Rally Takes a Breather on Macro & Micro Factors

2 Min. Read Time

Key News

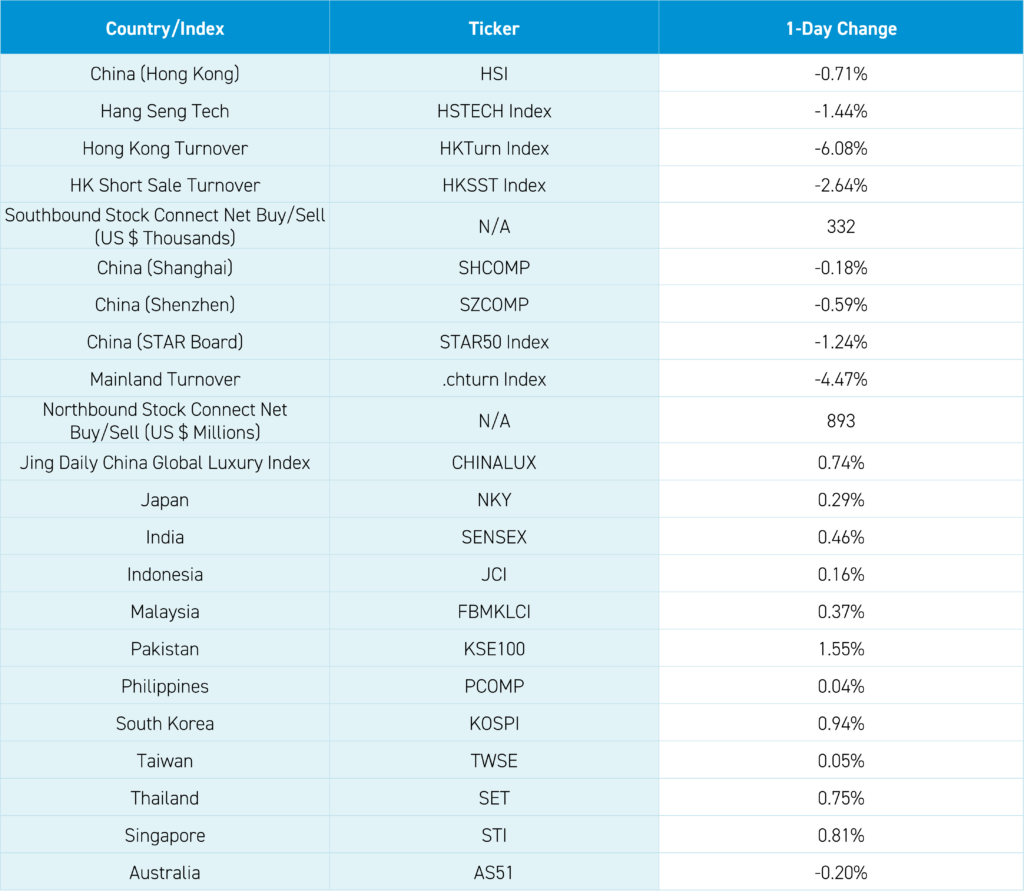

Asian equities were largely higher except for South Korea, Mainland China, and Hong Kong. Macro/top-down and micro/bottom-up factors weighed on the markets, though one could also argue they were due for a breather after a strong run from January lows.

The "Two Sessions" policy meetings have provided verbal policy support for the economy, though markets will want to see exact measures to be enacted. I jinxed things yesterday by mentioning the resiliency of the Chinese markets despite a very negative Western media narrative. The House’s TikTok ban vote weighed on investor sentiment as recent growth stock/sector outperformers underperformed. Semis were the worst sub-sector in both markets. Wuxi Biologics and Wuxi AppTec fell -13.08% and -12.12% on a biotech lobbying group dropping their support of the companies in light of Congressional efforts to prevent the companies receiving any compensation from healthcare providers that receive federal funding. Like TikTok, Congress acts as judge, jury, and executioner of private companies without providing evidence. Similar to the TikTok ban, I assume both will be challenged in court, where evidence needs to be provided.

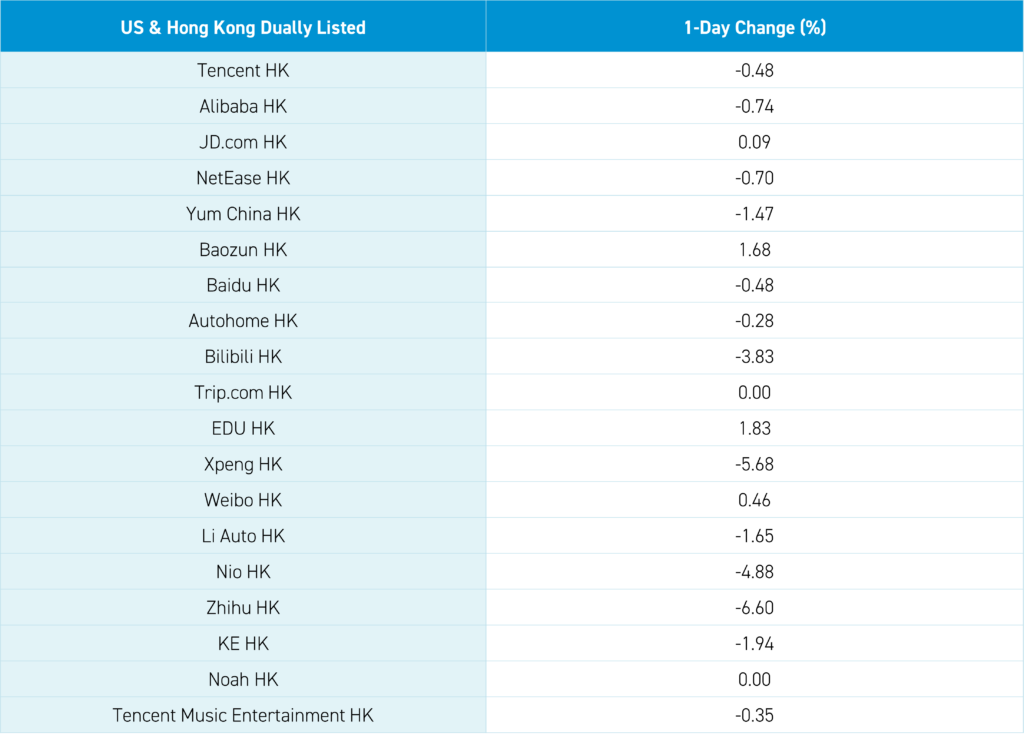

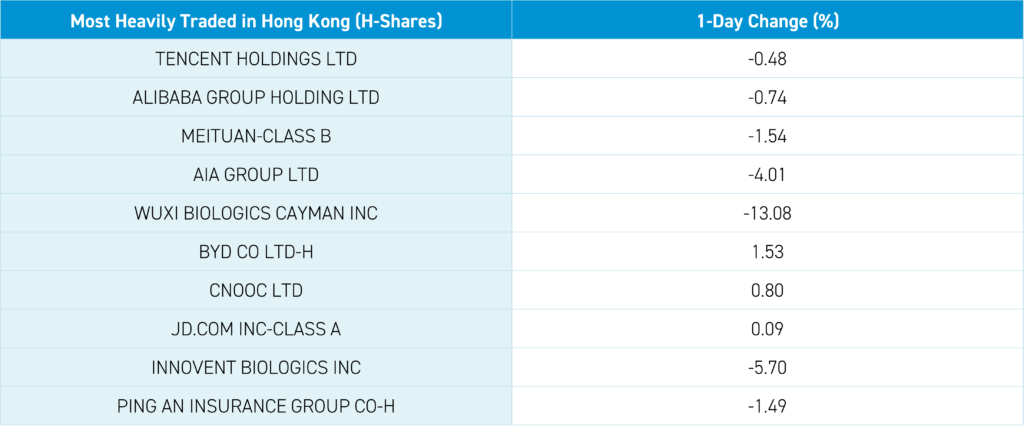

Interestingly, several Chinese and Hong Kong healthcare stocks rallied from policy support from the Two Sessions. Value stocks/sectors rallied, with real estate rebounding on policy support. Hong Kong was off led lower by recently outperforming growth stocks/sectors, with Hong Kong’s most heavily traded by value Tencent -0.48%, Alibaba HK -0.74%, Meituan -1.54%, AIA -4.01% and Wuxi Biologics -13.08%. Mainland investors bought the Hong Kong dip via Southbound Stock Connect.

Mainland China was off, though Northbound Stock Connect saw a healthy net buying of $893mm. The National Team’s two favored ETFs, tickers 510300 CH and 510310 CH, saw a jump in afternoon trading as the Mainland market fell, indicating they might have been buying. The medium-term lending facility rate is expected to remain at 2.5%, though there is a fair amount of chatter on continued easing. We shall see!

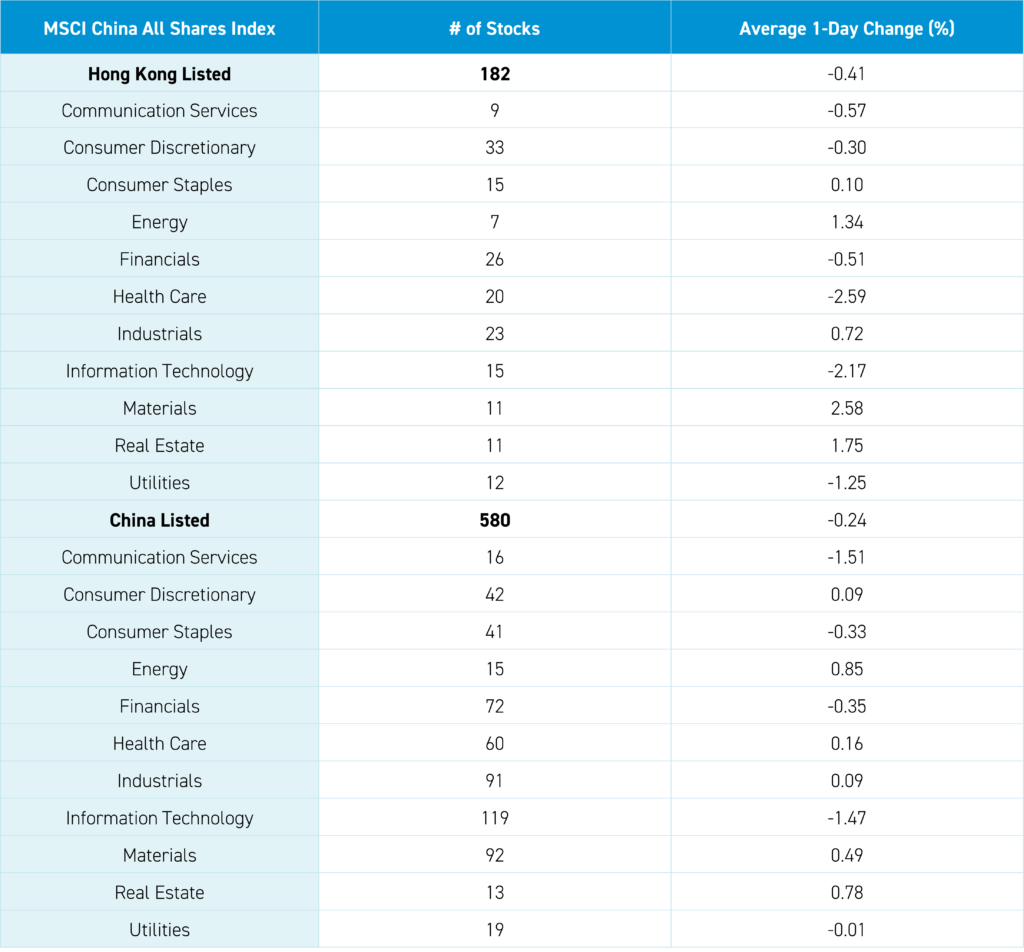

The Hang Seng and Hang Seng Tech fell -0.71% and -1.44% on volume -6.01% from yesterday, 115% of the 1-year average. 194 stocks advanced, while 279 declined. Main Board short turnover declined -2.62% from yesterday, which is 131% of the 1-year average as 20% of turnover was short turnover (remember Hong Kong short turnover includes ETF short volume, which is driven by market makers’ ETF hedging). The value factor and small caps “outperformed”/fell less than the growth factor and large caps. The top sectors were materials +2.58%, real estate +1.75%, and energy +1.34%, while healthcare -2.59%, tech -2.17% and utilities -1.25%. The top sub-sectors were materials, food/staples, and consumer durables, while semis, pharmaceuticals, and insurance were the worst. Southbound Stock Connect volumes were high as Mainland investors bought $332mm of Hong Kong stocks and ETFs with Sinopec, Tigermed, and China Mobile small net buys while Meituan was a small net sell, Hong Kong Tracker and Wuxi Biologics moderate net sells.

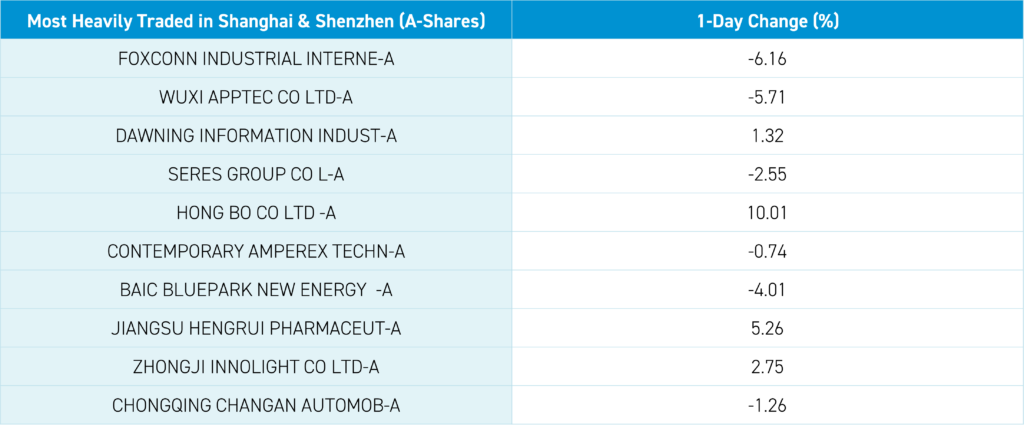

Shanghai, Shenzhen, and STAR Board fell -0.18%, -0.59%, and -1.24% on volume -4.47% from yesterday, 116% of the 1-year average. 1,094 stocks declined, while 3,798 declined. The value factor and small caps “outperformed”/fell less than the growth factor and large caps. Top sectors were energy +0.84%, real estate +0.78%, and materials +0.48%, while communication -1.51%, tech -1.48%, and financials -0.35%. The top sub-sectors were precious metals, airports, and marine, while internet, cultural media, and semis were the worst. Northbound Stock Connect volumes were moderate/high as foreign investors bought a healthy $893mm of Mainland stocks with Wuliangye, Cits, and Zijin Mining moderate/large net buys while Wuxi AppTec had moderate/large net sell, LXJM, and Mindray moderate net sales. CNY was off versus the US dollar. Treasury bonds were off. Copper was up while steel was off.

Last Night's Performance

Last Night’s Exchange Rates, Prices, & Yields

- CNY per USD 7.18 versus 7.19 yesterday

- CNY per EUR 7.86 versus 7.86 yesterday

- Yield on 10-Year Government Bond 2.34% versus 2.33% yesterday

- Yield on 10-Year China Development Bank Bond 2.48% versus 2.47% yesterday

- Copper Price +2.36%

- Steel Price -1.66%