TGHKSWGF! Thank Goodness HK Stocks Were Green Friday! Week In Review

2 Min. Read Time

Week In Review

- Nearly 3 million electric vehicles were sold in China in 2021, according to full year sales data reported Monday.

- Tencent sold its $3 billion stake in Southeast Asian E-Commerce platform Sea on Tuesday, leading to a slight downdraft in Tencent stock and others known to have been invested in by the internet conglomerate.

- A growth to value rotation took hold of markets in Asia on Wednesday following a relatively quiet start to 2022.

- Asian equities were lower on Thursday on US interest rate news, though Hong Kong internet stocks were a bright spot as the sector rebounded.

Friday’s Key News

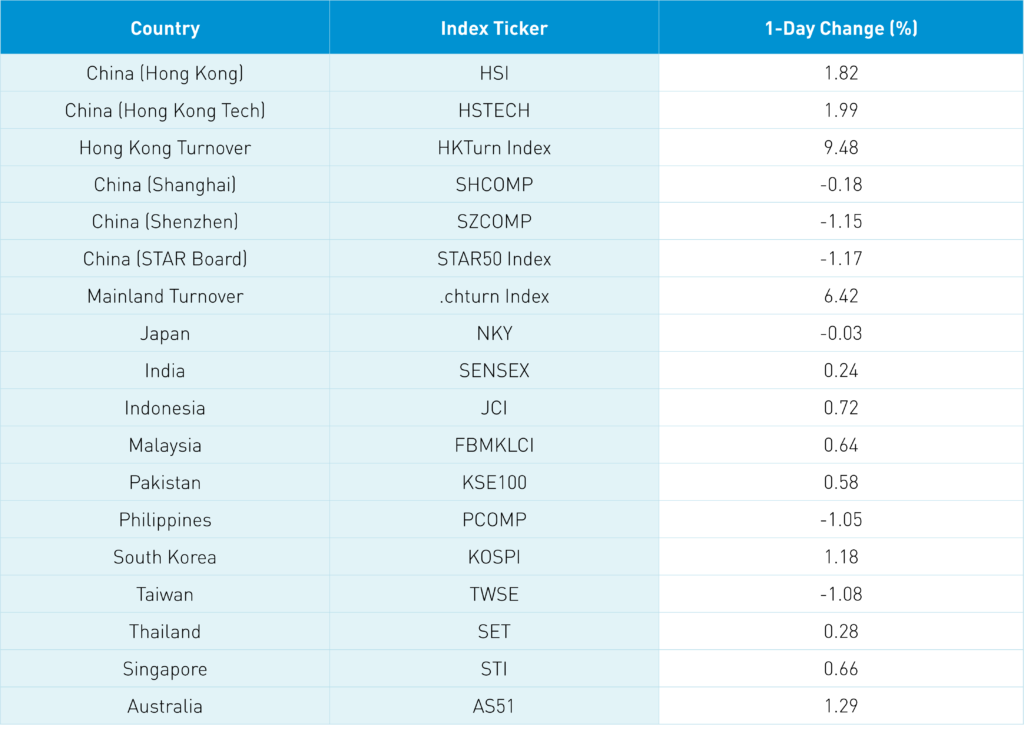

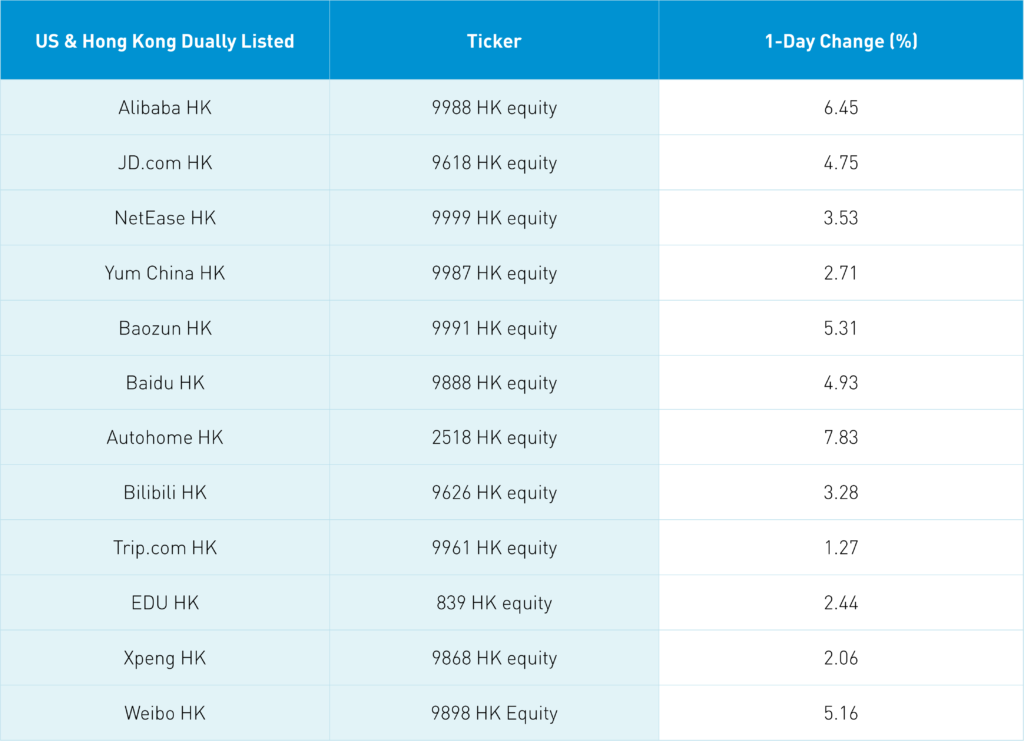

Asian equities rebounded as Hong Kong stocks outperformed while Japan was among the few markets off today. The Hang Seng gained +1.82% though the real story was Hong Kong internet stocks, which powered the Hang Seng Tech Index higher by +1.99%. Hong Kong’s most heavily traded stocks were Tencent, which gained +1.37%, Alibaba HK, which gained +6.45%, and Meituan, which gained +0.89%. I suspect the long JD.com/short Alibaba trade is being unwound with increasing urgency.

Yesterday, a prestigious investment bank’s Asia strategy equity team recommended China internet. What we really need is for big fund families to come back into the space, which could be driven by whether China can outperform India. Remember that as long as India outperforms, China will be underweighted (my Yogi Berra impersonation) as big fund families are currently overweight India

There is some chatter that Alibaba is providing cautious guidance in advance of their quiet period pre-financial results.

Volumes were up +9.48% from yesterday, which is only 88% of the 1-year average while 3 stocks advanced for every 2 decliners. Tencent and Meituan saw small net buying from Mainland investors via Southbound Stock Connect.

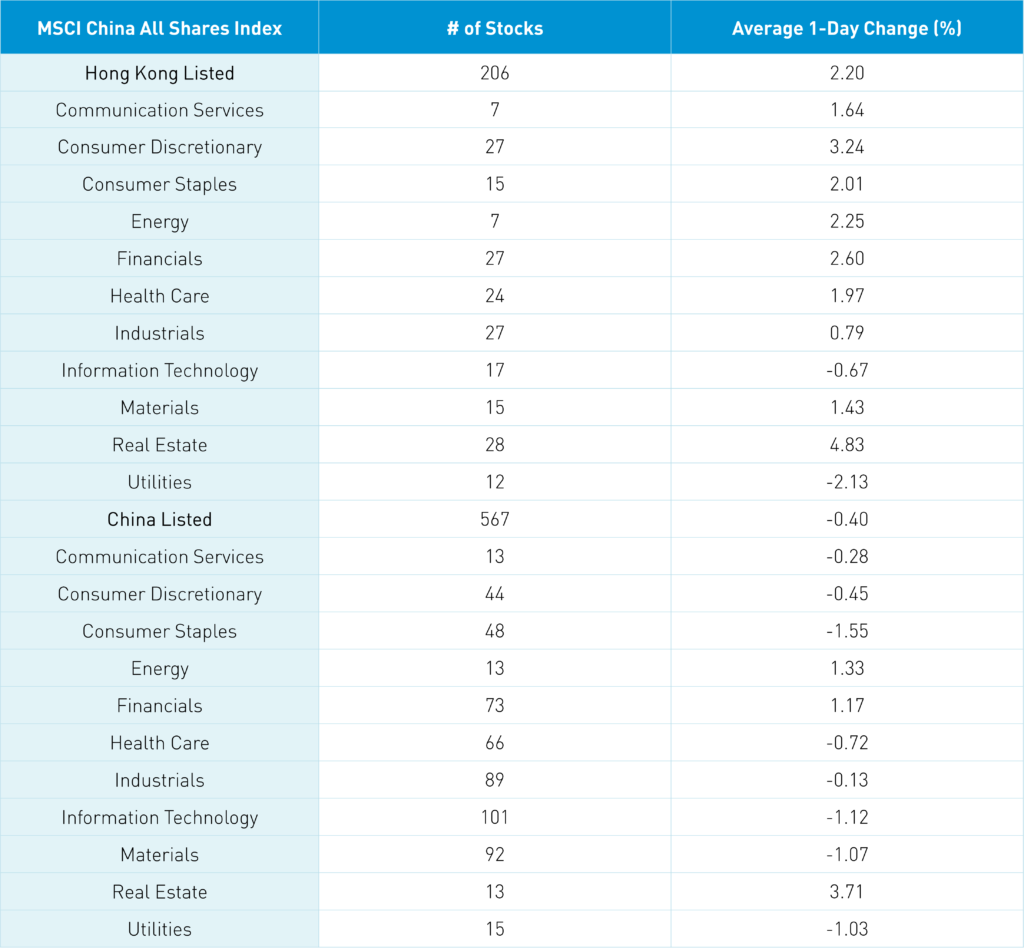

Real estate was the best performing sector in both Hong Kong and China gaining +4.83% and +3.69% in each market, respectively, on news that loans focused on mergers & acquisitions will not be included in the solvency metrics for real estate companies. Translation: real estate companies with strong balance sheets should buy/take over weak firms. It also shows policymakers have their ear to the real estate/Evergrande situation and do not want to see it spiral out of control.

The cleantech ecosystem had another tough night in both Hong Kong and Mainland China as electric vehicles (EVs), solar, wind, lithium, and nuclear power all struggled. Shanghai (large stocks/value) was off -0.18% while Shenzhen (large-mid stocks/growth) was off -1.15% and the STAR Board (mid-small stocks/growth) fell -1.17% on volume that was up +6.42% from yesterday, which is 114% of the 1-year average. Breadth was off with 3 decliners for every 1 advancer as growth/small caps underperformed value/large caps. These themes were big overweights for active managers and investors, along with liquor stocks.

The EV subsidy cut, which I don’t think anybody believes is detrimental to the trajectory of Chinese EV adoption, has led to a vicious round of profit-taking. Throw in the value/growth rotation that is playing out globally, it has made for a tough start to 2022. Because these stocks are well-positioned in the long run, I suspect investors will take advantage of this dip as an entry point.

Foreign investors used the dip in Mainland stocks overnight to snap up $1.464 billion worth of A-shares via Northbound Stock Connect. For the week, foreign investors bought a net $974 billion worth of Mainland stocks. Chinese Treasury bonds rallied, currency was flat versus the US dollar, and copper was off. The Mainland’s decline appears to have been noticed by the CSRC, China’s SEC, as numerous positive statements were made though some were after the close.

My colleague, Dr. Xiaolin Chen, shares her thoughts on the "three P's" that are poised to shape 2022 in our latest video.

Last Night’s Exchange Rates, Prices, & Yields

- CNY/USD 6.38 versus 6.38 yesterday

- CNY/EUR 7.23 versus 7.22 yesterday

- Yield on 1-Day Government Bond 1.76% versus 1.76% yesterday

- Yield on 10-Year Government Bond 2.82% versus 2.82% yesterday

- Yield on 10-Year China Development Bank Bond 3.10% versus 3.09% yesterday

- Copper Price -0.79% overnight