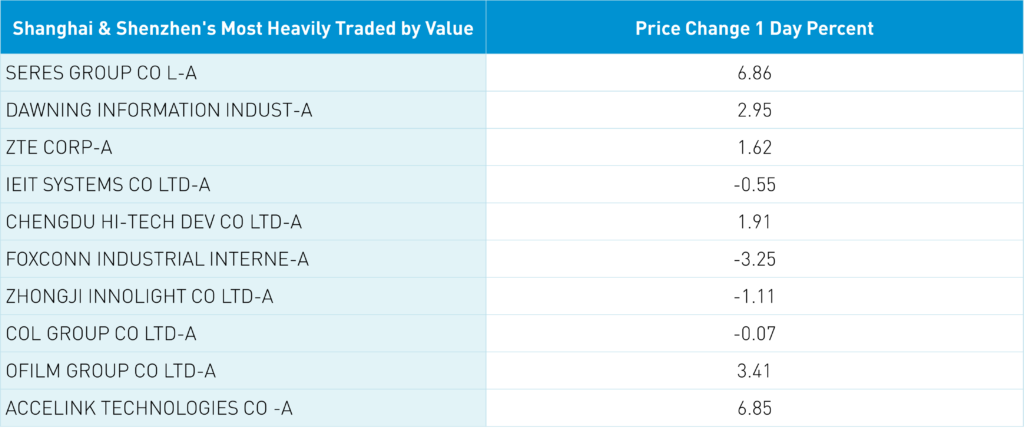

Shanghai, Shenzhen, and the STAR Board diverged to close -0.26%, +0.22%, and -0.72%, respectively, on volume that declined -12.69% from yesterday, which is 107% of the 1-year average. 3,176 stocks advanced, while 1,697 declined. The growth factor and small caps outpaced the value factor and large caps. The top-performing sectors were Industrials, which gained +0.29%, Materials, which gained +0.23%, and Utilities , which gained +0.19%. Meanwhile, Real Estate fell -1.56%, Consumer Staples fell -1.14%, and Communication Services fell -1.00, making up the worst-performing sectors. The top-performing subsectors were power generation equipment, motorcycles, and construction machinery. Meanwhile, semiconductors, liquor, and cultural media were among the worst-performing. Northbound Stock Connect volumes were moderate as foreign investors sold a net -$202 million worth of Mainland stocks, including Cypc, Sokon, and LCXX. Meanwhile, Kweichow Moutai was a moderate net sell, and CATL and LXJM small net sells. CNY was off slightly versus the US dollar. Treasury bonds rallied while copper and steel were off.

Last Night's Performance

Last Night's Exchange Rates, Prices, & Yields

- CNY per USD 7.19 versus 7.19 yesterday

- CNY per EUR 7.82 versus 7.81 yesterday

- Yield on 10-Year Government Bond 2.26% versus 2.31% yesterday

- Yield on 10-Year China Development Bank Bond 2.36% versus 2.42% yesterday

- Copper Price -0.19%

- Steel Price -0.83%