China ADRs to Climb the Great Wall of Worry as PCAOB Resets HFCAA Clock, Week in Review

5 Min. Read Time

Week in Review

- Asian equity markets had a mixed performance week as the PCAOB announced breaking news, Pfizer's COVID treatment was approved, and The Central Economic Work Conference (CEWC) concluded today.

- The PCAOB announced that it has secured complete access to inspect and investigate Chinese firms, which will allow them to maintain their US listings in compliance with the Holding Foreign Companies Accountable Act (HFCAA).

- Pfizer’s Paxlovid COVID treatment was approved in China, along with Genuine Biotech’s Azvudine.

- In this week’s video, Xiabing catches up on the latest developments from Baidu’s Apollo Day and breaks down what has changed since her first Robo Taxi ride in Jiading Shanghai in 2021.

Friday’s Key News

Yesterday, the PCAOB released a statement titled “PCAOB Secures Complete Access to Inspect, Investigate Chinese Firms for First Time in History”. According to the release the CSRC, China’s financial regulator, and Ministry of Finance allowed “complete access to inspect and investigate registered public accounting firms headquartered in Mainland China and Hong Kong.” The PCAOB inspected eight firms from KPMG Huazhen LLP in Mainland China and PricewaterhouseCoopers in Hong Kong Key.

The PCAOB had no problems accessing people, getting testimony or documents without any redactions. Therefore, the PCAOB stated “the Board voted to vacate the previous determinations to the contrary.” This “resets the three-year clock for compliance.” Huge exhale as the nearly two hundred stocks on the HFCAA list will be removed. The PCAOB noted there were deficiencies found which the auditors will need to fix. The SEC statement focused on the future work and compliance needed to be done. We always believed this issue was solvable though policy error was a risk. Due to the hard work by the PCAOB’s thirty plus members, who spent nine weeks away from their families, the US and global investors are better protected. Chinese authorities should be congratulated for making several concessions to allow these companies to remain listed in the US. Both sides should enjoy the weekend and holiday season!

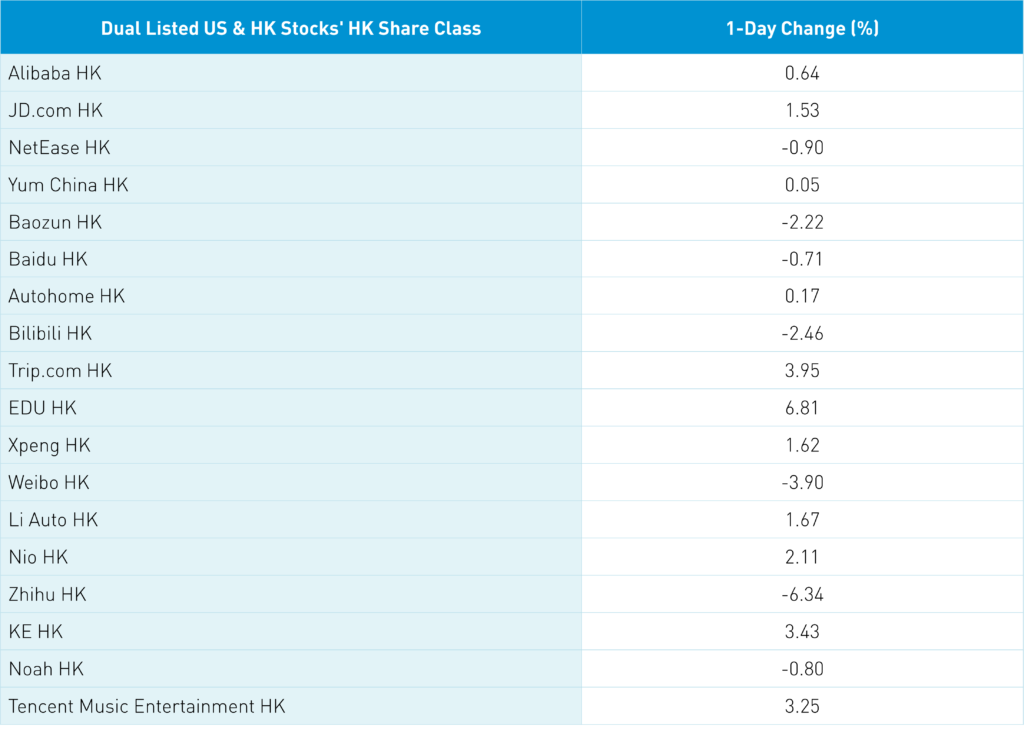

Why didn’t US China ADRs rip yesterday?

1) It was an off day for stocks post-Powell bearish press conference.

2) Fast money traders who had bought the rumor also sold the news following a significant gain over the last month and half.

3) Asset managers are focused on today’s index rebalances and triple witching marking the last big liquidity day of the year.

Long only professional managers now have the green light to come back into the stocks as buying China ADRs was a career risk due to the delisting risk. Who bought Alibaba over the last year? Charlie Munger! Why? He saw the value in the stock but more importantly because he is the boss! I thought Asian equities would gain 50% yesterday candidly. We will likely see a grind higher as investors skepticism and underinvestment toward China recedes. The rerating will happen incrementally as many investors are aware of the Post Party Congress Policy Pivot. We are seeing changes on the Big Three: US China political relationship, Zero COVID, and Real Estate. Yesterday, China’s US Ambassador met with Janet Yellen. At the same time, the Biden Administration added thirty-six companies to a technology export ban list. Ultimately, the US and Chinese economies are highly intertwined while US multi-nationals are doing great business in China.

Asian equities were largely lower with Hong Kong, Malaysia, and Indonesia posting positive returns. Today is the global rebalance for FTSE Russell and S&P indices requiring index fund and ETF managers to trade their portfolios at the market’s close. We also have Triple Witching as stock options, index futures, and index options expire today. Pro golfers call Saturday moving day as they try to position themselves for the Sunday final round. For professional investors, today is the last moving day of the year as volumes will expand allowing managers to buy and sell in size. The Central Economic Work conference, China’s annual economic conference, concluded with “contracting demand, supply shocks, and weak expectations” that have weighed on the economy. The key for investors is the pro-growth nature of the statement as the government moves to implement fiscal and monetary support with an emphasis on DOMESTIC CONSUMPTION.

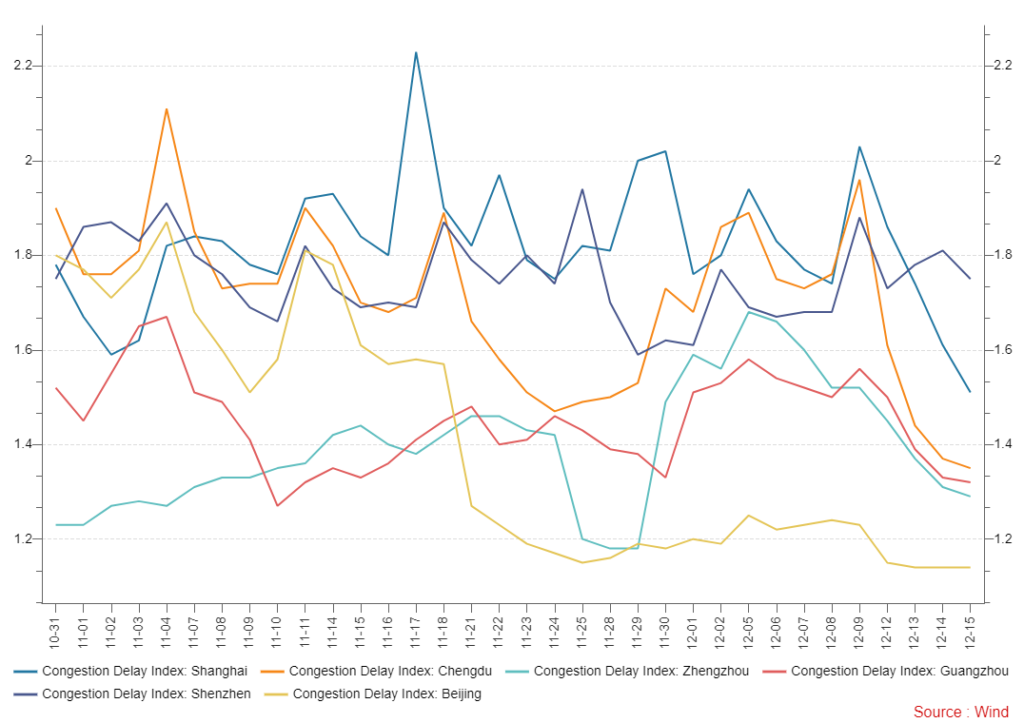

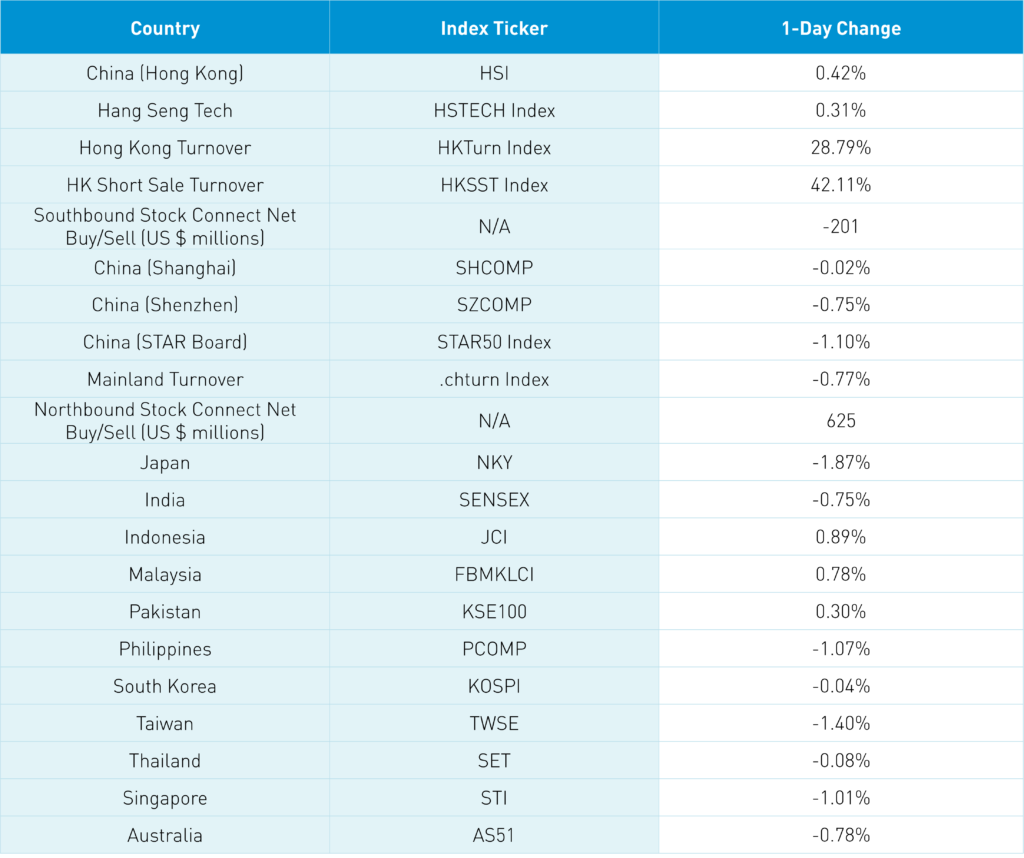

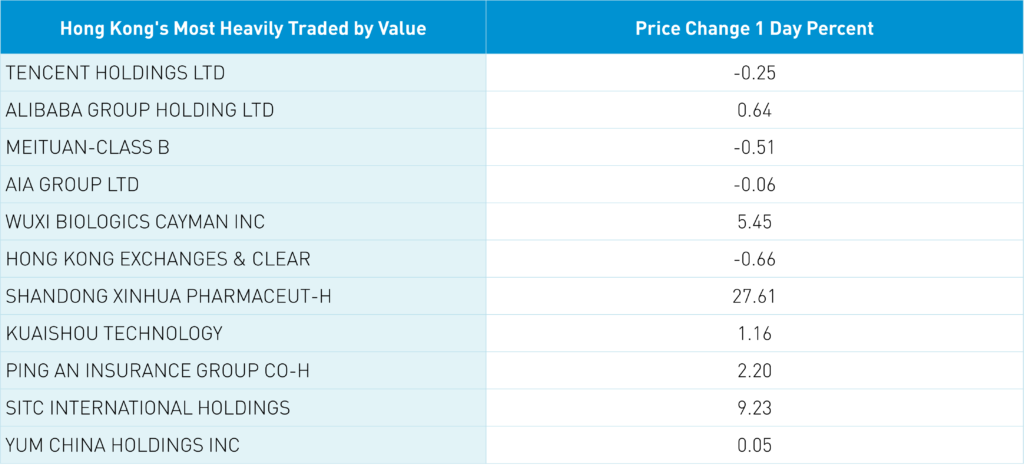

Hong Kong’s most heavily traded were Tencent -0.25%, Alibaba HK +0.64%, and Meituan -0.51% which should lead to a rebound in today’s ADRs. Hong Kong short sellers have been quiet in internet stocks. Real estate was the best sector in Hong Kong gaining +3.32% and China +1.12% as Vice Premier Li stated policies will continue to support the sector. The WSJ had an article today about the rebound in Chinese developers’ bonds which we have been doing for months. We have no buyers! Pain trade is higher as I’ll add to my position today. Value sectors outperformed today in both markets. Foreign investors bought $625 million of Mainland stocks today bringing the week’s total to $812 million. CNY and Asia dollar index both managed a small gain versus the US dollar. Our Mobility Tracker is showing a fall in traffic and subway. Clearly people are being cautious despite the relaxation in COVID rules with chatter that Hong Kong to/from China travel rules will be relaxed.

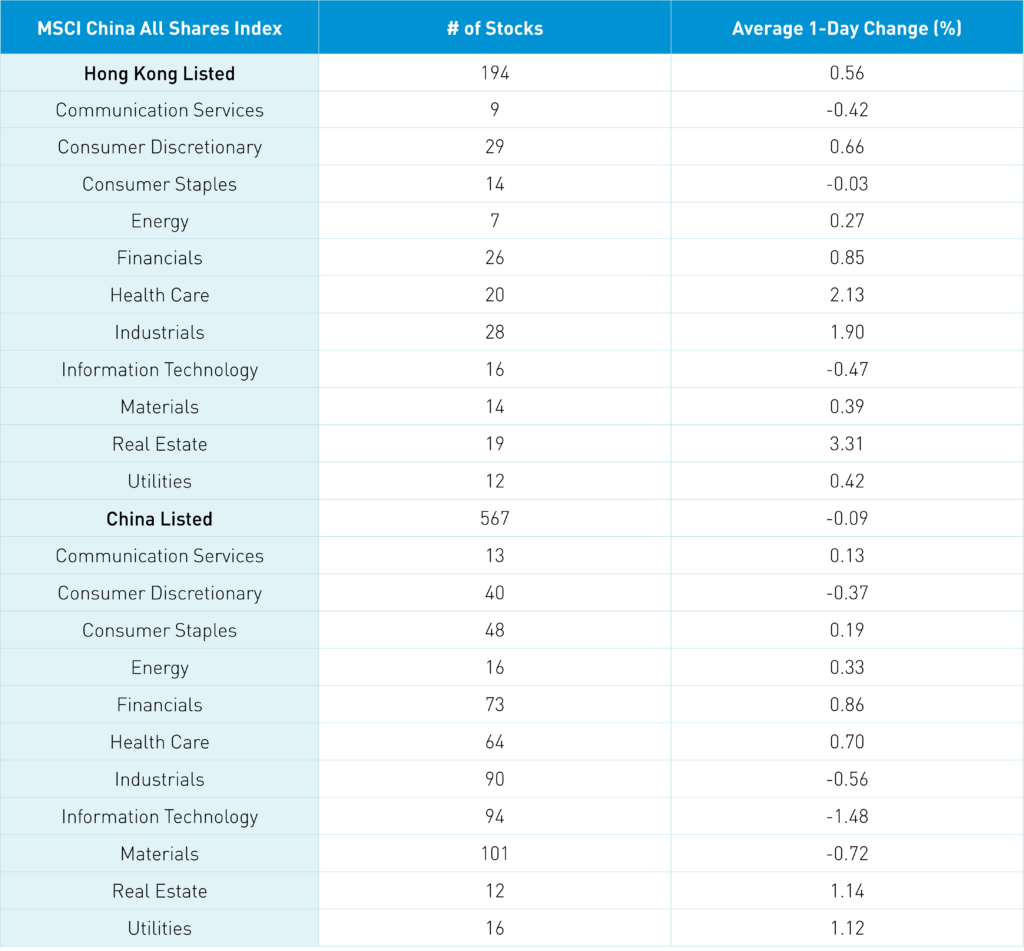

The Hang Seng and Hang Seng Tech gained +0.42% and +0.31% on volume +28.79% from yesterday which is 109% of the 1-year average. 315 stocks gained while 169 stocks declined. Main Board short turnover increased +42% from yesterday which is 91% of the 1-year average as 14% of turnover was short turnover. Value factors outperformed growth factors as small caps outpaced large caps. Top sectors were real estate +3.32%, healthcare +2.14%, and industrials +1.91% while tech -0.46%, communication -0.4%, and staples -0.02%. Top sub-sectors were food, household products, and transportation while semis, software, and telecom were among the worst. Southbound Stock Connect were light as Mainland investors sold -$201 million of Hong Kong stocks with Tencent a small net buy, Meituan and Kuaishou small net sells.

Shanghai, Shenzhen, and STAR Board fell -0.02%, -0.75% and -1.1% on volume -0.77% from yesterday which is 81% of the 1-year average. 1,297 stocks advanced while 3,354 stocks declined. Value factors outperformed growth factors as large caps outpaced small caps. Top sectors were real estate +1.15%, utilities +1.12%, and financials +0.86% while tech -1.48%, materials -0.72%, and industrials -0.56%. Top sub-sectors were pharma, highway industry, and real estate while auto parts, industrial machinery, and base metals were among the worst. Northbound Stock Connect volumes were light as foreign investors bought $625 million of Mainland stocks with Shanghai value stocks outpacing Shenzhen growth stocks. CNY gained 0.02% versus the US dollar closing at 6.97, Treasury bonds were flat, and copper fell -0.83%.

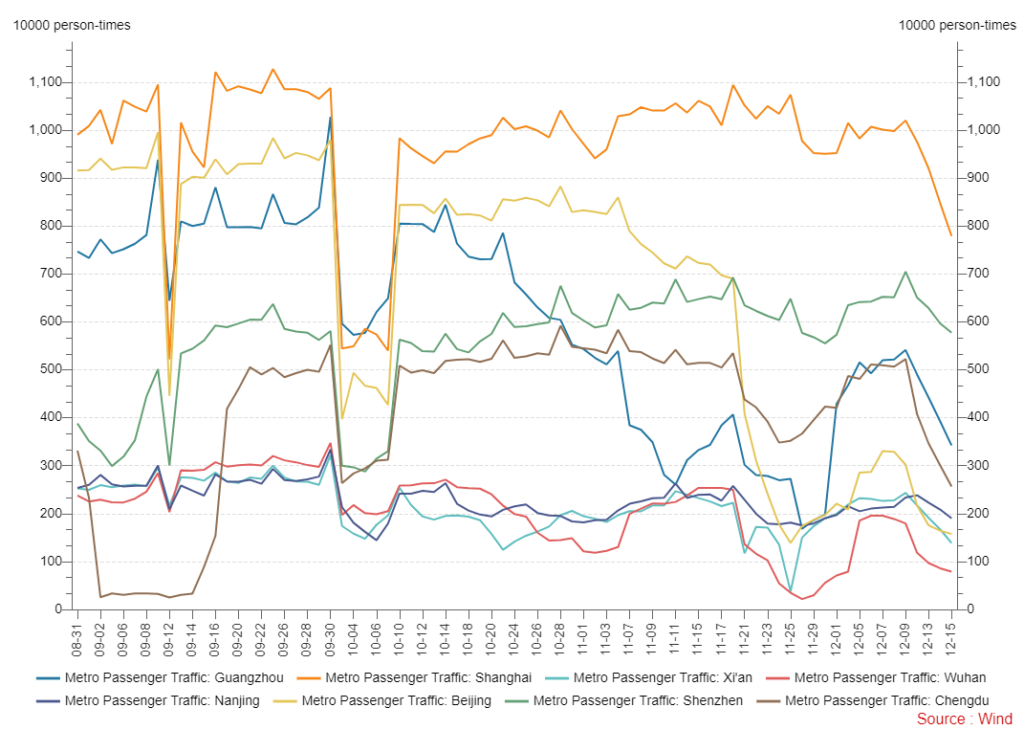

Major City Mobility Tracker

We continue to see activity drop as covid spreads across China.

Last Night's Performance

Last Night’s Exchange Rates, Prices, & Yields

- CNY per USD 6.97 versus 6.97 yesterday

- CNY per EUR 7.40 versus 7.40 yesterday

- Yield on 10-Year Government Bond 2.88% versus 2.88% yesterday

- Yield on 10-Year China Development Bank Bond 3.04% versus 3.03% yesterday

- Copper Price -0.83%