Cannonball Coming! Updated Ant Group Hong Kong Filing Review

4 Min. Read Time

Highlights From Ant Group's Latest Filing

The filing begins with a letter from Executive Chairman Eric Jing stating that in 2014 “Alipay pioneered online escrow payments to solve the problem of settlement risk due to a lack of trust between online buyers and sellers.” The company followed with “Quick Pay” ten years ago, the Yu’ebao money market fund seven years ago, and a merchant QR code payment system three years ago. The company commits 0.3% of annual revenues to charity while also supporting the Ant Forest reduction program, which has planted 200 million trees. So, let’s get into the fun stuff.

Who owns Ant Group? How large is the IPO?

Hangzhou Junhan and Hangzhou Junao hold 29.86% and 20.66 (50.52%) of total shares. Those entities are owned by Hangzhou Junao, of which Jack Ma owns 34% along with Eric Jing, Simon Hu and Fang Jiang, who hold 22% each. The filing states “Mr. Jack Ma has ultimate control over our Company.” Alibaba the company owns 33% while on page 145 it states Alibaba owns 730 million shares.

On page 285, it states 3.256B shares will issued. It states these are H shares though a friend said he believes this represents 1.6B for the HK listing and 1.6B shares for the STAR Board listing.

Updated Financials - YTD through Q3 Year over Year (YoY)

- Revenues +43% year YoY to RMB 118.191B.

- Gross Profits +74% YoY to RMB 69.549B from RMB 39.907B.

- Gross Margin 58.8%, up from 48.1% one year ago

US-China Political Rhetoric

Though the filing doesn’t address the US putting the company on the entity list, it doesn’t shy away from mentioning the deteriorating US-China political relationship. The company reassures investors that any US actions would have a minimal impact on its business, which is primarily conducted in China.

Investors

Other investors include a host of Chinese pension funds, insurance companies, and financial firms. Foreign investors include PE firms Warburg Pincus, KKR, Silver Lake, Carlyle and General Atlantic, sovereign wealth funds Temasek and GIC, Canadian pension fund CPP, the University of California, and US fund families T Rowe, Fidelity, and BlackRock, among others.

Key News

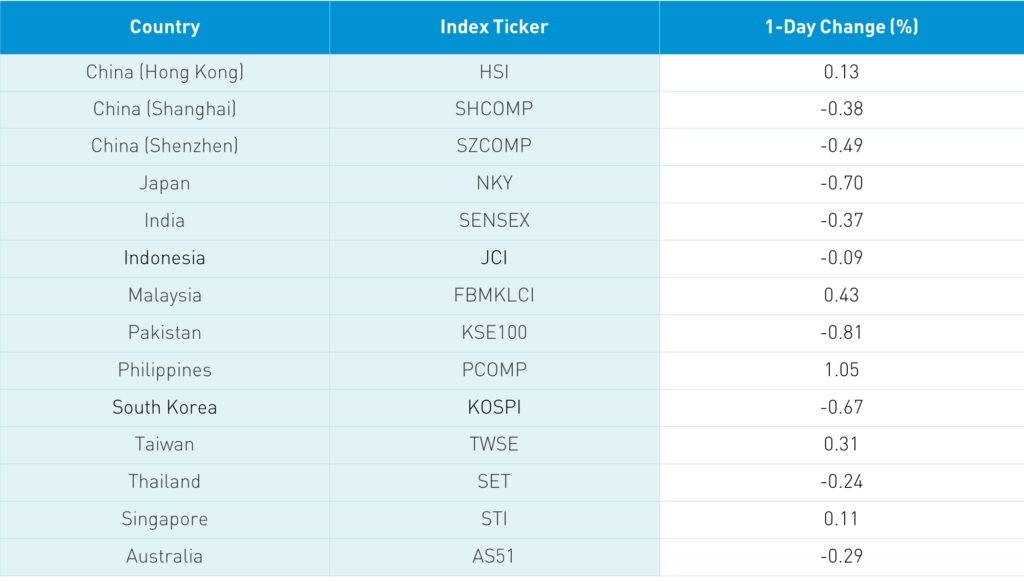

Asian equities were largely off overnight as investors remain skeptical over the new US stimulus deal and wary of potential volatility surrounding the US election. Trading volumes in the region were anemic again as investors sit on their hands for the time being. The Hang Seng Index managed a +0.13% gain though decliners outpaced winners on both the Hang Seng Index and broader Hang Seng Composite. Hong Kong volume leaders were Tencent, which fell -0.52%, Alibaba HK, which pulled a James Bond falling -0.07%, Meituan Dianping, which was unchanged, China Construction Bank, which gained +2.3%, ICBC bank, which gained +2.61%, BYD, which gained +4.37%, Xiaomi, which fell -0.22%, and AIA Group, which rose +0.71%. Macau casino stocks were led higher after results from Sands China, which gained +5.2%. Yesterday’s telecom rally was short lived as China Unicom fell -11.5% and China Telecom dropped -5.36% on paltry quarterly results. Brokers led financials higher as Hong Kong IPOs should help them. The establishment of Wealth Connect, which will allow Mainland investors to buy asset management products in Hong Kong, is also set to benefit Hong Kong brokers. The Mainland was off with Shanghai falling -0.38% and Shenzhen falling -0.49% in light trading as all sectors were in the red. After highlighting CNY/renminbi’s strength, it, of course, reversed today versus the US dollar. It is worth noting that copper had a decent day.

Growing up, I loved the Mad Max films. Whenever Max was being chased, he would punch the nitrous in his Ford Falcon to accelerate away. This kind of reminds me of the US market’s infatuation with stimulus. The Wall Street Journal’s James Mackintosh has an interesting article on whether the E (earnings) can justify the P (price) for US equities. I hope so, though he raises some good points. US equities going sideways could raise interest in non-US equities as the dollar’s slide gives them a nice boost. Japan and Europe have very low/negative rates so the dollar can’t move too much against them. However, Emerging Markets and particularly China have higher interest rates, which could help Emerging Market currencies versus the dollar.

TAL Education (TAL US) reported earnings before the US market open today that missed on both the top line and bottom line. Adding insult to injury was the revenue forecast for next quarter. The problem is exploding costs, which cut into margins and profits. Management will have a lot of explaining to do on the investor call. TAL’s stock took a hit yesterday after fellow online education firm GSX was hit by an analyst downgrade and chatter of slower sales.

- Revenue +20.8% to $1.1B up from $913mm versus estimate $1.13B

- Operating costs & expenses +34.7%, Cost of Revenues +29.1%, selling and marketing expenses +44.3%, and General & Administrative expenses +33.5%

- Student enrollment +655 to 5.632mm

- Gross profit +14.3% to $581mm from $508mm

- Adjusted EPS $0.08 up from $0.01 versus estimate $0.12

- Q3 Revenue Forecast $1.06B to $1.09B versus estimate $1.13B

H-Share Update

The Hang Seng overcame morning losses to close +0.13%/+31 index points to close at 24,786. Volumes were off, -2% below the 1-year average, while breadth was off too with 18 advancers and 27 decliners. The 204 Chinese companies listed in Hong Kong fell -0.15% as only financials and real estate were positive, gaining +1.35% and +0.67%, respectively. On the downside, staples -1.3%, energy -1.25%, materials -0.9%, communication -0.88% and health care -0.46%. Southbound Connect volumes were light as Mainland investors bought $275 million worth of Hong Kong stocks as Southbound Connect accounted for 10.4% of Hong Kong turnover.

A-Share Update

Shanghai and Shenzhen cut losses with an afternoon rally to close -0.38% and -0.49% at 3,312 and 2,243, respectively. Volumes were off -6% along with breadth with 1,373 advancers and 2,270 decliners. The 517 Mainland stocks within the MSCI China All Shares Index declined -0.69% with all sectors in the red. Laggards were communication -2.11%, health care -1.72%, materials -1.13%, industrials -1.08%, and tech -0.61%. Northbound Stock Connect volumes were light as foreign investors sold -$411 million worth of Mainland stocks today as Northbound Connect trading accounted for 5.6% of Mainland turnover.

Last Night’s Exchange Rates & Yields

- CNY/USD 6.66 versus 6.67 yesterday

- CNY/EUR 7.90 versus 7.90 yesterday

- Yield on 1-Day Government Bond 1.35% versus 1.34% yesterday

- Yield on 10-Year Government Bond 3.19% versus 3.20% yesterday

- Yield on 10-Year China Development Bank Bond 3.72% versus 3.74% yesterday