US Commerce Department’s Unverified List Tanks Wuxi and Investor Sentiment

3 Min. Read Time

| Webinar 1: Carbon/climate |

| Join us this Thursday, February 10, 2022 for our webinar at 11:00 am EST. Carbon Market State of the Union with KraneShares and Climate Finance Partners Click here to register. |

| Webinar 2: China |

| Join us on Tuesday, February 15, 2022 for our webinar at 10:00 am EST. Get Your “A” Game On – KraneShares and MSCI Discuss the Future of Investing in Mainland China Click here to register. |

Key News

Going into last night’s market session, I was in a great mood. My weekend reading of institutional research focused on China’s inexpensive valuations, under allocation from investors, China’s monetary easing in 2022 against the backdrop of Fed tightening, and the likely end of China's internet regulation. I also caught a webinar from UBS Asset Management’s legendary portfolio manager Bin Shi who manages $25B of China's dedicated equity strategies. Bin is focused on similar themes though he also mentioned the likelihood of China developing a coronavirus vaccine that would end China’s draconian lockdowns.

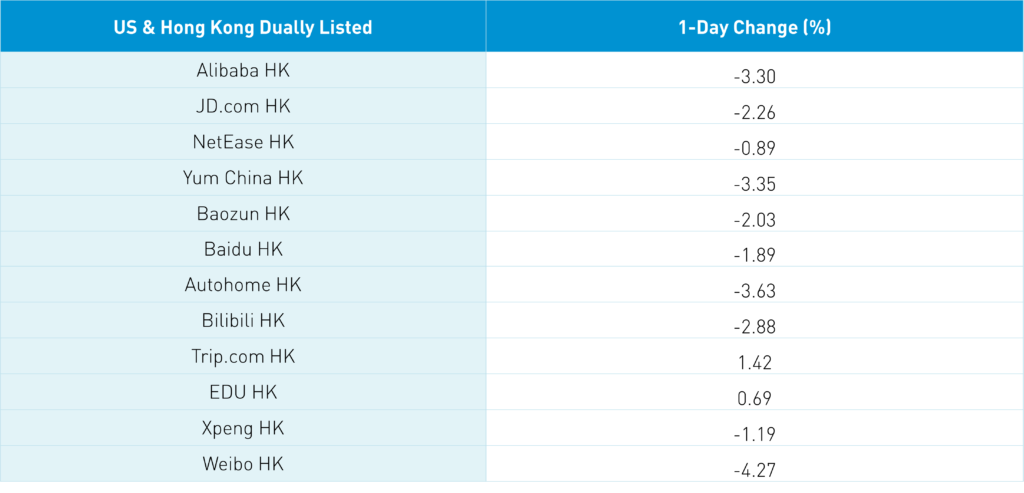

While Asia had a good night, China and Hong Kong underperformed. Alibaba’s filing of one billion new shares last Friday is rumored to be linked to early and large investor SoftBank unloading some of its stake. That may or may not be true. What if SoftBank is simply converting its non-public stake into Alibaba’s HK listing to reduce its risk of ADR delisting? There are several other theories out there that are non-sale related but it has weighed heavily on Alibaba and investor sentiment in the China internet space. A sale at Alibaba’s current price makes no sense to me.

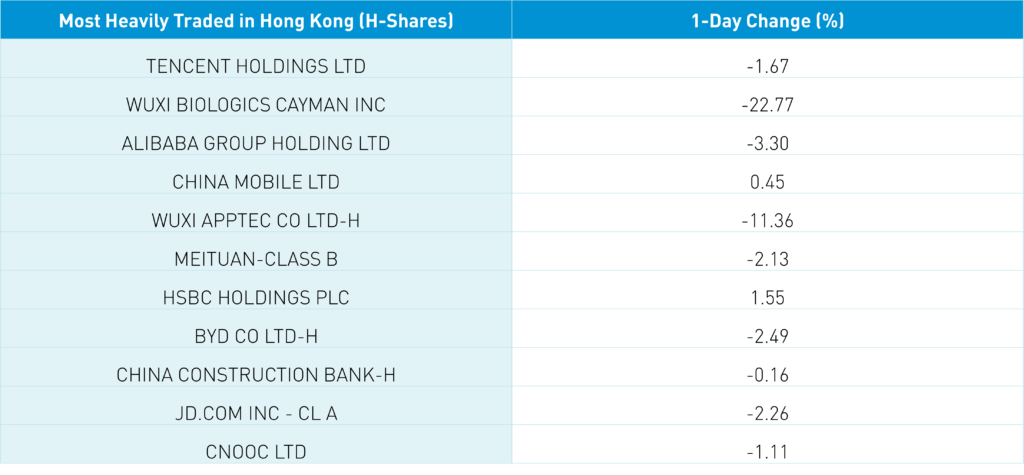

We also had the US Commerce Department add thirty-three Chinese companies to an unverified red flag list including Wuxi Biologics (2269 HK), a highly regarded and widely owned global pharmaceutical company. Investors in Asia didn’t do a lot of homework on what the unverified list is as it simply states that the company needs to explain what equipment it imports from the US. This is exceedingly different than the entity list/Executive order list that bans foreign ownership. Wuxi tanked -22.75% prior to being halted in Hong Kong as the US Commerce effectively destroyed $14.035 billion of investors' saving.

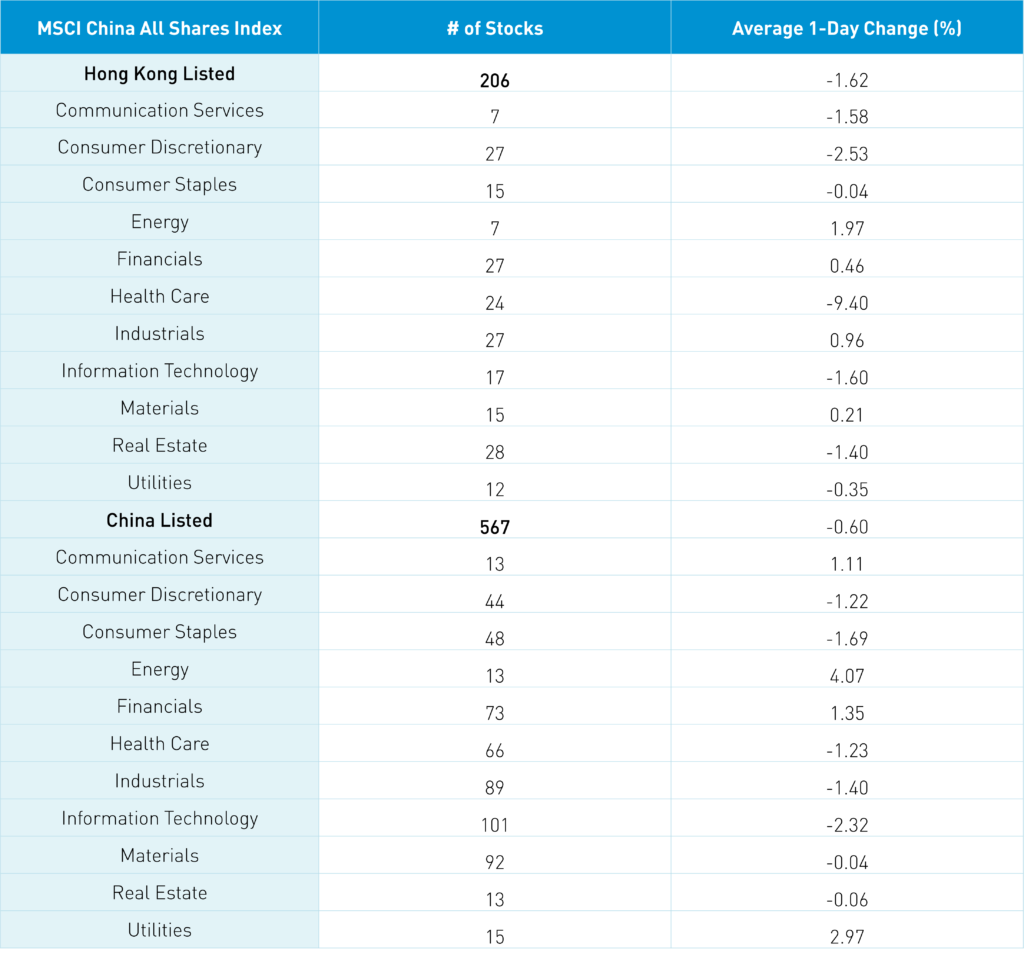

The Hang Seng Index and Hang Seng Tech were off -1.02% and -1.6% on volume +5.89% from yesterday which is 83% of the 1-year average. Value sectors managed a decent day as energy +1.96%, industrials +0.96%, financials -0.45% and materials -0.21% while healthcare -9.4%, discretionary -2.53% and tech -1.6%. Mainland investors in Hong Kong were fairly quiet as they were very small sellers of Tencent and small buyers of Meituan overnight via Southbound Stock Connect.

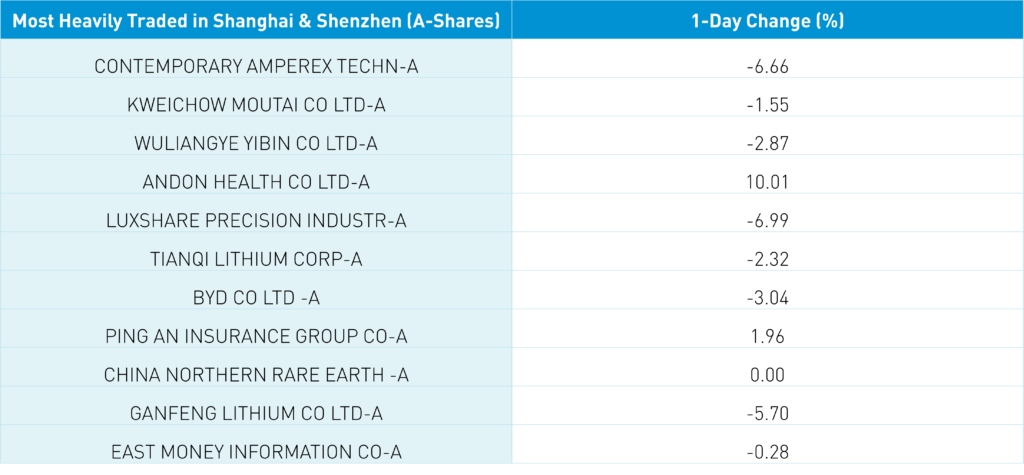

The US Commerce move weighed significantly on growth stocks in the Mainland market as Shanghai (large-cap value) +0.67%, Shenzhen (large/mid-cap growth) -0.24%, and STAR Board (mid/small-cap growth) -2.4%. The markets came off their intra-day lows significantly as Shanghai was off -1.14%, Shenzhen -2.26%, and STAR -3.41% though there was talk of China’s national team buying stocks. Pension plans and insurance companies tend to buy Mainland stocks on weakness. Dubbed “The Plunge Protection Team”, these institutional investors are simply buying low. They do focus on mega-cap/large caps stocks which is why Mainland indexes geared to mega-caps will outperform. For instance, ETFs based on the MSCI China A50 will outperform the CSI 300 which will, in turn, outperform the MSCI China A. Volumes were +6.5% from yesterday which is 83% of the 1-year average while there were 2 advancers for every 1 decliner. Foreign investors sold -$128mm of Mainland stocks today via Northbound Stock Connect. Chinese Treasury bonds were off and the currency was off versus the US $. Copper was off small.

So, China didn’t meet its trade obligations, though a global recession caused by a global pandemic might have been a factor. Another factor was the 737Max. If the plane didn’t have its problems, Chinese airlines would have bought it, allowing China to have gotten a lot closer to holding its end of the bargain. The other factor of course is that the Chinese don’t believe there is a trade deficit. If one takes the revenue generated from US companies who manufacture and then sell in China and adds that number to China’s exports, there is no trade deficit.

China VAT receipts, a sales tax, increased 21% over Chinese New Year versus 2020. Not too bad! Internet sales were +37% year over year.

There was chatter overnight that PBOC is providing support to the real estate sector via regulation loosening. Also, some chatter of allowing Southbound Connect trading of Hong Kong-listed stocks in RMB versus Hong Kong Dollars.

Last Night’s Exchange Rates, Prices, & Yields

- CNY/USD 6.37 versus 6.36 yesterday

- CNY/EUR 7.27 versus 7.28 yesterday

- Yield on 10-Year Government Bond 2.72% versus 2.73% yesterday

- Yield on 10-Year China Development Bank Bond 2.96% versus 2.97% yesterday

- Copper Price -0.31% overnight