March PMIs Shine, Stocks Hit With Quarter-End Clip

3 Min. Read Time

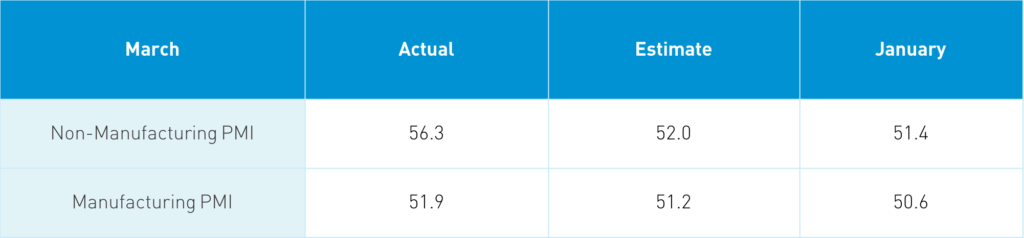

PMI Release Overview

Takeaway: The release was a strong one, as anticipated. PMIs are diffusion indexes. Readings above 50 indicate month-to-month expansion while readings under 50 indicate contraction. Today, we had the “official” PMI as the National Bureau of Statistics conducts a large survey of purchasing managers across predominantly large companies. Within the Manufacturing PMI, output and new orders rose from February along with import and export orders while inventories of raw materials continued to dwindle in a good sign for commodities. Input and output prices increased from February’s 66.7 and 58.5 to 69.4 and 59.4, which is not a great sign if you are worried about inflation, though Chinese bonds rallied today. We are on the cusp of global reopening, which will only power China’s export manufacturing. Within the Non-manufacturing release, we see a similar story as new orders, input prices, and sales prices increased while inventories contracted. Business activity expectations are strong at 63.7, down from February’s 64. The strong release was widely anticipated and there was little to no market reaction. If anything, it supports removing stimulus, though that will happen incrementally.

Key News

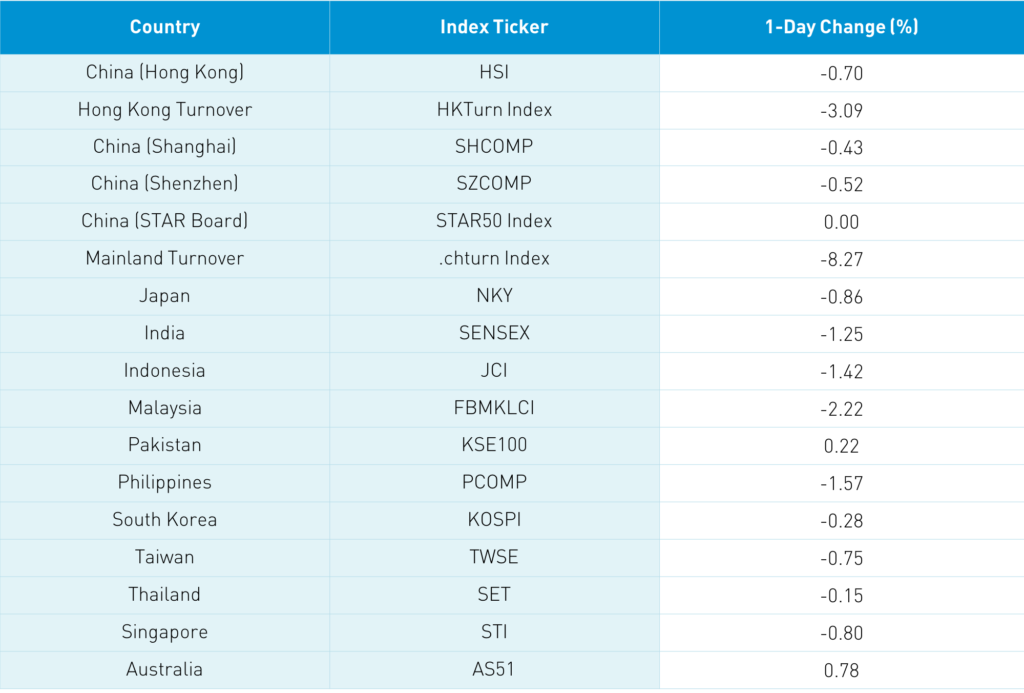

Asian markets were a sea of red on the last day of the quarter and in advance of market holidays on Friday and Monday. There was no single catalyst to the downside though quarter-end rebalancing was potentially a factor. There was no improvement in US-China political rhetoric. Earnings drove the action in single securities along with concerns about rising US Treasury yields.

The Wall Street Journal noted today that Japanese investors are selling US Treasury bonds and redeploying the proceeds globally. Overnight, China’s five-year government bond yield declined from yesterday’s 3.02% to 2.98%.

Reuters is reporting that China may launch a new stock exchange to attract foreign companies. The article mentions Apple and Tesla as potential candidates for secondary China listings, along with US-listed Chinese companies. Admittedly, it does seem somewhat premature at this point to be naming potential companies.

Two IPOs overnight highlight how investor attitudes have changed as fintech company Bairong (6608 HK) fell 16% after its Hong Kong IPO and food delivery company Deliveroo (ROO LN) fell -24% after its London listing. These IPOs would have been monsters a year ago.

One year ago, I noticed a chart from a research report that took China’s stock dividend yield and divided it by the 10-year Chinese government bond yield. Since 2006, the average is 0.58 while today we are at 0.64, which would indicate stocks are attractive versus bonds, though we are far from an extreme level.

Reuters is also reporting that JD.com (JD US) sold its cloud and artificial intelligence unit to its fintech subsidiary JD Digits for $2.4 billion in order to focus on E-Commerce. However, the company’s website has nothing on this.

H-Share Update

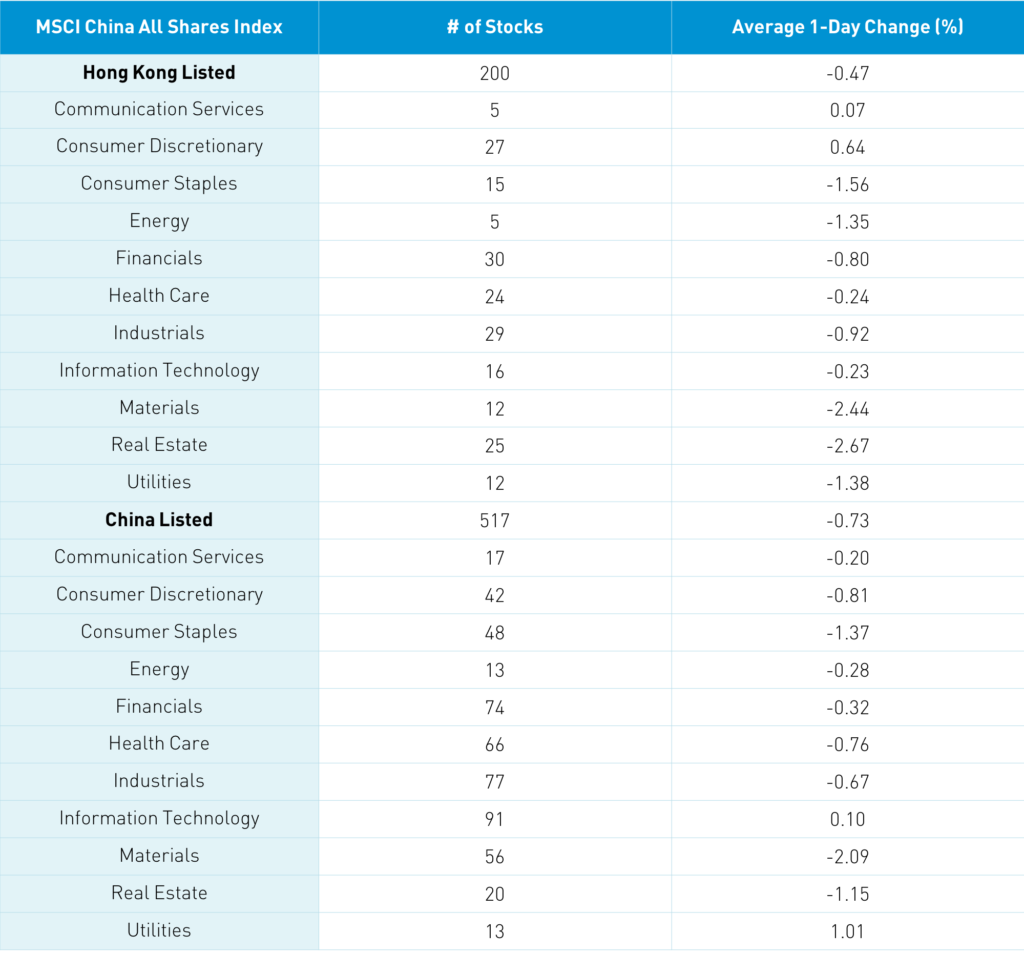

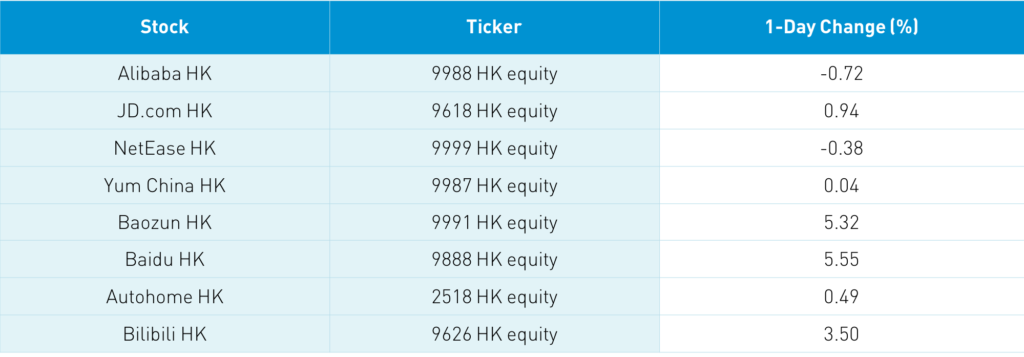

The Hang Seng Index opened higher but fell quickly, closing -0.7% as volume declined -3% from yesterday, which is just above the 1-year average. Breadth was off today with nearly 3 decliners for every 1 advancer while the 200 Chinese stocks listed in Hong Kong and within the MSCI China All Shares Index declined -0.47%. Everything was off today though real estate fell -2.67%, materials fell -2.44%, and staples fell -1.35%. Meanwhile, communication and discretionary posted small gains. Hong Kong’s most heavily traded stocks by value were Xiaomi, which gained +0.59% as the investors appear to cheer its move into electric vehicles, Tencent, which gained +0.08%, Meituan, which gained +1.57%, Alibaba HK, which fell -0.72%, Ping An Insurance, which fell -1.07%, HK Exchanges, which fell -1.34%, BYD, which fell -3.23%, AIA, which fell -1.82%, Baidu, which gained +5.55%, and pork provider WH Group, which fell -12.74% after poor Q4 results. Southbound Connect volumes were light as Mainland investors bought $168 million worth of Hong Kong stocks today as Southbound Connect trading accounted for 11.5% of Hong Kong turnover. Tencent saw robust inflows once again.

A-Share Update

Shanghai, Shenzhen, and the STAR Board ended -0.43%, -0.52%, and flat, respectively, as turnover slumped -8% from yesterday to just 79% of the 1-year average. The 517 Mainland stocks within the MSCI China All Shares Index were off -0.73% with materials -2.09%, real estate -1.19% and staples -1.37%. Meanwhile, utilities and tech managed gains of 1.01% and 0.1%, respectively. Breadth was decent with 2,068 advancers and 1,751 decliners. Clean tech plays managed to have a good day. The Mainland’s most heavily traded stocks by value were Sany Heavy Industry, which fell -7.7% after beating 2020 revenue expectations but missing on net income (Sany’s forward P/E is 15 versus a 2-year average of 12.3), Kweichow Moutai, which fell -2.29% after revenue missed but net income beat expectations (similar forward P/E 44 versus 2 year average of 33.5), Longi Green Energy, which gained +0.43%, CATL, which gained +1%, BYD, which lost -2.66%, Sungrow Power, which fell -0.51%, China Southern Power, which gained +1.74%, Ping An Insurance, which fell -0.84%, broker East Money, which fell -2.47%, and liquor company Wuliangye Yibin, which fell -2%. Northbound Stock Connect volumes were moderate as foreign investors sold -$1.206 billion worth of Mainland stocks and Northbound Connect trading accounted for 6.4% of Mainland turnover. Bonds rallied, CNY appreciated versus the US dollar, and copper fell.

Last Night’s Exchange Rates, Prices, & Yields

- CNY/USD 6.55 versus 6.57 yesterday

- CNY/EUR 7.69 versus 7.71 yesterday

- Yield on 1-Day Government Bond 1.81% versus 1.61% yesterday

- Yield on 10-Year Government Bond 3.19% versus 3.21% yesterday

- Yield on 10-Year China Development Bank Bond 3.57% versus 3.58% yesterday

- China’s Copper Price -1.09%