China Health Care Fuels Exports in May

3 Min. Read Time

Key News

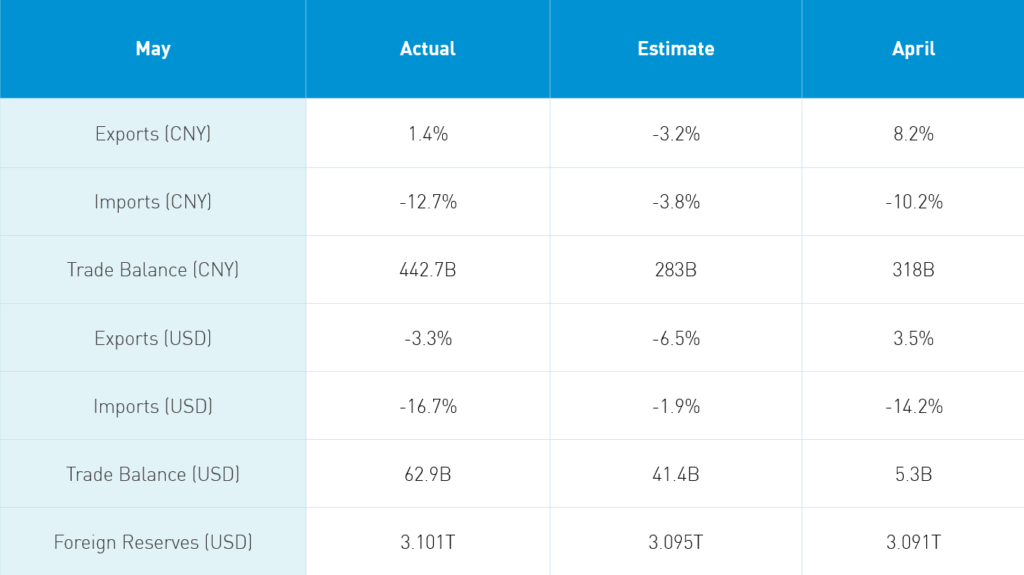

Expectations going into today’s release were fairly low due to the economic consequence of global quarantines. Exports showed resilience. Rumor has it that medical exports helped fuel the surprise strength in exports. Supply chains coming online likely helped as well. However, imports were hurt by the drop in commodity prices and a difficult year-over-year comparison. The interpretation that the import number indicates China’s consumer is weak should be dismissed as consumer demand is slower on the uptake than production and Chinese consumers are increasingly buying domestic goods and services. Overall, this is a positive release considering the circumstances. If global re-openings go well the June figures could see a nice jump.

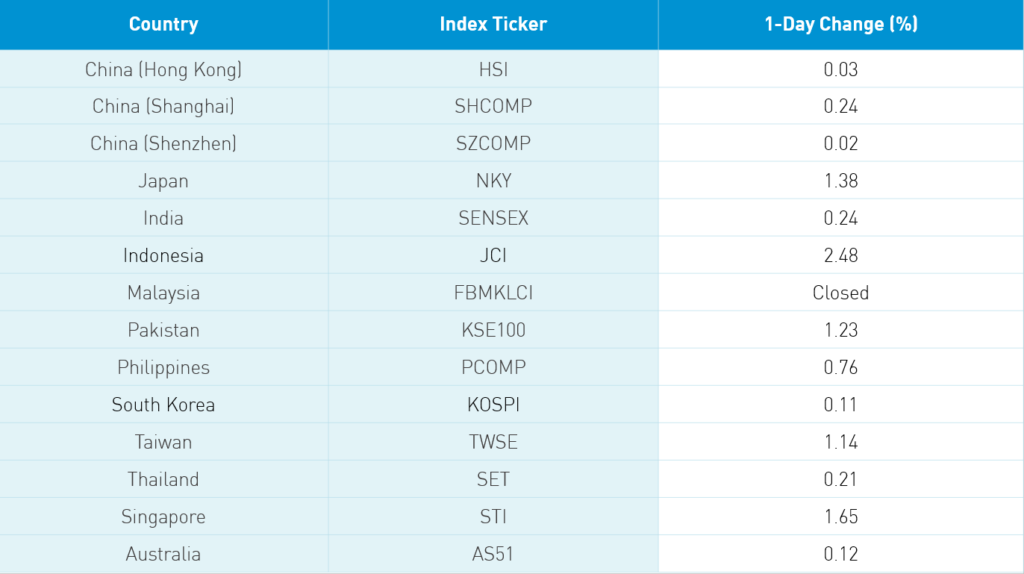

Asian equities had a nice start to the week fueled by the great US jobs release Friday, the lack of new US-China political rhetoric, and the easing of quarantine restrictions across the globe. Hong Kong and Mainland China managed modest gains as many markets play catch up to China’s first in first out (FIFO) advantage. Growth names were weak in Hong Kong with volume leaders Tencent -0.97%, Meituan Dianping -2.64%, Alibaba HK +0.09% and Xiaomi -1.23%. Growth names could be lagging due to Thursday’s NetEase HK relisting IPO as investors raise cash to participate.

Energy stocks outperformed as oil spot prices continue to rise. Geely Auto rose +1.7% after reporting strong May sales in yet another sign that China’s auto market may have bottomed. Apple supplier and panel maker BOE Tech ripped +9.22% on news it will be Apple’s 5G iPhone screen maker. Healthcare was lower despite reports of a human antibody clinical trial beginning and the strong export release. Several growth sectors have seen profit-taking that has resulted in underperformance the last week or so. I believe reversion to the mean is taking place as the laggards play catch up.

We have received a question regarding what will happen if the House passes the Senate’s version of the Equitable Act and President Trump signs the bill into law, thereby requiring the PCAOB to audit US-listed Chinese companies over a three-year time frame. Obviously, there remain many contingencies including whether the House sends the bill to committee, whether the Chinese regulator changes the law, or whether a compromise is reached allowing private companies to allow their auditors to release their working papers to the PCAOB. Regardless, we are several years from the nuclear option. US-listed Chinese companies are relisting in Hong Kong at a steady pace. They are doing so regardless of this issue and with the hope of more interest in their stocks from within Asia and higher valuations as a result. As these companies relist in Hong Kong, US shares may be converted to Hong Kong shares. If we get the nuclear option and the clock runs out with no changes occurring, would unconverted shares become a zero? I believe the shares would likely still trade though Over the Counter on the pink sheets. The tickers would likely become five letter tickers. Nestle’s US-listed ADR (NSRGY US) is not sponsored meaning the company didn’t approve of the custodian bank issuing the ADR. As a result, the company doesn’t file with the SEC. My thesis is only conjecture at this point though I have a call today that should clarify the issue. I’ll report back tomorrow.

H-Share Update

The Hang Seng traded in a tight range with small swings between gains and losses to close +0.03%/+6 index points at 24,776 on volumes -4% from Friday though still above the 1-year average. Breadth was mixed with 25 advancers and 23 decliners led by China Construction Bank -1.56%/-32 index points, HSBC +1.23%/+31 index points and Tencent -0.97%/-23 index points. Hang Seng Bank was the day’s best performer +3.41%/+11 index points while Hengan International Group was the worst -3.43%/-4 index points. Hong Kong-domiciled companies outperformed China-domiciled companies +0.47% versus -0.57% using the HS HK 35 and HS China Enterprise Indexes as proxies. The Chinese companies listed in Hong Kong within the MSCI China All Shares Index eased -0.67% with energy +1.48%, industrials +0.17%, tech -0.0%, financials -0.34%, real estate -0.35%, utilities -0.46%, materials -0.61%, communication -0.98%, discretionary -1.14%, staples -1.87%, and healthcare -1.97%.

Southbound Stock Connect volumes were moderate in mixed trading. Tencent and Meituan Dianping were both sold by Mainland investors while Semiconductor Manufacturing saw net buying. Mainland investors bought $62mm of Hong Kong-listed stocks as Southbound Connect accounted for 7.7% of Hong Kong turnover.

A-Share Update

Shanghai & Shenzhen also traded in a tight range managing gains of +0.24% and +0.02% to close at 2,937 and 1,856. Volumes were +8.5% from Friday while breadth was off 1,483 advancers and 2,118 decliners. Large caps outperformed mid and small caps today. The Mainland stocks within the MSCI China All Shares Index rose +0.27% with real estate +1.4%, energy +1.37%, materials +1.03%, discretionary +0.92%, utilities +0.68%, financials +0.48%, industrials +0.46%, tech +0.37%, staples -0.16%, healthcare -1.04%, and communication -1.13%.

Northbound Stock Connect volumes were moderate in mixed trading as Shanghai saw inflows while Shenzhen was mixed with some slight selling. Volume leader BOE Technology saw buyers outpace sellers by 2 to 1, Kweichow Moutai was sold 3 to 2 and Inner Mongolia Yili was bought 3 to 1. Foreign investors bought $86mm worth of Mainland stocks today as Northbound Stock Connect accounted for just over 6% of Mainland trading.

Last Night’s Prices & Yields

- CNY/USD 7.07 versus 7.08 Friday

- CNY/EUR 7.99 versus 8.01 Friday

- Yield on 1-Day Government Bond 1.90% versus 1.13% Friday

- Yield on 10-Year Government Bond 2.81% versus 2.85% Friday

- Yield on 10-Year China Development Bank Bond 3.13% versus 3.17% Friday