Risk Off On Middle East Tensions & Trade Data, Week in Review

4 Min. Read Time

Week in Review

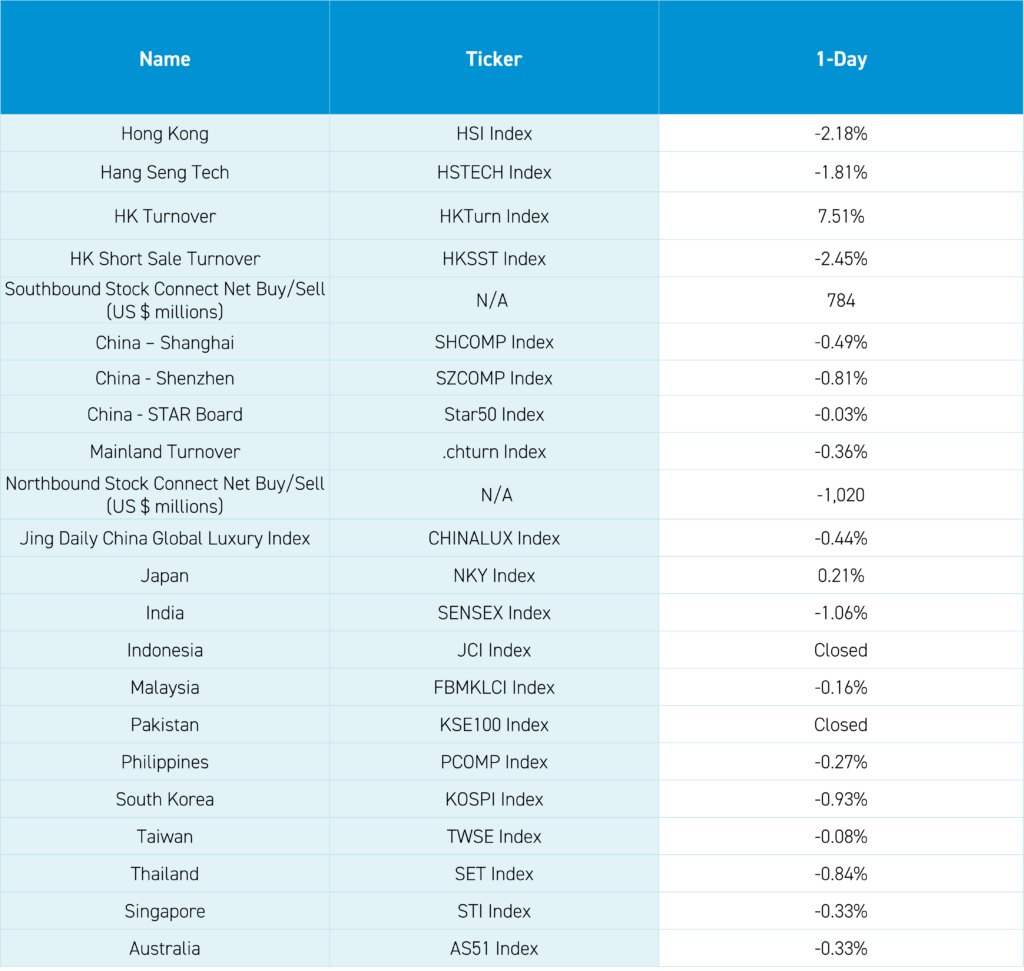

- Asian equities were mostly lower for the week, though Hong Kong-listed internet and technology stocks managed gains.

- US Treasury Secretary Janet Yellen was in China this week and had many productive meetings with Premier Li, People’s Bank of China (PBOC) Chair Pan Gongsheng, Vice Premier He Lifeng, and Ministry of Finance Head Lan Fo'an.

- China’s March inflation, as measured by the official consumer price index (CPI), came in at +0.1% year-over-year, below estimates and February’s figure, despite a rise in pork prices.

- The electric vehicle ecosystem had a strong week on fresh data from the China Association of Automobile Manufacturers (CAAM) showing that March new energy vehicle sales were up +35% year-over-year.

Key News

Asian equities ended the week with a thud, with Indonesia and Pakistan closed for Eid al-Fitr. The US dollar was a wrecking ball overnight, causing the Asia Dollar Index to decline by -0.19% as the South Korean Won underperformed by -0.89% overnight, with the US 10-year Treasury yield over 4.5%.

The Middle East “tensions” are potentially escalating, leading to today’s risk-off-market move, with safe havens such as gold and the US dollar surging. The South China Morning Post noted Secretary of State Blinken spoke with Foreign Minister Wang Yi about trying to keep Iran from retaliating against Israel.

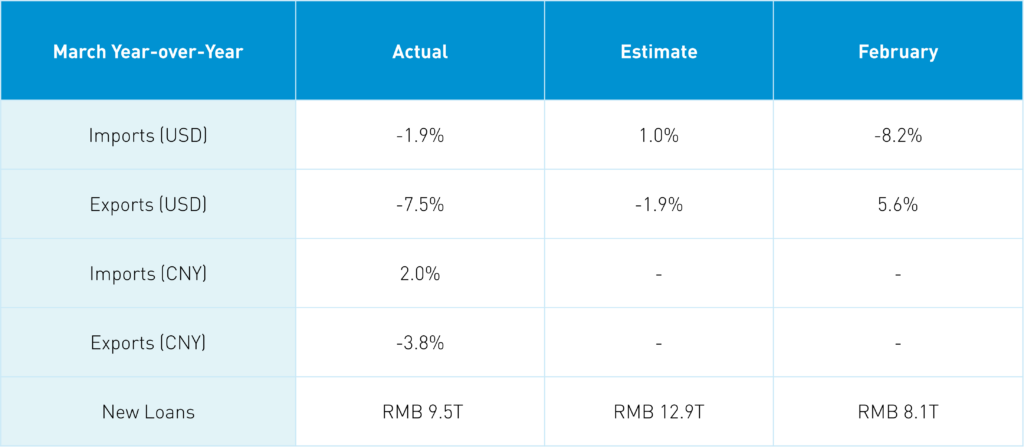

Hong Kong opened lower and slid throughout the trading day, while Shanghai and Shenzhen bounced around the room on weak trade data, leading to a late-day selloff.

In CNY terms, the numbers were not as bad. Some argued that the trade data, which is reported year-over-year, was likely distorted by the Chinese New Year taking place in February, though a miss is still a miss. All told, the data is not a great sign for the global economy. New loans and aggregate financing increased, a sleeper positive as low rates in China are not the issue. Rather, what needs to be solved is the demand for loans.

Nonetheless, markets were in a foul mood. Also in focus were reports of new Mainland financial regulations, including an examination of offerings of Hong Kong insurance products to Mainland investors.

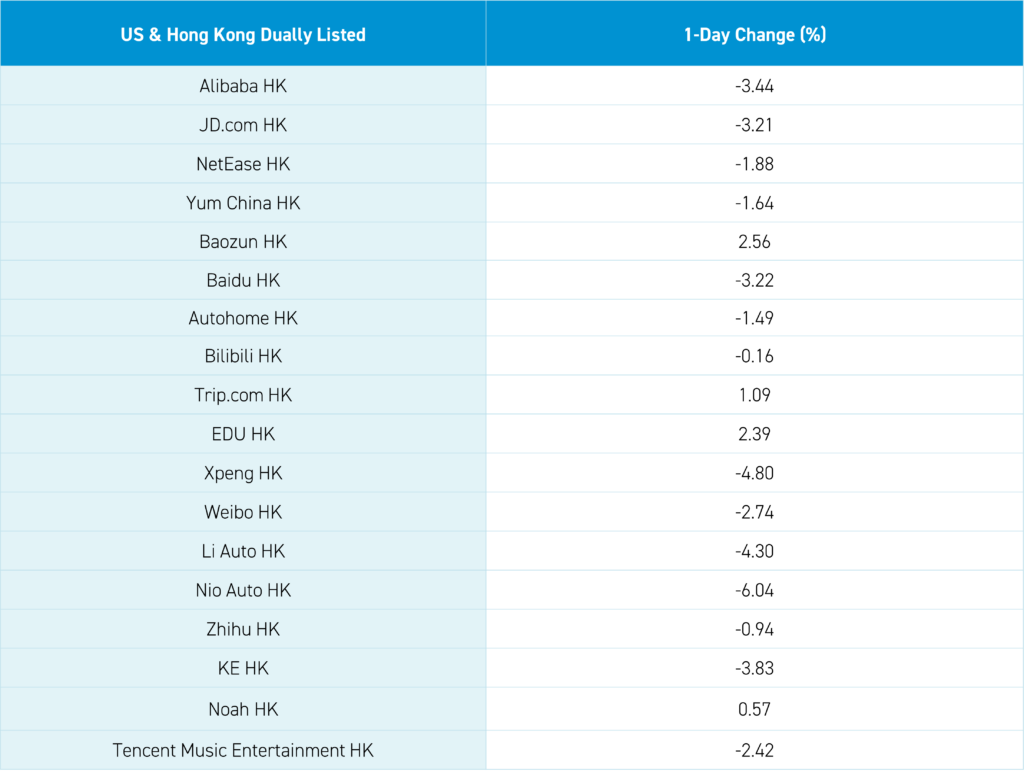

Hong Kong’s most heavily traded stocks by value were Tencent, which fell -1.71%, buying 3.2 million shares today, AIA, which fell -5.81% on the insurance sales examination, Xiaomi, which gained +2.61% on an analyst upgrade, Alibaba, which fell -3.44%, and Meituan, which fell -2.3% after buying 3.9 million shares today. Trip.com gained +1.09%, a rare bright spot, though growth stocks held up better (i.e. fell less than) value stocks.

Today’s loss wiped out what would have been a decent week as the Hang Seng fell below 17,000 level to close at 16,721. Mainland investors bought the dip in size with a healthy $784 million worth of net buying of Hong Kong-listed stocks and ETFs. Mainland China was not off as much Hong Kong overnight, though Mainland markets underperformed for the week. Foreign investors sold Mainland stocks in size, with $1.02 billion worth of net selling, which didn’t help sentiment. Precious metals shined amid high gold prices. The Shanghai Composite is sitting above the 3,000 level and Shenzhen is sitting above the 1,700 level.

Export-driven manufacturing has supported the economy since the end of COVID restrictions. However, today’s data should pressure policy makers to step on the domestic consumption gas pedal. There was chatter regarding continued progress on auto and home appliance repurchase plans, though no one told JD.com shareholders as its stock fell -3.21%.

The Wall Street Journal reported that Chinese telecom companies were told to replace US semiconductor companies by 2027 according to “people familiar with the matter”. However, I did not see anything in China media on this, so your guess is as good as mine.

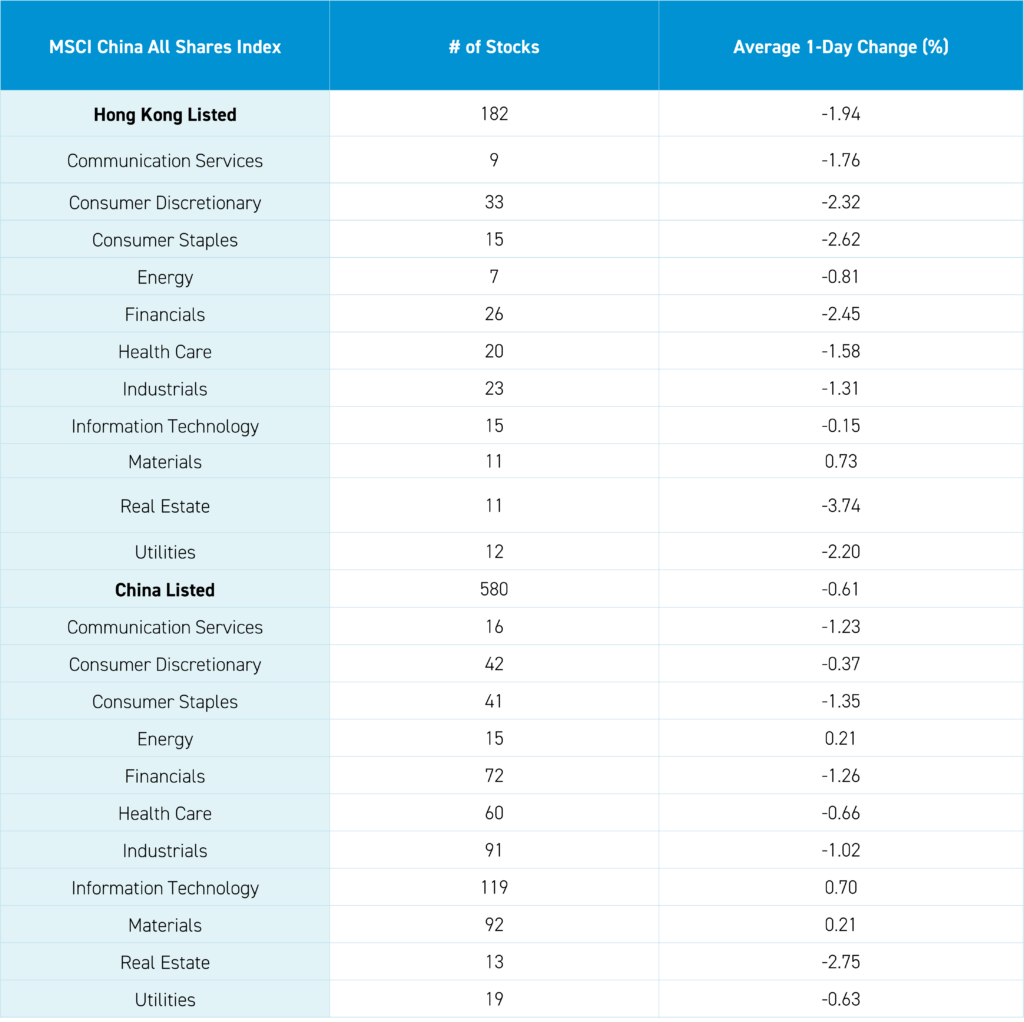

The Hang Seng and Hang Seng Tech indexes fell -2.18% and -1.81%, respectively, on volume that increased +7.51% from yesterday, which is 109% of the 1-year average. 87 stocks advanced while 405 stocks declined. Main Board short turnover decreased -2.45% overnight, which is 117% of the 1-year average, as 19% of turnover was short turnover (remember Hong Kong short turnover includes ETF short volume, which is driven by market makers’ ETF hedging). All factors were negative as the growth factor and large caps fell less than the value factor and small caps. Materials represented the only positive sector, gaining +0.73%. Meanwhile, Real Estate fell -3.74%, Consumer Staples fell -2.62%, and Financials fell -2.45%. The top-performing subsectors were technical hardware, food & beverage, and materials. Meanwhile, insurance, retail, and semiconductors were among the worst-performing. Southbound Stock Connect volumes were moderate as Mainland investors bought $784 million worth of Hong Kong-listed stocks and ETFs, including Bank of China, Xiaomi, and China Mobile, which were moderate net buys. Meanwhile, Anta Sports, Tencent, and Li Auto were small net sells.

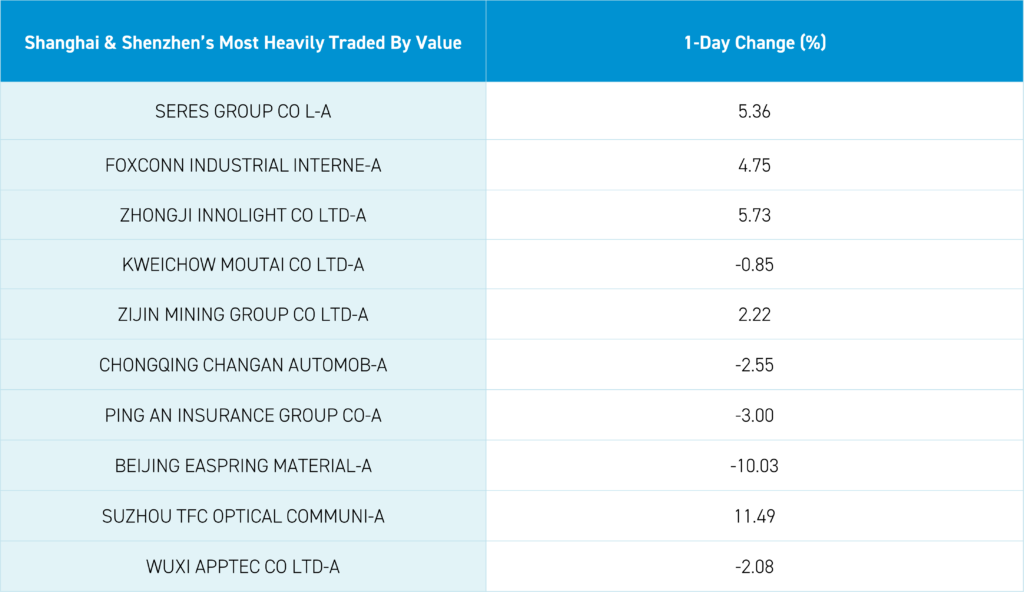

Shanghai, Shenzhen, and the STAR Board fell -0.49%, -0.81%, and -0.03%, respectively, on volume that decreased -0.36% from yesterday, which is 94% of the 1-year average. 1,837 stocks advanced while 3,098 declined. The growth factor and large caps fell less than the value factor and small caps. The top-performing sectors were Technology, which gained +0.7%, Energy, which gained +0.21%, and Materials, which also gained +0.21%. Meanwhile, Real Estate fell -2.75%, Consumer Staples fell -1.35% and Financials fell -1.26%. The top-performing subsectors were precious metals, marine/shipping, and motorcycles. Meanwhile, insurance, diversified financials, and fine chemicals were among the worst-performing. Northbound Stock Connect volumes were moderate/light as foreign investors sold a healthy net -$1.02 billion worth of Mainland stocks, including Gigadevice, BOE Technology, and Kingsoft Office, which were small net buys. Meanwhile, Ping An, Foxconn, and Kweichow Moutai were large net sells. CNY and the Asia Dollar Index were off versus the US dollar overnight. Treasury bonds rallied. Copper and steel were higher.

Last Night’s Performance

Last Night’s Exchange Rates, Prices, & Yields

- CNY per USD 7.24 versus 7.24 yesterday

- CNY per EUR 7.69 versus 7.76 yesterday

- Yield on 1-Day Government Bond 1.48% versus 1.49% yesterday

- Yield on 10-Year Government Bond 2.28% versus 2.29% yesterday

- Yield on 10-Year China Development Bank Bond 2.40% versus 2.42% yesterday

- Copper Price +0.14%

- Steel Price +0.64%