You Don’t Need Tea Leaves to Read Where Policy Wants Capital, Week in Review

4 Min. Read Time

Week in Review

- On Monday, we heard that Bytedance’s long-anticipated IPO in Hong Kong may occur as early as the fourth quarter this year or early 2022.

- Both imports and exports slowed in July, according to an economic release Monday. The steeper drop in exports can be partially explained by global economies coming back online, resulting in consumers rotating spending from physical goods and into services such as dining and travel.

- China internet stocks rallied Tuesday as fintech platform Lufax reported that Q2 net profit increased by +53% year-over-year and that fintech regulation would have a minimal impact on its finances and operations.

- Baidu reported strong earnings growth Thursday morning before the US market open. The company beat estimates on top-line revenue, but margins suffered due to investment in non-search businesses.

Key News

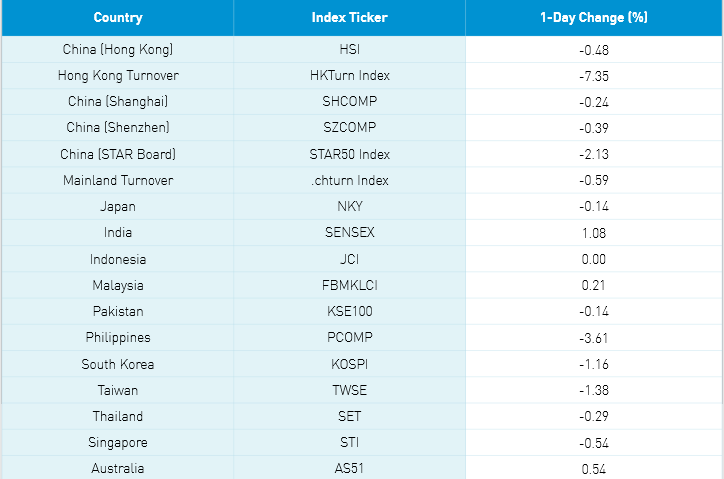

Asian equities ended the week mixed with India outperforming while the Philippines, Korea, and Taiwan underperformed in a fairly quiet August Friday. There was chatter that China’s Sunday economic release might be weaker than expected as flooding and regional lockdowns, such as the one occurring in port city Ningbo currently, to contain Delta might constrain July data. This might lead to more accommodative policies ironically that bad news would be good news.

Hong Kong and Mainland stocks were off a touch led lower by tech as semiconductor stocks and internet stocks were off. There is increasing chatter of semiconductors reaching a cyclical peak just as governments globally throw subsidies at the sector. Clean energy was off because the Senate’s infrastructure package includes an amendment that would ban Chinese solar inputs in US government contracts. I doubt it would have any material impact on the companies in the space though it will undoubtedly raise the cost for the US government given that China is the low-cost producer. How quickly we forget about Solyndra! Also, an ECON 101 reminder that tariffs are inflationary.

Within clean tech, the one bright spot in both Mainland China and Hong Kong were material inputs which had a strong day as demand is expected to outpace supply. EV battery giant CATL was a factor after announcing a $9B stock sale which sent the stock down to an intra-day low of -4.38% though it rallied to close +0.01%. CATL was a net sale from foreign investors in Northbound Stock Connect along with liquor giant Kweichow Moutai leading to a net outflow day. Hong Kong internet stocks had an off night as the constant media barrage on the space isn’t letting up.

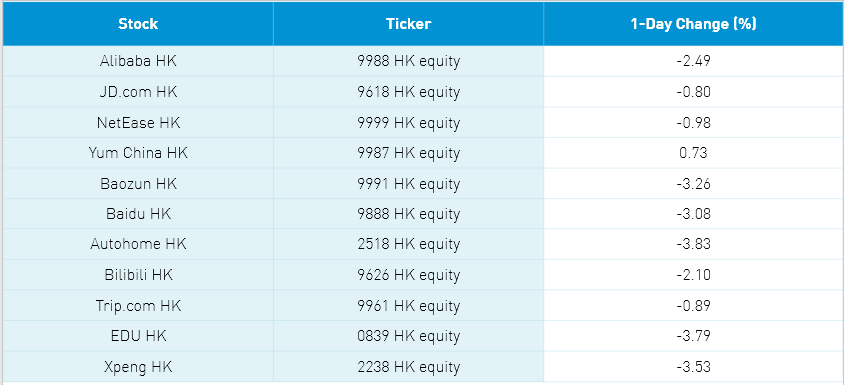

I thought Baidu and IQ had good results yesterday though they were sent to the woodshed. This is despite Baidu hosting their Baidu World event on Chinese TV next week. On Baidu’s earnings call, when questioned about data privacy, CEO, Chairman, and founder Robin Li responded, “Data security is very important to us, and we have consistently improved on the management of our internal data security system over the past few years…I’m quite confident we will be able to cope with the new regulatory environment well in terms of data security and user privacy.” Strong statement!

CFO and soon-to-be Chief Strategy Officer Herman Yu made an interesting statement on the China internet space saying “…the country is promoting new growth sectors such as industrial Internet, V2X autonomous driving and monetization of city government. Thus, we will not be surprised if certain incentives for the older industries gradually decrease, while the new economy benefits from government incentives. We believe government policy will also be adjusted to support these new growth areas.” Baidu is saying that its non-search businesses including AI, EV software, and cloud computing are beneficiaries of China’s policy favoring the technologies China will need in the coming decades. We as investors should take note and position accordingly.

There was a fair amount of chatter on global and Chinese private equity firms taking a performance hit on after-school tutoring companies. Worth noting, foreign direct investment, which is reported on a year-to-date basis, clearly fell in July with a reading of 25.5% versus year-to-date through June’s 28.7%. Not a significant fall but policymakers should recognize that publicity surrounding the China internet crackdown could affect the real economy as multi-national corporations worry that what they are seeing could happen to them.

Personal Update

Good to be back in the saddle after a few restful vacation days with the family. Shoutout to my colleagues Henry and Megan for their efforts in keeping you informed. I read Pearl Buck’s The Good Earth which is about a Chinese farmer in the 1920s. A good insight into how far not only China, but the world, has come over the last hundred years. An insightful read for all parents in my opinion. I also read another good Lee Child book in his Jack Reacher series which I recommend.

H-Share Update

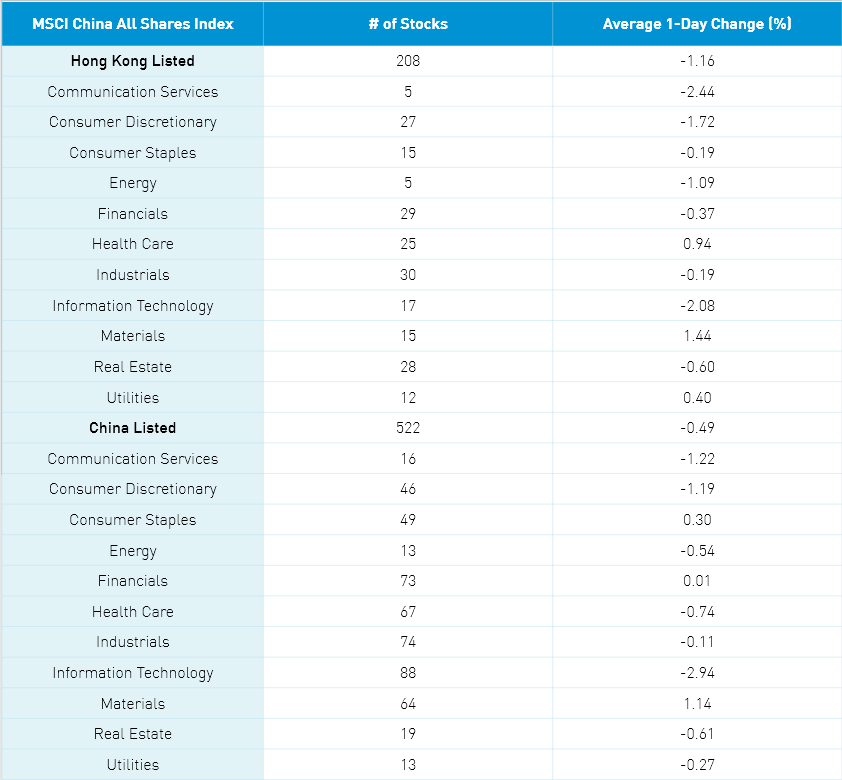

The Hang Seng Index bounced around the room closing down -0.48% while the Hang Tech fell -1.93% on light volume off -7% from yesterday which is just 75% of the 1-year average. The 208 Chinese companies within the MSCI China All Shares was off -1.16% with materials +1.44%, healthcare +0.94% and utilities +0.4% while communication -2.44%, tech -2.08%, discretionary -1.72%, energy -1.09%, real estate -0.6%, financials -0.37%, industrials -0.19% and staples -0.19%. Hong Kong’s most heavily traded by value were Tencent -2.45%, Alibaba HK -2.49%, Meituan -1.35%, Xiaomi -3.23%, China Mobile +3.08%, SMIC -3.91%, Ping -1.32%, Wuxi Biologics +1.92%, Geely Auto -1.56% and BYD -1.23%. Southbound Stock Connect volumes were average/light as Mainland investors sold -$289mm of Hong Kong stocks as Southbound trading accounted for 14.5% of Hong Kong turnover.

A-Share Update

Shanghai, Shenzhen and STAR Board were off -0.24%, -0.39% and -2.13% on volume flat from yesterday which is still 141% of the 1-year average. The 522 Mainland stocks within the MSCI China All Shares were off -0.48% led by materials +1.15%, staples +0.31% and financials +0.02% while tech -2.93%, communication -1.21%, discretionary -1.18%, healthcare -0.73%, real estate -0.59%, energy -0.53%, utilities -0.25% and industrials -0.1%. The Mainland’s most heavily traded by value were Qinghai Salt Lake +3.18%, CATL +0.01%, China Northern Rare Earth +1.05%, Tianqi Lithium +0.73%, Cosco Shipping -1.55%, Shanxi Meijin Energy +3.5%, BYD -2.9%, Longi Green Energy -2.86%, Kweichow Moutai +0.59% and Sungrow PowerSupply -4.02%. Northbound Stock Connect volumes were moderate/high as foreign investors sold -$191mm of Mainland stocks with Kweichow Moutai and CATL net sales as Northbound trading accounted for 4.9% of Mainland trading.

Last Night’s Exchange Rates, Prices, & Yields

- CNY/USD 6.48 versus 6.48 yesterday

- CNY/EUR 7.62 versus 7.60 yesterday

- Yield on 1-Day Government Bond 1.48% versus 1.46% yesterday

- Yield on 10-Year Government Bond 2.88% versus 2.86% yesterday

- Yield on 10-Year China Development Bank Bond 3.23% versus 3.21% yesterday

- Copper Price -0.40% overnight