Index Rebalances Lift Volumes, Week in Review

3 Min. Read Time

Week in Review

- Asian equities were mixed for the week as China outperformed and the Hang Seng Tech Index rallied +5% and is close to being positive year-to-date.

- The “Two Sessions” important policy meetings concluded this week with multiple supportive indications, including potential incentives for trade-ins of appliances and vehicles, which could help improve consumer confidence.

- Sports apparel maker Li Ning announced plans to go private, which boosted its stock this week.

- The US House passed a bill to potentially force a sale of TikTok’s US operations, though multiple lawmakers expressed hesitation over the bill and how fast it was pushed through. Meanwhile, Trump said he did not support a ban because of the market power it would hand to Meta.

Key News

Asian equities were largely lower as China and Malaysia outperformed while South Korea, Indonesia, the Philippines, and Hong Kong underperformed.

Overseas investors appeared to be worried about stickier US inflation and US interest rates staying higher for longer after yesterday’s higher-than-expected US producer price index (PPI) release as the US dollar gained overnight. Today was a significant trading day as Hong Kong volumes spiked on FTSE Russell, Nasdaq, and S&P Dow Jones index rebalances, and Triple Witching as stock index futures, stock index options, and single stock futures expire. Today’s liquidity allows institutional investors to adjust their positions as the jump in volumes hides their movements.

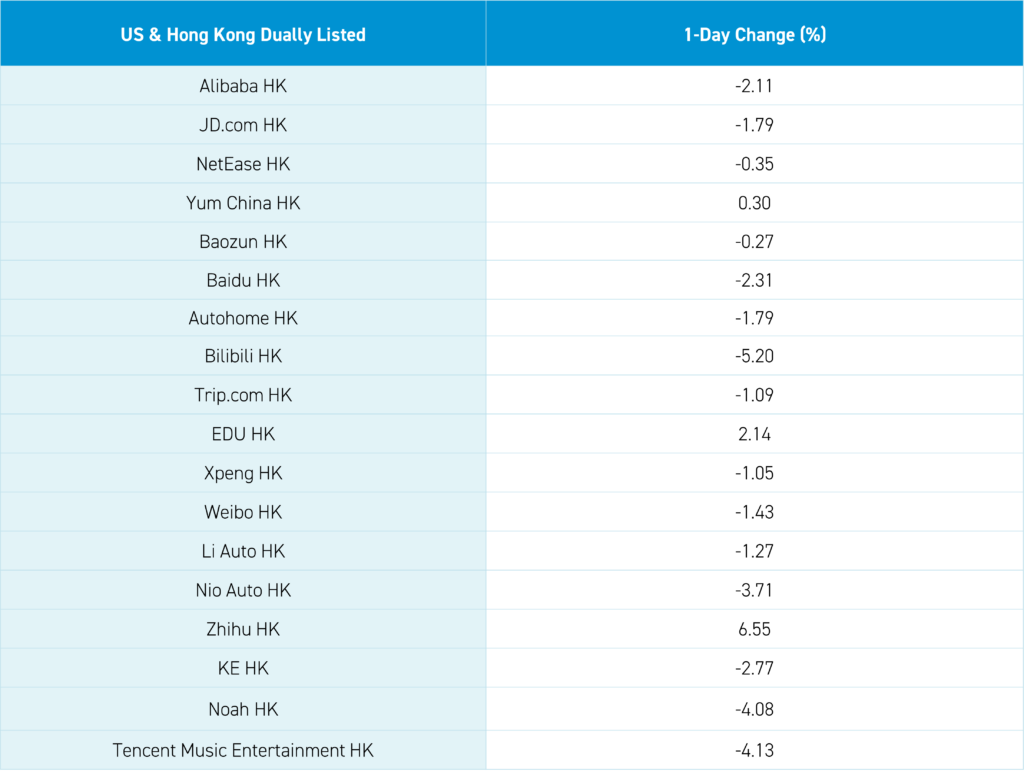

Although Hong Kong was off, it was not off as much as US-listed China stocks were yesterday and came off intra-day lows as Mainland investors bought the dip via Southbound Stock Connect. Shanghai and Shenzhen also rose from a lower morning to close higher on strong Northbound Stock Connect volumes, which resulted in $1.4 billion worth of net buying as China stocks were bought by funds tracking FTSE indexes.

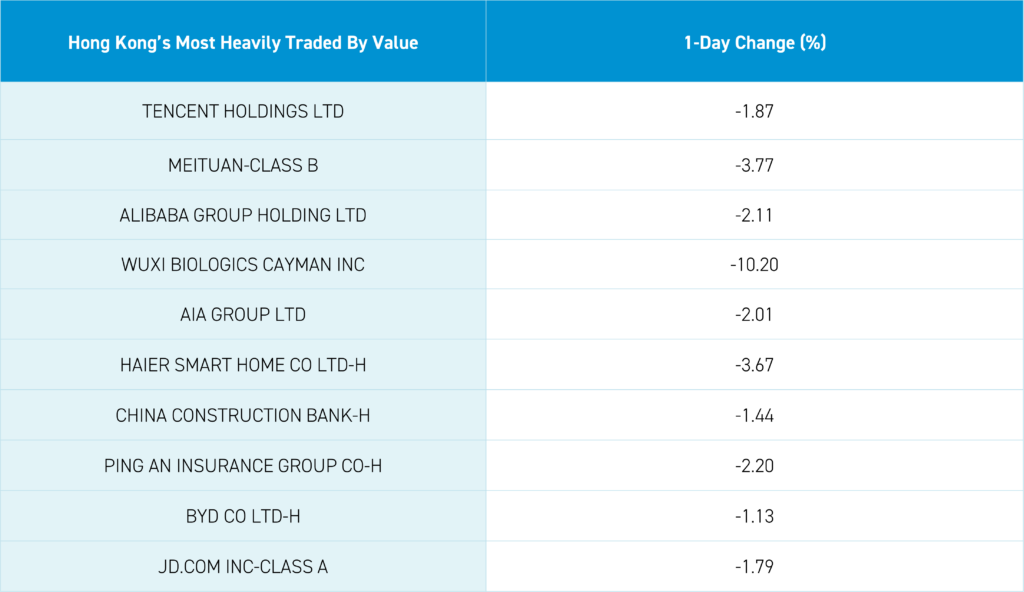

As the Mainland market swooned, there was a temporary increase in the National Team’s favorite ETFs’ volumes. Hong Kong and Mainland China-listed semiconductor stocks had a strong day on chatter that there will be a push to use more domestic chips in electric vehicle (EV) production. Wuxi Biologics fell -10.2% and WuXi AppTec fell -8.79% after the trade association clarified that the companies left the association on their own accord after the group supported legislation effectively banning the companies from US federal contracts. While TikTok’s ban gets the most attention, the false accusations against these companies are highly disconcerting as a certain Congressional committee becomes judge, jury, and executioner without any evidence. This is why this, like TikTok’s ban, will likely go to court.

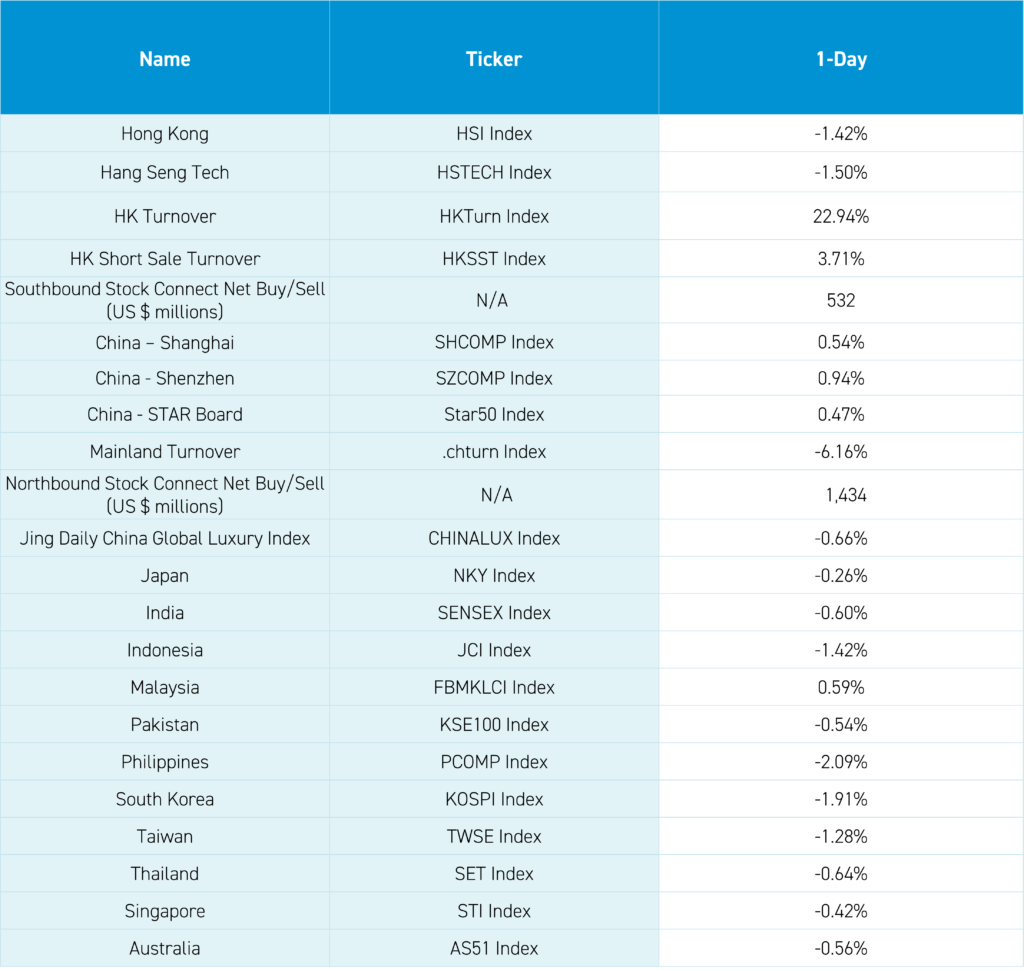

The 1-year medium-term lending facility rate (MLF) was left unchanged at 2.5%. Meanwhile, new and used home prices fell again month-over-month, which weighed on real estate in Mainland China, where it fell -0.76%, and Hong Kong, where it fell -1.99%. Money Supply/M2 was in line while new loans and aggregate financing increased month-over-month.

Vice Chairman of the China Securities Regulatory Commission (CSRC) Li Chao spoke on encouraging companies to pay more dividends and punishing corporate fraud.

It was a quiet night, though we have a busy week of Q4 financial results next week!

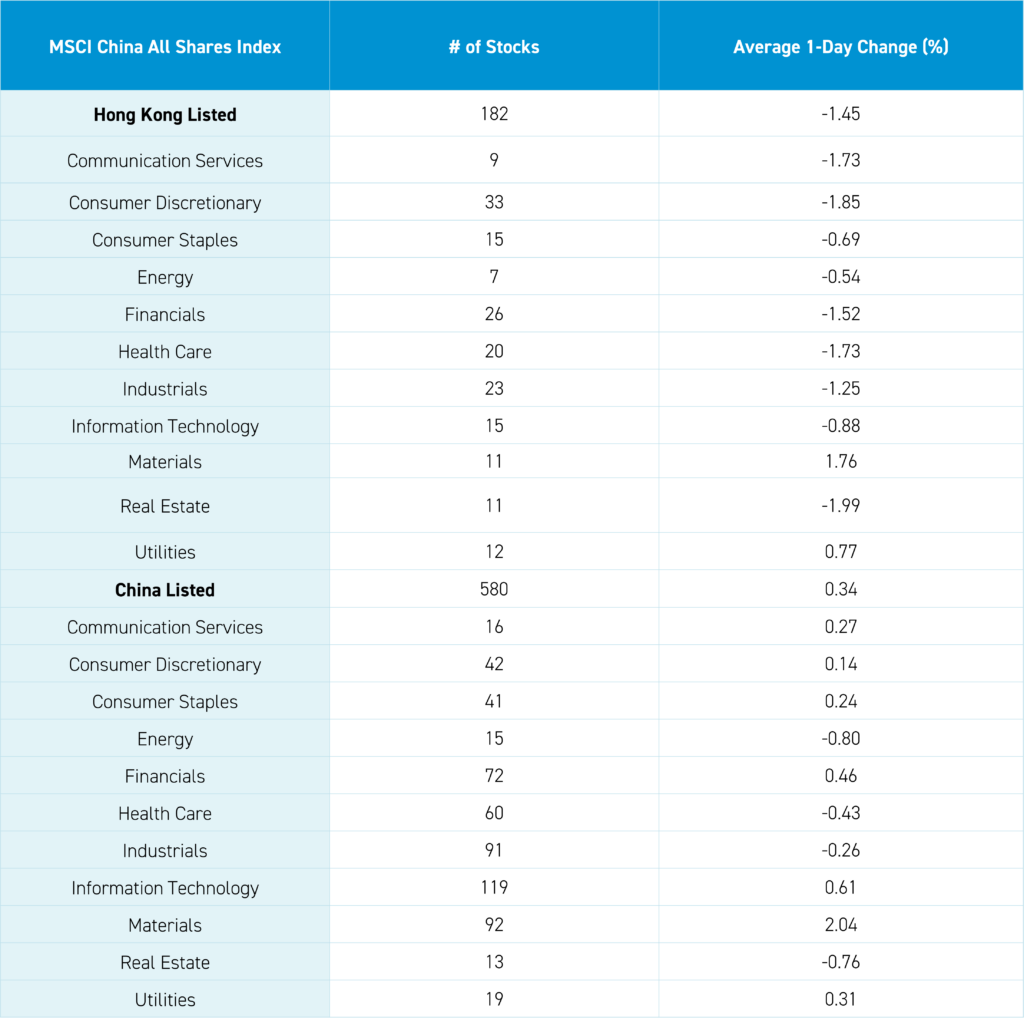

The Hang Seng and Hang Seng Tech indexes fell -1.42% and -1.50%, respectively, on volume that increased +22.94% from yesterday, which is 141% of the 1-year average. 148 stocks advanced while 344 stocks declined. Main Board short turnover increased +3.7% from yesterday, which is 135% of the 1-year average, as 17% of turnover was short turnover (remember Hong Kong short turnover includes ETF short volume, which is driven by market makers’ ETF hedging). All factors were negative with the value factor falling slightly less than the growth factor. Materials and Utilities were the only positive sectors, gaining +1.76% and +0.78%, respectively, while Real Estate fell -1.98%, Consumer Discretionary, which fell -1.85%, and Health Care, which fell -1.73%. Materials, utilities, and semiconductors were the only positive subsectors while media, insurance, and retail were among the worst-performing. Southbound Stock Connect volumes were high as Mainland investors bought a net $532 million worth of Hong Kong-listed stocks and ETFs, as Bank of China, China Mobile, and PetroChina were small net buys. Meanwhile, Wuxi Biologics, Tencent, and Meituan were moderate net sells.

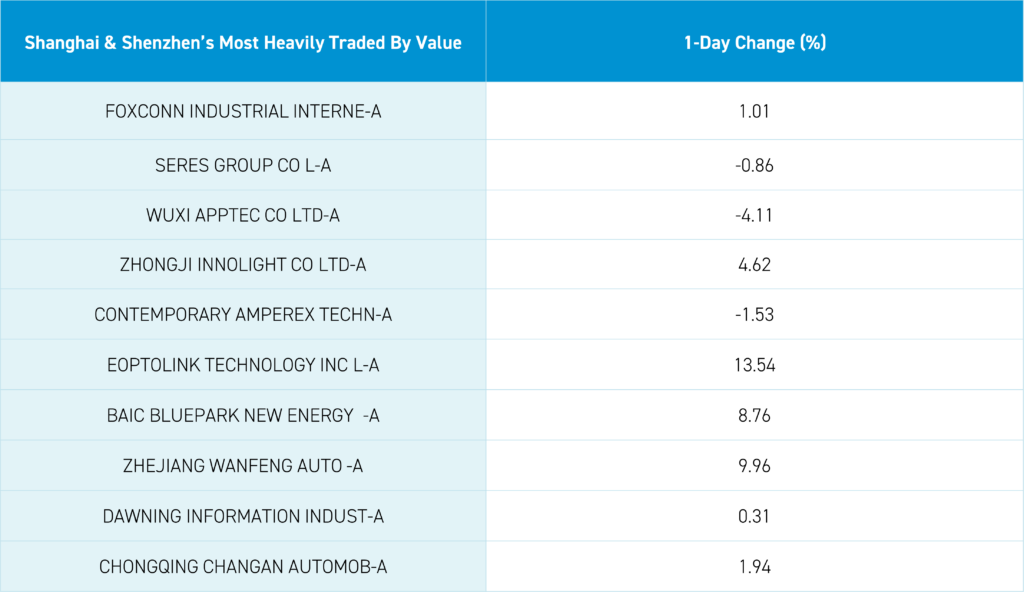

Shanghai, Shenzhen, and the STAR Board gained +0.54%, +0.94%, and +0.47%, respectively, on volume that decreased -6.16% from yesterday, which is 89% of the 1-year average. 3,806 stocks advanced while 1,091 declined. The value factor and large caps outperformed the growth factor and small caps. The top-performing sectors were Materials, which gained +2.04%, Technology, which gained +0.61%, and Financials, which gained +0.45%. Meanwhile, Energy fell -0.8%, Real Estate fell -0.76%, and Health Care fell -0.43% to form the worst-performing sectors. The top-performing subsectors were precious metals, base metals, and environmental protection industries. Meanwhile, power generation equipment, coal, and household appliances were among the worst-performing subsectors. Northbound Stock Connect volumes were high as foreign investors bought a healthy $1.43 billion worth of Mainland stocks, including PAB, Wuliangye Yibin, and HR, which were moderate net buys. Meanwhile, LONGi Green Technology, Aier Eye Hospital, and Kweichow Moutai were small net sells. CNY and the Asia Dollar Index were off versus the US dollar. Treasury bonds rallied. Copper gained while steel fell.

Last Night’s Performance

Last Night’s Exchange Rates, Prices, & Yields

- CNY per USD 7.20 versus 7.19 yeste

- CNY per EUR 7.84 versus 7.83 yesterday

- Yield on 1-Day Government Bond 1.48% versus 1.48% yesterday

- Yield on 10-Year Government Bond 2.32% versus 2.34% yesterday

- Yield on 10-Year China Development Bank Bond 2.45% versus 2.48% yesterday

- Copper Price +1.00%

- Steel Price -1.38%